Revealed on November twelfth, 2025 by Felix Martinez

Excessive-yield shares pay out dividends which are considerably increased than the market common. For instance, the S&P 500’s present yield is barely ~1.2%.

Excessive-yield shares will be notably useful in supplementing earnings after retirement. A $120,000 funding in shares with a median dividend yield of 5% creates a median of $500 a month in dividends.

Freehold Royalties Ltd. (FRHLF) is a part of our ‘Excessive Dividend 50’ collection, which covers the 50 highest-yielding shares within the Positive Evaluation Analysis Database.

We have now created a spreadsheet of shares (and carefully associated REITs, MLPs, and many others.) with dividend yields of 5% or extra.

You may obtain your free full checklist of all securities with 5%+ yields (together with essential monetary metrics akin to dividend yield and payout ratio) by clicking on the hyperlink under:

Subsequent on our checklist of high-dividend shares to overview is Freehold Royalties Ltd. (FRHLF).

Enterprise Overview

Freehold Royalties Ltd. is a Calgary-based vitality royalty firm that acquires and manages royalty and mineral title pursuits in oil, pure fuel, and pure fuel liquids throughout Western Canada and the US. The corporate focuses on high-quality, liquids-heavy belongings in premier basins, together with the Permian, Midland, and Eagle Ford within the U.S., and Mannville, Clearwater, and southeast Saskatchewan in Canada.

Its enterprise mannequin generates income via royalties, lease bonuses, and manufacturing from third-party operators, permitting Freehold to learn from oil and fuel manufacturing with out immediately working wells.

The corporate’s portfolio emphasizes progress and resilience, with U.S. belongings delivering increased per-well manufacturing and Canadian belongings offering regular oil-weighted volumes. Freehold maintains a robust stability sheet, persistently pays dividends, and invests in strategic mineral acquisitions and lively leasing applications.

By specializing in liquids-rich, long-life belongings and investment-grade operators, Freehold goals to ship enticing, risk-adjusted returns whereas mitigating publicity to commodity value volatility.

Supply: Investor Relations

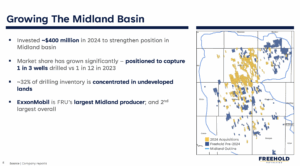

Freehold Royalties delivered $78 million in income and $57 million in funds from operations ($0.35/share) in Q2 2025. Complete manufacturing rose 2% from the earlier quarter to 16,584 boe/d, with a liquids weighting of 67%. U.S. belongings drove progress, whereas Canadian oil performs in Mannville, Clearwater, and southeast Saskatchewan contributed to a ten% year-over-year enhance.

The corporate signed 40 new leases and drilled 271 gross wells (45 in Canada, 226 within the U.S.), whereas investing $12 million in mineral title acquisitions within the Midland and Delaware basins. Bonus and lease revenues reached $1.9 million for the quarter, up 50% from earlier data.

Freehold maintained a robust stability sheet with $271 million in internet debt (1.1× FFO) and paid $44 million in dividends ($0.27/share). Realized costs averaged $50.36/boe, with a 31% premium for U.S. manufacturing, reflecting the energy of its liquids-heavy, royalty-focused portfolio regardless of decrease oil costs.

Progress Prospects

Freehold Royalties’ progress prospects are carefully tied to the efficiency of its liquids-heavy royalty portfolio and the broader oil and fuel market. Traditionally, the corporate earned close to C$1/share yearly through the late 2000s and early 2010s, when crude costs had been round $100/barrel.

Nevertheless, the collapse in oil costs in 2015 sharply decreased profitability, and Freehold struggled to generate significant earnings between 2015 and 2020. Since then, the corporate has strengthened its portfolio via acquisitions in premium U.S. basins and lively leasing applications, boosting manufacturing and money stream regardless of commodity value volatility.

Dividend sustainability and future progress stay linked to money stream reasonably than accounting earnings, as royalties are paid from operational money reasonably than internet earnings. Whereas Freehold has a historical past of sustaining excessive dividends relative to earnings, previous cuts in 2016 and 2020 illustrate the vulnerability of payouts throughout downturns.

The present month-to-month dividend of C$0.09 ($0.77 yearly) gives a gentle return, nevertheless it could possibly be decreased throughout extended recessions. Wanting forward, Freehold’s deal with high-quality, long-life liquids belongings, coupled with strategic U.S. acquisitions, positions the corporate to generate secure money stream and potential progress, although publicity to commodity cycles stays a key danger.

Supply: Investor Relations

Aggressive Benefits & Recession Efficiency

Freehold Royalties’ aggressive benefit lies in its liquids-heavy, royalty-focused portfolio throughout premier North American basins. By proudly owning royalty and mineral title pursuits reasonably than working wells, the corporate advantages from manufacturing upside whereas avoiding the excessive capital and working prices of conventional oil and fuel producers.

Its strategic deal with high-quality U.S. and Canadian belongings, mixed with lively leasing applications and selective acquisitions, gives publicity to long-life reserves, increased nicely productiveness, and premium pricing for liquids, giving Freehold a resilient money stream base relative to friends.

Regardless of these benefits, Freehold’s efficiency stays delicate to commodity value cycles. Throughout recessions or intervals of low oil costs, akin to in 2015 and the 2015–2020 downturn, the corporate’s profitability and dividend funds had been materially impacted. Whereas Freehold’s royalty mannequin buffers it from direct working dangers, dividends are in the end funded by money stream, making payouts weak throughout extended market weak point.

Nonetheless, its diversified, high-quality portfolio and deal with liquids-rich belongings assist mitigate downturns, supporting extra secure operations and positioning the corporate for restoration when market situations enhance.

Dividend Evaluation

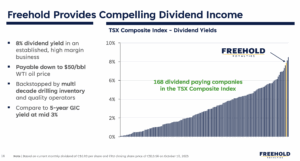

Freehold Royalties at the moment gives a excessive dividend yield of seven.4%, considerably above the 1.2% yield of the S&P 500, making it enticing for income-focused traders. Nevertheless, the dividend is weak because of the cyclical nature of the oil and fuel trade.

Earnings have declined sharply from a 10-year excessive of $1.03 per share in 2022, pushing the payout ratio from 68% to 90%, a stage that’s unsustainable over the long run.

The corporate has minimize its dividend in three of the final ten years, highlighting the danger to earnings throughout market downturns. U.S. traders also needs to take into account the impression of foreign money fluctuations on dividend funds.

From a valuation perspective, Freehold Royalties trades at 18.6 occasions trailing earnings, above an assumed honest P/E of 14.0. If the inventory reverts to this honest valuation over the following 5 years, it might create a -5.0% annualized drag on returns.

Mixed with flat earnings and the present dividend yield, the inventory is predicted to ship solely round 2.4% common annual complete return, suggesting that traders could also be higher served by ready for a decrease entry level to enhance the margin of security and potential long-term returns from this extremely cyclical firm.

Supply: Investor Relations

Closing Ideas

Freehold Royalties stands out for its robust manufacturing and reserve progress potential, an above-average dividend yield of seven.4%, and a strong stability sheet, making it interesting to income-focused traders.

Nevertheless, the corporate’s efficiency has traditionally been risky resulting from cyclical oil and fuel markets, and the inventory seems totally valued at present ranges. Traders could also be higher served ready for a extra enticing entry level.

Excessive-Yield Particular person Safety Analysis

Different Positive Dividend Assets

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

{kind=link}