Printed on October thirtieth, 2025 by Felix Martinez

Excessive-yield shares pay out dividends which are considerably greater than the market common. For instance, the S&P 500’s present yield is just ~1.2%.

Excessive-yield shares might be significantly useful in supplementing revenue after retirement. A $120,000 funding in shares with a mean dividend yield of 5% creates a mean of $500 a month in dividends.

Bridgemarq Actual Property Providers Inc. (BREUF) is a part of our ‘Excessive Dividend 50’ sequence, which covers the 50 highest-yielding shares within the Certain Evaluation Analysis Database.

We’ve created a spreadsheet of shares (and intently associated REITs, MLPs, and so forth.) with dividend yields of 5% or extra.

You may obtain your free full listing of all securities with 5%+ yields (together with essential monetary metrics resembling dividend yield and payout ratio) by clicking on the hyperlink beneath:

Subsequent on our listing of high-dividend shares to evaluate is Bridgemarq Actual Property Providers Inc. (BREUF).

Enterprise Overview

Bridgemarq Actual Property Providers helps residential actual property brokers and REALTORS throughout Canada by offering info, instruments, and companies that improve their operations. Working beneath the Royal LePage, By way of Capitale, Johnston, and Daniel manufacturers, the corporate, previously often called Brookfield Actual Property Providers, rebranded as Bridgemarq in 2019. Based in 2010, Bridgemarq is headquartered in Toronto.

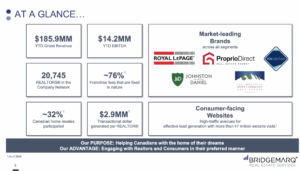

The corporate generates income via mounted and variable franchise charges from a community of practically 21,000 REALTORS. Roughly 81% of those charges are mounted, offering steady, predictable money flows which are additional secured by long-term contracts. Bridgemarq maintains sturdy accomplice relationships, as mirrored in its traditionally excessive renewal price of 96%. Royal LePage franchise agreements, representing 96% of the corporate’s REALTORS, span 10 to twenty years, making certain vital money stream visibility.

Bridgemarq holds a number one place within the Canadian market, collaborating in over 70% of nationwide residence resales. Its model fame and technological benefits entice franchisees and reinforce its market dominance. Nonetheless, the corporate was considerably impacted by the 2020 pandemic-induced recession, with earnings per share falling 47%, from $0.34 in 2019 to $0.18 in 2020.

Supply: Investor Relations

The corporate reported Q2 2025 income of $108.0 million, barely beneath final 12 months’s, whereas year-to-date income rose to $186.0 million, pushed by acquisitions and better franchise charges. Adjusted Web Earnings had been $2.2 million, with Free Money Stream of $3.6 million. The corporate declared a month-to-month dividend of $0.1125 per share, sustaining its $1.35 annual goal.

The corporate posted a web lack of $5.4 million ($0.57 per share), pushed by a $4.9 million loss on Exchangeable Items, partially offset by decrease curiosity and depreciation. Working money stream fell to $5.9 million attributable to greater curiosity prices and dealing capital adjustments, whereas Adjusted Web Earnings and Free Money Stream edged down from 2024.

Bridgemarq added about 600 gross sales representatives to its Royal LePage community, strengthening its presence in key markets. Regardless of a 4% year-over-year decline within the Canadian housing market, exercise improved in Quebec and a few metro areas, supported by steady rates of interest and managed inflation.

Progress Prospects

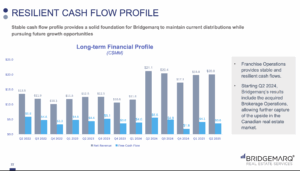

Over the previous decade, Bridgemarq has developed from a pure franchise operator to a extra built-in actual property platform. Traditionally, its income got here from steady mounted and variable franchise charges, offering regular money stream even throughout downturns just like the COVID-19 pandemic. Latest strikes, together with the 2024 acquisition of brokerage operations and the internalization of administration, have expanded the corporate into direct actual property gross sales and eradicated third-party charges, strengthening its operational management and cash-generating capabilities. Regardless of volatility in EPS, largely pushed by non-cash objects resembling exchangeable unit revaluations, the underlying enterprise has constantly supported its dividend.

Wanting forward, progress prospects are restricted. Elevated working prices, dangers from integrating latest acquisitions, and uncertainty within the Canadian housing market make EPS and dividend progress unlikely. Bridgemarq has maintained a steady month-to-month dividend of CAD $0.1125 since 2017, reflecting consistency fairly than progress. Whereas the corporate stays cash-generative, traders ought to anticipate stability fairly than vital near-term earnings or dividend progress.

Supply: Investor Relations

Aggressive Benefits & Recession Efficiency

Bridgemarq’s aggressive edge comes from its giant community of over 21,000 REALTORS, supported by sturdy manufacturers like Royal LePage and By way of Capitale. Its mixture of franchise and corporately owned brokerages, long-term franchise agreements, and superior expertise instruments ensures predictable money stream, excessive agent loyalty, and market dominance.

The corporate has confirmed resilient throughout recessions, together with the COVID-19 downturn. Its reliance on mounted franchise charges and cash-generative operations has allowed it to maintain dividends and keep stability, even when earnings fluctuate attributable to non-cash accounting objects.

Dividend Evaluation

Bridgemarq affords a excessive dividend yield of 9.9%, far above the 1.2% S&P 500 yield, making it engaging for income-focused traders. U.S. traders ought to notice that dividends are affected by the CAD/USD alternate price.

Nonetheless, the corporate’s payout ratio is excessive at 98%, and its web debt of $182 million exceeds its market cap, signaling a weak stability sheet. The dividend has been primarily flat over the previous 9 years, so significant progress is unlikely.

Supply: Investor Relations

Ultimate Ideas

Bridgemarq offers steady revenue via a resilient, fee-based actual property platform, however its restricted progress potential and sensitivity to the housing market place it extra as a yield-focused funding than a progress alternative. We venture annualized returns of 6.6%, pushed largely by the present dividend yield however partially offset by potential valuation pressures.

Given the speculative nature of latest acquisitions and the internalization of administration, mixed with the absence of latest dividend will increase, we keep a promote score on the inventory.

Excessive-Yield Particular person Safety Analysis

Different Certain Dividend Sources

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to help@suredividend.com.