")

Antoine2K/iStock through Getty Photographs

All monetary numbers on this article are in Canadian {dollars} until famous in any other case.

Introduction

It is time to discuss two associated issues: geopolitics and the Cameco Company (NYSE:CCJ).

On June 18, I wrote an article titled The Nuclear Increase – What To Make Of Cameco’s New Inventory Worth Excessive? In that article, I mentioned the brand new upswing in world uranium demand and the corporate’s essential place within the Western provide chain – particularly in mild of dependence on uranium imports from nations that may be thought of to be much less pleasant to Western nations.

Since then, CCJ shares have added 17%, bringing the entire return of this uranium big to 65% on a year-to-date foundation!

Now, we’re taking issues to the following degree, fueled by geopolitics.

On this article, I will replace my bull case and clarify why CCJ stays in a terrific house to gas the power calls for of the West for a lot of many years to come back.

So, let’s get to it!

Geopolitics As A Basic Driver

I am not a geopolitical knowledgeable. Whereas I steadily talk about geopolitics on podcasts and numerous interviews, I have a tendency to stay to some key issues/developments that I monitor when making funding choices.

This contains the larger image. For uranium, the larger image is fairly clear. If Western nations need to enhance nuclear power output, they’re depending on a really unstable provide chain.

In Might, the Wall Avenue Journal wrote an article highlighting a few of these developments.

Wall Avenue Journal

In keeping with the paper, nuclear energy is experiencing a resurgence within the Western world, with new reactors rising in the USA and Europe, pushed by the necessity for cleaner power sources and a want to scale back dependence on Russian oil and gasoline.

Nonetheless, a big problem lies forward—the Western nations lack the mandatory nuclear gas assets and manufacturing capability.

Notably, a considerable portion of crucial nuclear gas substances is sourced from Russia’s state monopoly, Rosatom, which has raised considerations on account of its involvement within the Ukraine battle.

Bloomberg

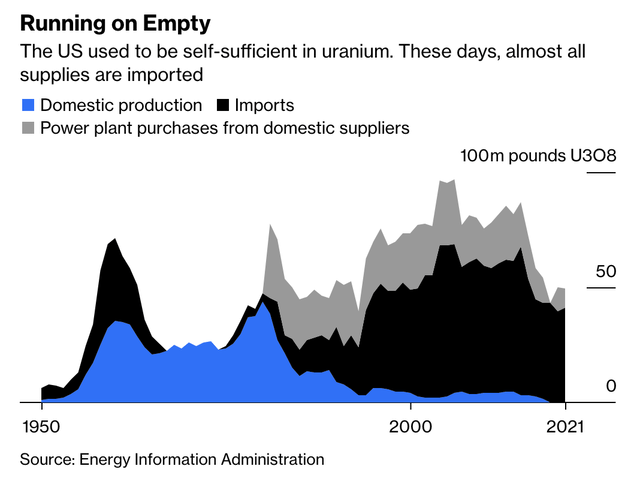

The origin of the West’s dependence on Russian nuclear gas dates again to a 1993 deal often known as Megatons to Megawatts, which aimed to transform extremely enriched uranium from Russian warheads into reactor gas.

Whereas this program efficiently decreased nuclear weapon stockpiles, it led to a state of affairs the place Russia grew to become the dominant provider of enriched uranium on the earth.

Because the chart above reveals, because the Nineteen Nineties, the U.S. has grow to be fully depending on imports.

Final month, Bloomberg columnist Javier Blas elaborated on these points.

Bloomberg

Russia’s affect goes properly past its personal manufacturing. In any case, identical to the U.S., Russia has lots of connections to different nations that can take heed to its calls for.

This contains numerous African nations, as Russia is attempting to win affect in that continent.

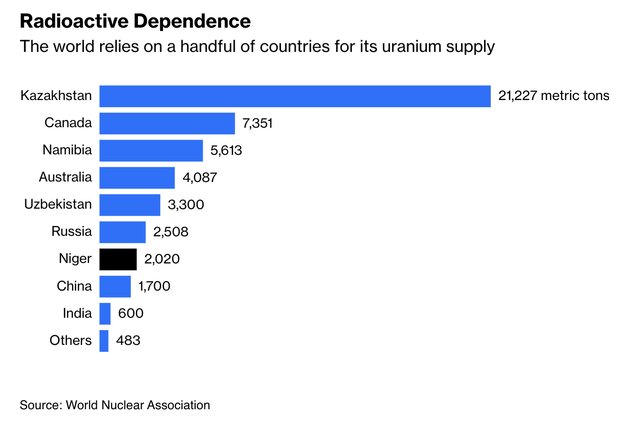

On August 1, I tweeted that the more and more difficult state of affairs in Niger is a cause to look at Cameco. In any case, that is the place France will get most of its uranium.

Twitter/X (@Growth_Value_)

Keep in mind that France generates 70% of its electrical energy from nuclear power!

Going again to Javier Blas’ feedback, he wrote that the Kremlin’s propaganda machine has fueled anti-French and American sentiment throughout the Sahel area, resulting in a collection of political upheavals since 2020.

For instance, pro-coup demonstrations in Niger’s capital, Niamey, have seen the show of the Russian flag, signaling Russia’s rising affect within the area.

If Niger had been to fall beneath Russian affect, the world’s dependence on Moscow for atomic power would enhance considerably, given Russia’s substantial uranium conversion and enrichment capabilities.

When mixed with different main uranium-producing nations like Kazakhstan and Uzbekistan, this might end in over 60% of the world’s uranium provide being managed by Russia and its shoppers.

Bloomberg

Evidently, that is an enormous deal!

Russia holds an almost 45% share of the worldwide marketplace for uranium conversion and enrichment, which poses a strategic vulnerability for nations like the USA and its companions – together with France and everybody seeking to escape rising fossil gas costs by switching to nuclear power.

All of that is excellent news for CCJ.

CCJ Stays In A Prime Spot

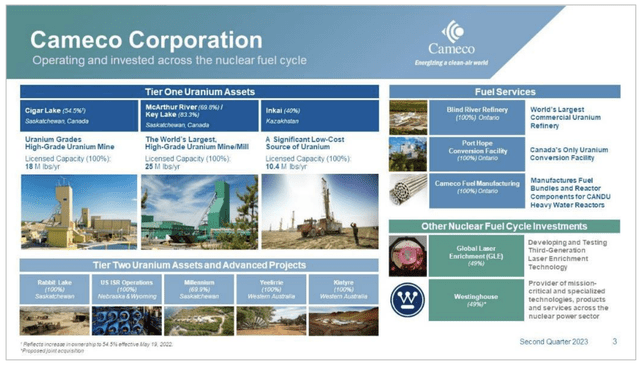

With a $16 billion market cap in New York, Cameco is the world’s largest publicly traded uranium producer. The corporate has main mining operations in North America, Australia, and Kazakhstan, together with the world’s largest uranium mine, McArthur River-Key Lake, in northern Saskatchewan (Canada).

Cameco Corp.

It goes with out saying that the corporate is properly conscious of the numerous tailwinds benefiting its firm. This contains electrification, decarbonization, and headwinds like geopolitics, power disruptions, and many years of underinvestment.

Cameco Corp.

This case is hard (to place it mildly), as we’re basically attempting to exchange 85% of the present power provide with clear options whereas attempting to carry 1/third of the worldwide inhabitants out of poverty.

Between 2050 and 2021, electrical energy demand might rise by as much as 80%.

So, even with out further disruptions, the world is taking a look at a widening provide hole for a few years to come back, benefiting future uranium costs.

Cameco Corp.

Throughout its 2Q23 earnings name, the corporate elaborated on these developments, because it famous the growing world help for nuclear energy, pushed by authorities insurance policies and company choices.

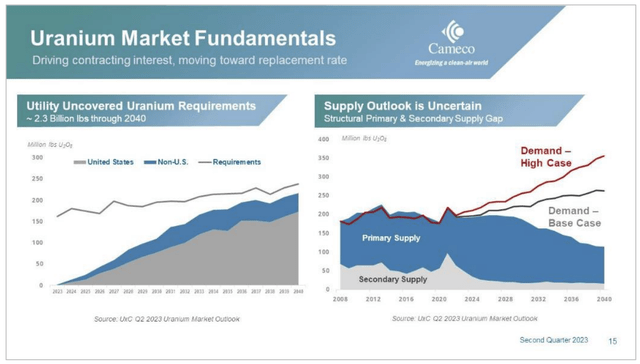

With demand development trying extra sturdy than ever and with the business expectation that by 2030 each major and secondary provides is not going to be adequate, the business must put money into extra capability. However increasing or constructing new capability throughout the gas cycle will take time.

[…] Along with manufacturing challenges, let’s not overlook the geopolitical uncertainties are resulting in considerations about origin of provide. Some utilities are searching for to exclude Russia of their future contracting choices. And there is all the time the continuing threat of formal sanctions. Then tied to the origin threat, there was a latest reminder that shifting nuclear materials across the globe to numerous factors within the gas cycle can be tougher than it as soon as was.

[…] Utilities are beginning to contract now to cowl their necessities 2030 and past, which is what we imply after we say we’re in a long-term contracting cycle right now.

– CCJ 2Q23 Earnings Name

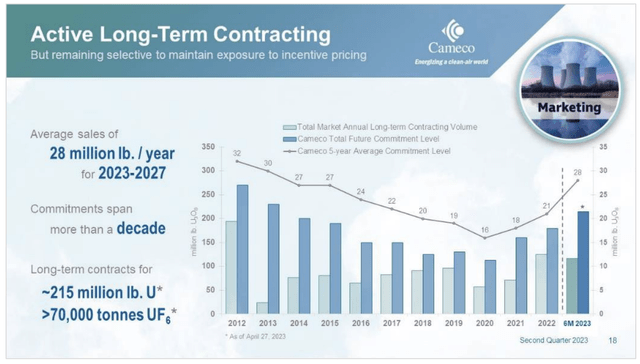

Thanks to those tailwinds, over the following 5 years, the typical supply quantity is projected to extend from 26 million kilos per 12 months to twenty-eight million kilos per 12 months.

Cameco Corp.

This development is attributed to the interpretation of beforehand introduced accepted volumes into executed contracts.

Moreover, the corporate holds supply commitments that stretch past a decade, with some contracts extending out to 2040.

Cameco additionally has a considerable and increasing pipeline of contracting discussions in progress.

Cameco Corp.

I do know what you are considering proper now. Is not long-term contracting a significant concern for an environment friendly pricing technique?

Cameco is not committing to future costs.

The corporate is pursuing market-related pricing mechanisms for these contracts.

Which means contract costs shall be based mostly on the long run value of uranium, probably together with ground value safety and ceilings.

In any case, the corporate’s purpose is to take care of publicity to future incentive costs, which is able to incentivize funding in new provide to satisfy long-term demand.

This method supplies flexibility to profit from potential value will increase whereas additionally providing sturdy draw back safety in opposition to macroeconomic or business headwinds.

Given the long-term business tailwinds, it is a unbelievable technique.

Cameco can be boosting its output to answer increased world demand.

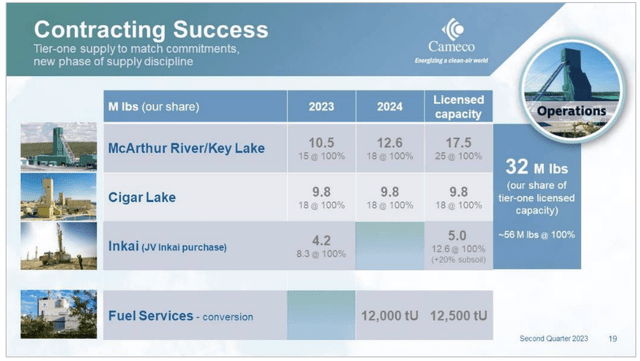

Throughout its second-quarter earnings name, Cameco highlighted its flexibility in managing uncovered necessities and its current Tier 1 property.

The corporate retains the choice to develop and lengthen manufacturing at these property, probably growing its annual share of Tier 1 uranium provide to roughly 32 million kilos.

Nonetheless, for Tier 2 property, Cameco plans to maintain them on care and upkeep until it will possibly safe long-term contracts that supply returns much like these achievable with Tier 1 property.

This strategic method to contracting and manufacturing is predicted to result in improved earnings and money movement, bringing the corporate again to Tier 1 run charges.

It additionally has a wholesome stability sheet.

Within the second quarter, the corporate reported $2.5 billion in money, $1 billion in complete debt, and a $1 billion undrawn credit score facility.

In different phrases, the corporate is web money optimistic.

Valuation

The valuation is hard. In any case, we’re coping with a bull case that’s anticipated to see growing provide shortages for a few years sooner or later. This warrants an elevated valuation – however how a lot is truthful?

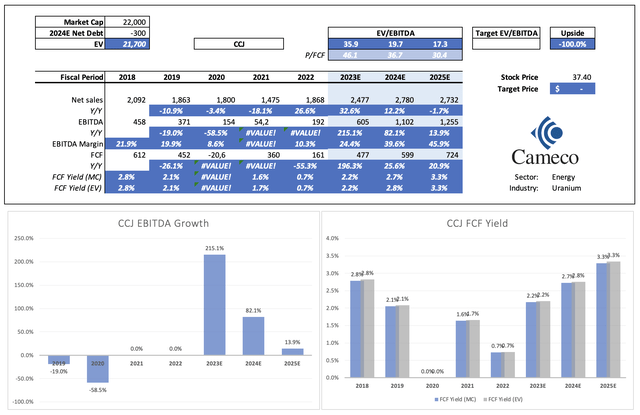

Utilizing estimates till 2025, the corporate is buying and selling at 17.3x 2025E EBITDA. It is usually free money movement optimistic, with sturdy EBITDA development in each 2024 and 2025. Personally, I anticipate that EBITDA development will develop into a lot increased within the years forward, as I consider that we’re seeing geopolitical shifts that put a good greater emphasis on provide from CCJ and its allies.

Leo Nelissen (Based mostly on analyst estimates)

The present consensus value goal for NY-listed shares is $38, which is simply 2% above the present value.

Whereas I don’t recommend that buyers chase the worth at present ranges, I consider that CCJ is poised for a long-term uptrend – particularly if my oil and gasoline thesis seems to be right, which might put a good greater emphasis on the return to nuclear.

Once more, I’d look ahead to a correction earlier than leaping in and consider that we might see $50 – $60 inside 12–24 months.

Takeaway

In a world formed by geopolitical complexities and an pressing want for clear power, the Cameco Company emerges as a stellar participant within the uranium market.

As I’ve mentioned in prior articles as properly, Western nations discover themselves topic to an unstable provide chain closely reliant on Russia, which is elevating considerations about power safety.

CCJ, with its place because the world’s largest publicly traded uranium producer, capitalizes on these dynamics. Its strategic method to contracting and manufacturing, versatile pricing mechanisms, and sturdy stability sheet place it as a powerful participant in assembly the surging demand for nuclear power.

Whereas valuing CCJ is a problem, given the provision shortages looming on the horizon, it is clear that this firm holds monumental potential.

Whereas I do not advocate chasing present costs, CCJ seems primed for a long-term uptrend, particularly if the shift away from fossil fuels continues.

A correction could current an entry level, however do not be shocked if we see CCJ attain $50 to $60 inside the subsequent 12–24 months.