")

izusek

We beforehand lined Genco Delivery & Buying and selling Restricted (NYSE:GNK) in October 2023, discussing its glorious dividend prospects then, due to the extremely competent administration workforce, more healthy steadiness sheet, and decreased working bills.

Mixed with its improved Capesize TCE charges in comparison with the dry bulk spot charges and its pre-pandemic charges, we had continued to price the inventory as a Purchase then.

On this article, we will talk about why the GNK inventory has been briefly downgraded to a Maintain now, with the rising optimism embedded in its inventory valuations and costs doubtless providing minimal returns forward.

Mixed with the again loaded FQ4’23 reserve steering of $19.5M, the dry bulker’s dividend funding thesis could also be briefly disappointing certainly.

The Dry Bulk Funding Thesis Stays Optimistic – However You Could Have Missed The Boat

For now, GNK has reported impacted FQ3’23 voyage revenues of $83.36M (-7.9% QoQ/ -38.7% YoY), adj EBITDA of $14.6M (-51.3% QoQ/ -75.7% YoY), and adj EBITDA margins of 17.5% (-15.6 factors QoQ/ -26.8 YoY).

A lot of the headwind is attributed to the underwhelming fleet-wide TCE charges of $12.08K (-22.3% QoQ/ -48.8% YoY) and rising Each day Vessel Working Bills [DVOE] of $6.11K per vessel (+8.3% QoQ/ +12.1% YoY), with $6K of DVOE projected in FQ4’23 (-1.8% QoQ/ +18.4% YoY).

With bills rising and contracted TCE charges falling, it’s comprehensible why its backside line era has been negatively affected, although a part of the bills are attributed to one-time prices.

Alternatively, readers should additionally word that GNK’s revenues are largely uncovered to the spot market-related time charters at $55.45M (+21.5% QoQ/ -27.3% YoY), or the equal 66.5% of its whole voyage revenues within the newest quarter (-16.2 factors QoQ/ -22.7 YoY).

With the administration already guiding an estimated FQ4’23 fleet-wide TCE charges of $16.66K (+37.9% QoQ/ -13.8% YoY), due to the rising Capesize charges of $20.83K (+35% QoQ/ +8.3% YoY) and Extremely/Supra charges of $14.63K (+49.5% QoQ/ -43.4% YoY), it seems that we might even see glorious subsequent quarter outcomes forward.

That is on prime of the increasing Baltic Dry Index [BDI] to $1.5K as of January 24, 2024, up by +8.6% from the November 2023 backside of $1.38K, by +15.3% from the January 2024 backside of $1.3K, and by +10.2% the 2019 common of $1.36K.

These numbers suggest that we might even see GNK file a equally glorious efficiency in FQ1’24, with the BDI showing to carry regular over the previous week.

Whereas the continued Purple Sea debacle has but to unfold to the dry bulk business, with 7% of the worldwide dry bulk delivery probably affected within the intermediate time period, we might even see the elevated BDI/ TCE charges persist for a bit of longer till these points are resolved.

That is on prime of the doubtless longer mileage for a part of GNK’s future voyage, with Genco Picardy already focused twice on the time of writing.

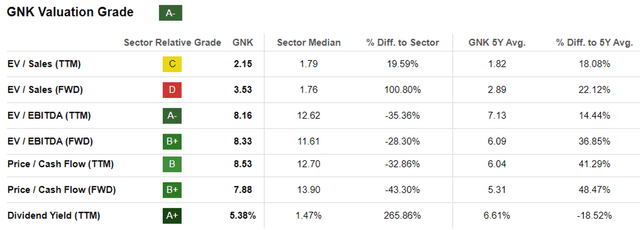

GNK Valuations

Looking for Alpha

And it’s for these causes that we will perceive why Mr. Market has awarded the GNK inventory with the upper FWD EV/ EBITDA valuation of 8.33x and FWD Value/ Money Circulation valuation of seven.88x.

That is in comparison with its 1Y imply of 5.36x/ 4.50x and pre-pandemic imply of 5.79x/ 5.97x, although nonetheless lagging behind the sector median of 11.61x/ 13.90x, respectively.

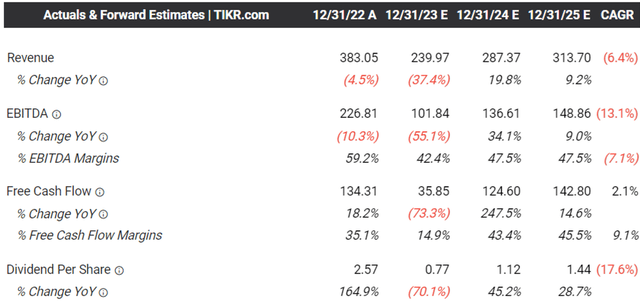

The Consensus Ahead Estimates

Tikr Terminal

Maybe that is attributed the optimistic consensus ahead estimates, with GNK anticipated to generate spectacular adj EBITDA margins of over ~40% by means of FY2025.

Whereas these numbers pale compared to the hyper-pandemic margins of almost ~60%, readers should word that these are a lot improved that its pre-pandemic averages of ~30%.

Most significantly, the GNK administration has made nice efforts to deleverage to a long-term debt state of affairs of $139.99M (-5.5% QoQ/ -19.1% YoY/ -66.1% from FY2019 ranges), apart from the brand new $500M revolving credit score facility.

This feat is spectacular certainly, regardless of the constant fleet renewal throughout its capability with a median age of 11.5 years as of November 27, 2023 (-0.2 years QoQ/ +0.8 YoY), in comparison with the 9.7 years reported in This autumn’19.

Because of this, we consider that GNK stays properly positioned to benefit from the TCE tailwinds, additional aided by the Fed’s supposed price pivot from Q1’24 onwards.

Although the method could also be extended, with the macroeconomic outlook anticipated to normalize solely by 2026, we consider that the dry bulker’s Efficient Curiosity Fee of 8.71% by the most recent quarter (+0.32 factors QoQ/ +3.37 YoY/ +3.4 from 2019 averages) might average from henceforth.

This may increasingly additionally carry down the dry bulker’s annualized curiosity bills from the $7.96M reported within the newest quarter (-6.5% QoQ/ -12.3% YoY), offering additional tailwinds to its backside line.

So, Is GNK Inventory A Purchase, Promote, or Maintain?

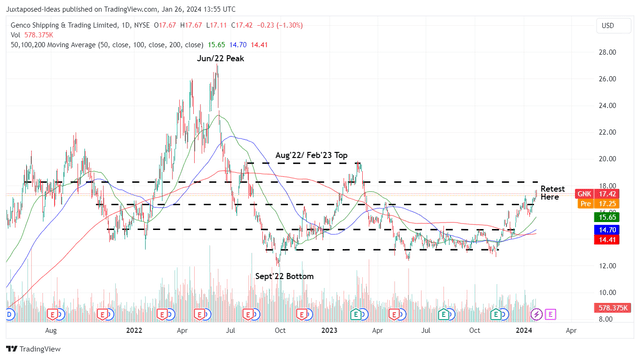

GNK 2Y Inventory Value

Buying and selling View

Because of these tailwinds, it’s also unsurprising that GNK has quickly damaged out of its 50/ 100/ 200 days transferring averages over the previous few weeks, with it prone to retest its subsequent resistance ranges of $18s within the near-term.

Then once more, right here is the place we need to warning traders, because it stays to be seen whether it is nonetheless a viable dividend funding thesis right here.

That is due to GNK’s narrowed projected ahead yield of three.4%, primarily based on its newest quarterly payout of $0.15 per share. This yield is notably decrease than its 4Y common yields of 8.37%, although nonetheless expanded from the sector median of 1.47%.

As well as, readers should additionally word that the administration has been adjusting their voluntary quarterly reserves from the mounted sum of $10.75M since FQ1’23 at $2.19M, FQ2’23 at $9.92M, and FQ3’23 at $4.4M to deal with shareholder payouts. This naturally impacts its money on steadiness sheet to $48.63M (-6.4% QoQ/ -31.7% YoY) by the most recent quarter.

Mixed with the administration’s back-loaded FQ4’23 reserve steering of $19.5M, anybody hoping for an enormous payout within the upcoming quarter should mood their expectations certainly.

Because of these elements, the GNK inventory is barely appropriate for present traders seeking to DRIP.

In any other case, we urge new traders to attend for a average retracement, because of the decreased danger/ reward ratio at present ranges and potential returns, in comparison with the US Treasury Yields of between 4.03% and 5.35%.