shisheng ling/E+ by way of Getty Photos

Elevator Pitch

I price Full Truck Alliance Co. Ltd. (NYSE:YMM) inventory as a Maintain. Beforehand, I wrote about YMM’s close to time period monetary prospects and its long run monetary targets in my June 20, 2023 initiation article.

My consideration turns to Full Truck Alliance’s newest quarterly leads to the present replace. YMM’s precise This fall 2023 working earnings failed to satisfy the market’s expectations resulting from higher-than-expected gross sales and advertising prices. The corporate’s gross sales and advertising bills may stay elevated going ahead, although its Q1 2024 income steerage was favorable. Making an allowance for each its high line progress steerage and its price outlook, I depart my Maintain ranking for Full Truck Alliance unchanged.

YMM’s This fall Working Revenue Miss Was Under Consensus Estimate

On March 7, 2024 earlier than the market opened, Full Truck Alliance revealed its monetary efficiency for the fourth quarter of 2023 with an earnings press launch.

The corporate’s normalized working revenue decreased by -13% QoQ from RMB458.5 million for Q3 2023 to RMB398.8 million in This fall 2023 as disclosed in its earnings launch. Extra importantly, Full Truck Alliance’s newest fourth quarter normalized working earnings got here in -13% decrease than the market’s consensus forecast of RMB458.3 million (supply: S&P Capital IQ).

Individually, YMM’s high line expanded by +25% YoY and +6% QoQ to RMB2,408.0 million within the ultimate quarter of the earlier 12 months. In its earnings launch, Full Truck Alliance cited “a quickly rising consumer base and order quantity” as the important thing causes for the rise in its high line. The corporate had achieved a +5% income beat for This fall 2023 as in comparison with the promote facet’s consensus gross sales estimate of RMB2,303.0 million as per S&P Capital IQ information. This means that Full Truck Alliance’s This fall 2023 working earnings miss wasn’t pushed by below-expectations income progress.

It was higher-than-expected bills that led to Full Truck Alliance’s precise fourth quarter working revenue falling in need of the market’s consensus projection. Particularly, YMM’s gross sales and advertising prices rose by +50% YoY and +45% QoQ to RMB421.0 million within the final quarter of the prior 12 months. Because of the sharp improve in gross sales and advertising bills, the corporate’s This fall 2023 normalized working margin of 16.6% turned out to be -3.3 share factors under the analysts’ consensus working margin forecast of 19.9% (supply: S&P Capital IQ).

Full Truck Alliance defined on the firm’s This fall 2023 earnings name that larger “investments in advertising to amass new customers” and “model promotion to extend our model consciousness” contributed to the substantial progress in gross sales and advertising prices.

Good Q1 Income Steering Was Overshadowed By Unfavorable Value Outlook

YMM is anticipating to ship a high line of RMB2,135 million for Q1 2024 as per the mid-point of its steerage as indicated in its earnings launch. The corporate’s income steerage implies that Full Truck Alliance’s gross sales are projected to extend by +25% YoY in Q1 2024, which is identical tempo of YoY income growth that it registered for This fall 2023.

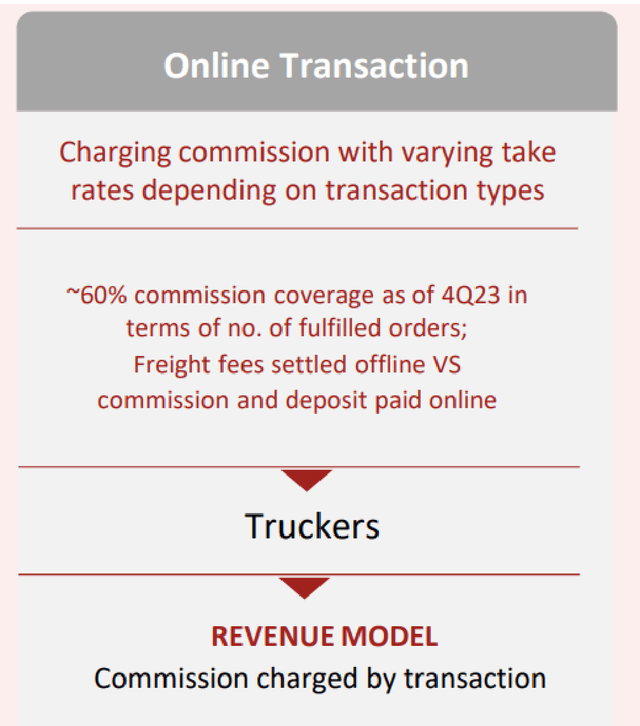

Transaction commissions had been the quickest rising income stream for YMM in This fall 2023, and that is prone to be the corporate’s key high line driver this 12 months.

Within the fourth quarter of final 12 months, the corporate’s transaction commissions grew by +44% YoY. As compared, Full Truck Alliance’s income generated by freight brokerage companies and freight itemizing companies elevated by +19% and +10%, respectively for the current quarter on a YoY foundation. Wanting forward, Full Truck Alliance guided at its This fall earnings briefing that its 2024 “fee income progress” might be “probably surpassing the expansion price that we achieved prior to now 12 months (2023)” contemplating that its “present fee charges are very conservative.”

Full Truck Alliance’s Transaction Commissions Income Mannequin

YMM’s Investor Presentation Slides

On the flip facet, elevated working prices would possibly proceed to weigh on Full Truck Alliance’s future profitability.

At its fourth quarter outcomes briefing, YMM outlined its expectations that it’s going to “improve our consumer acquisition efforts (for 2024) as compared with final 12 months.” The corporate additionally indicated at its newest quarterly earnings name that “within the longer run, we anticipate a continued improve in gross sales and advertising bills aligned with the growth of recent enterprise ventures.”

Contemplating the corporate’s below-expectations This fall 2023 working earnings and its forward-looking administration commentary, it’s affordable to be involved that YMM’s precise working revenue margins for brief time period and future may not be nearly as good as what buyers are hoping for.

Precise Share Repurchases Fell Quick Of Expectations

In its This fall 2023 earnings launch, Full Truck Alliance disclosed that it spent roughly $200 million on share buybacks between early-March 2023 and early-March 2024. In different phrases, YMM’s historic one-year buyback yield was round 3%, which I deem to be respectable however unappealing.

Notably, the corporate solely accomplished 40% of its one-year $500 million share buyback plan that was initiated in mid-March final 12 months.

Provided that the corporate had money and investments of $3.9 billion (or roughly 60% of market capitalization) on its steadiness sheet as of end-2023, it’s sensible to assume that Full Monitor Alliance has the monetary capability to be much more aggressive with its share repurchases.

Extra considerably, Full Truck Alliance’s conservatism on the subject of buybacks would possibly ship the message that the inventory’s present valuations at 12.9 instances (supply: S&P Capital IQ) consensus subsequent twelve months’ normalized P/E are affordable.

Concluding Ideas

Full Truck Alliance’s prospects are combined, which warrants a Maintain ranking.

On one hand, the corporate’s Q1 2024 high line progress steerage is nice. YMM anticipates that it might file a powerful +25% YoY improve in income for the primary quarter of this 12 months.

However, YMM expects to take a position extra in gross sales and advertising going ahead. This means there’s a significant danger that Full Truck Alliance’s precise Q1 2024 and full-year 2024 working earnings and working margins might not meet the analysts’ expectations.

{kind=link}