")

Vitezslav Vylicil

Creator’s Word: This text was printed on iREIT on Alpha in early July 2023.

Pricey subscribers,

It’s totally, very uncommon that you will discover me investing in any type of progress inventory. A inventory that doesn’t pay a dividend, or the attraction hinging fully on capital appreciation just isn’t an funding I make calmly, typically or with out having a transparent aim for the place or the corporate.

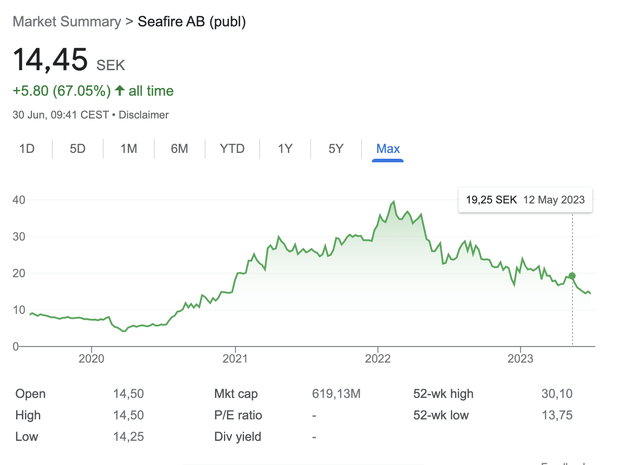

Nevertheless, usually, once I do progress investments, they are usually smaller corporations in glorious positions. One of many final progress inventory investments I made was a small firm often called Seafire AB. Not solely did I do know administration, however I had spent years following the corporate and its technique. I used to be assured that an funding would generate triple-digit RoR, and so I purchased a modest allocation, round $8000 value of shares, at close to a backside worth. I offered this throughout tech froth mania.

Seafire Inventory (Google Finance)

I ended up making over 400% on the funding. There are a number of the explanation why you do not see me speaking about such investments typically, or why you’ve by no means seen or heard about this one:

- Seafire is an organization that 90%+ of you can not spend money on, it is a Swedish enterprise with lower than $80M market cap. It has no ADR.

- Seafire is on no account consultant of the investments I make 99% of the time, and beginning to showcase such investments would possibly give individuals the flawed impression about how I make investments on a common degree.

- It was a small funding.

However I do, at occasions, spend money on progress shares.

And at present, I’ll present you a latest buy that I intend to broaden upon with time.

flatexDEGIRO (OTCPK:FNNTF) – A web-based dealer with a sensible upside

So, lots of chances are you’ll not know this, however Europe is pretty fragmented in terms of brokerages. There are native massive gamers – we use Nordnet and Avanza in Sweden and Scandinavia in some elements, however there aren’t any Schwabs (SCHW) which have a pan-European protection, or comparable dominance.

European market outperformed and on-line brokers that handle to indicate actual dominance are, due to this fact, doubtlessly fascinating to me. I like investing in brokers and in inventory market operators, as evidenced by my protection of Deutsche Börse (OTCPK:DBOEY) and comparable corporations. I “know” that the fitting firm doing on the European continent what IBKR (IBKR) is doing globally, would generate important revenue and returns – and that some areas that are undercover by IBKR, akin to Germany, France, and Southern European International locations are ripe for entry.

Subsequently, enter FlatexDEGIRO.

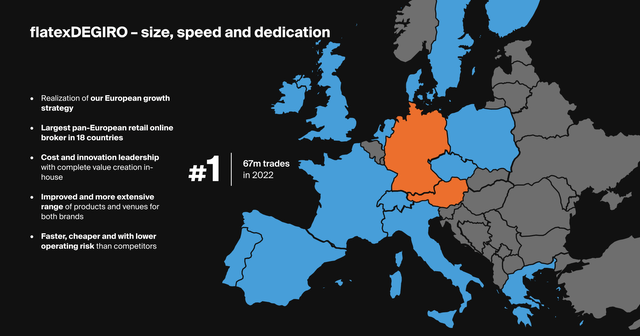

The corporate is the main and fastest-growing on-line dealer with 16 million prospects in 16 international locations. Flatex just lately bought DEGIRO, which signifies that the firm with a present market capitalization of lower than €1B handles 91M transactions on a yearly foundation, or a transaction quantity of €350B – and I consider this to be solely the start.

Flatex IR (Flatex IR)

So – 16 markets, 2.4M buyer accounts, 1,300 workers, €40B in belongings beneath custody, and over 65M LTM executed trades make this firm what it’s. It has an interesting income mannequin break up between on-line brokerage, credit score/treasury, and IT/providers, with brokerage being virtually 75% of the corporate’s revenues.

What makes this progress firm so a lot better than others?

What makes me cowl such an organization like this one?

Profitability.

As I’ve at all times stated, I concentrate on fundamentals and worth. So let’s start with fundamentals.

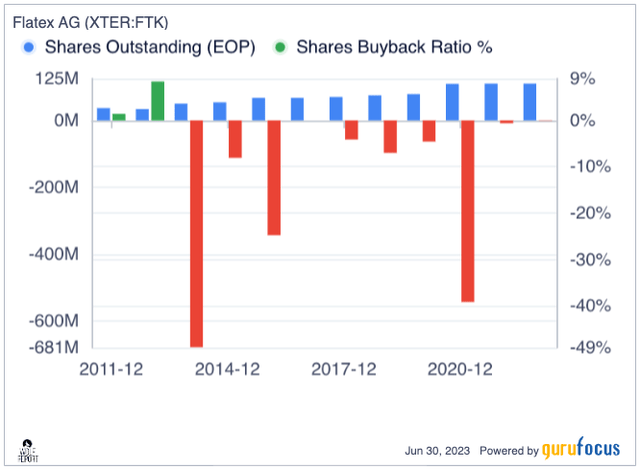

flatexDEGIRO has among the best ROCE numbers within the trade, and regardless of its present smaller scale, manages above-average profitability metrics when it comes to 67% gross margins, 32% working margin, and an almost 19% web margin. The corporate has a particularly low debt to EBITDA at 0.28x, among the best within the trade. Nevertheless, it is also ready to nonetheless problem substantial quantities of widespread shares at a comparatively continuous tempo.

Flatex SO (GuruFocus)

Nevertheless, the corporate has very a lot a working enterprise mannequin – and that is what I need to see once I spend money on an organization. It is the bread and butter of investing, and particularly in corporations which are small and comparatively new to the market. There are traders that spend money on unprofitable corporations hoping for a turnaround, however I’m not one in all them – not if the profitability points are well-established.

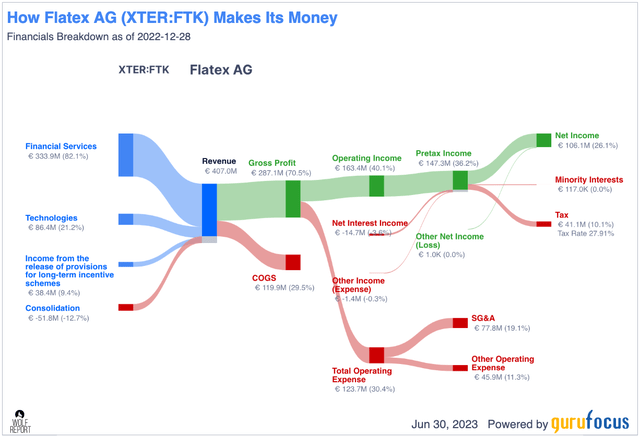

With this firm, regardless of its dimension and age, the enterprise is operating like a well-oiled machine already, churning out over 20% web margins for the 2022 interval.

Flatex income/web (GuruFocus)

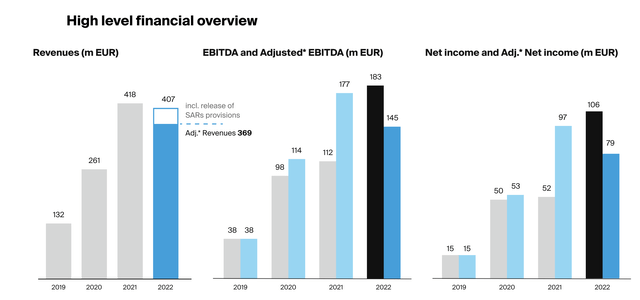

Like every on-line dealer, the corporate makes cash by commissions, margins and trades/curiosity and costs. Profitability has been a factor for Flatex for a number of years.

FlatexDegiro IR (FlatexDegiro IR)

As with most brokers, 2021 was the excessive yr with virtually 100M transactions and shutting in on €44B belongings beneath custody – however the firm remains to be rising, with virtually 500 000 web provides in prospects throughout 2022 alone. The corporate’s geographical protection could be very spectacular.

FlatexDegiro IR (FlatexDegiro IR)

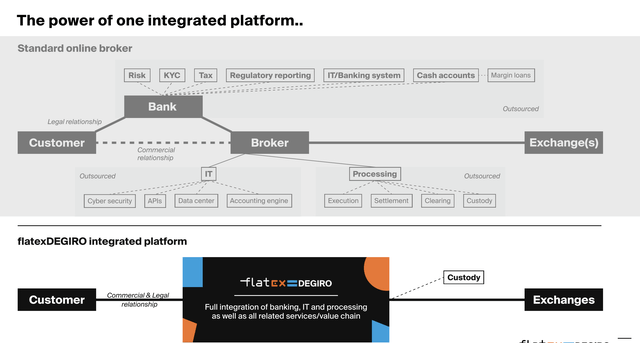

The corporate is an try to carry a number of in any other case complicated geographies collectively – and so they’re doing this very nicely up to now. What differentiates the corporate from different on-line brokerages is its full integration of banking, IT and processing in addition to all associated providers, in comparison with a regular dealer which must have banking contacts, authorized relationships, IT and processing relationships in a means that flatexDEGIRO doesn’t have.

FlatexDEGIRO IR (FlatexDEGIRO IR)

This allows scaling and edge in terms of prospects, as a result of it signifies that companions can combine seamlessly, together with funding banks, ETF suppliers, fund managers and others, which then have the power to hook up with a large European buyer base. The corporate has already gained all kinds of awards, meany of them in Germany.

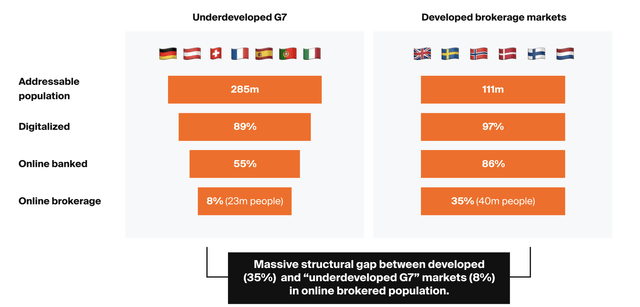

For these of you who have no idea this – most of Europe apart from Scandinavia, UK and Netherlands, are extraordinarily underdeveloped when it comes to brokers and funding/on-line brokerages. Solely 8% of individuals in France, Spain, Portugal, Italy, Germany, Austria and Switzerland use on-line brokerages – 23 million individuals. Within the developed aforementioned markets that quantity is 40M individuals, however that is 35% of the entire.

FlatexDEGIRO IR (FlatexDEGIRO IR)

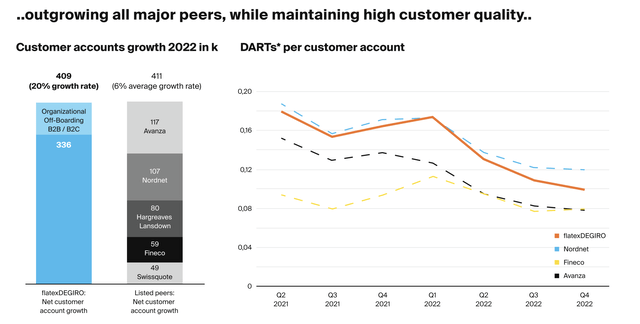

So there’s loads of room to develop for the corporate. And the extensive availability of data and rising curiosity in investing throughout Europe makes this the proper time to go deeper into one thing like this. We’re speaking about 285M individuals, a 100M buyer market assuming a LFL penetration to Scandinavia of 35%. The corporate is already main the cost a bit with zero fee buying and selling, clear pricing, and no cost dependency, with its core markets of Netherlands, Germany, and Austria – and the expansion markets are main the cost right here with important account progress that has resulted in outgrowing all main friends.

FlatexDEGIRO (FlatexDEGIRO)

As you’ll be able to see, my brokerage (Nordnet) is on that listing. I personally am not a Flatex buyer, as a result of the corporate would not provide me the personal banking attraction that Nordnet can – however I’m not essentially the corporate’s goal buyer. And in terms of goal prospects, the corporate is doing an excellent job.

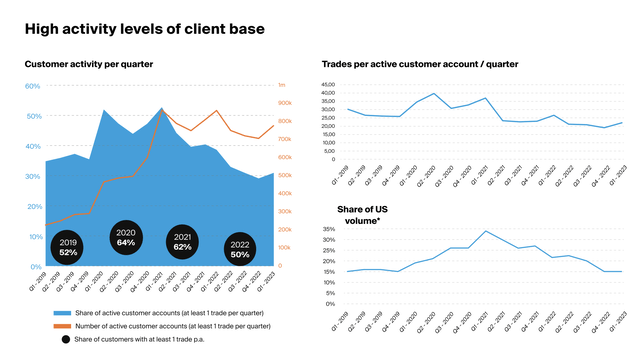

The corporate has an energetic consumer base that is rising, and there is nonetheless lots of room to develop the US quantity on the platform.

FlatexDEGIRO IR (FlatexDEGIRO IR)

The corporate’s month-to-month inflows have stayed very constant regardless of ECB price will increase. On the elemental aspect, the corporate is extraordinarily well-capitalized. What do I imply by this?

I imply that flatexDEGIRO has a CET1-requirement of 15.6%, and is shut to twenty% right here, with a leverage ratio of round 6.9%. There was a latest BaFin audit of the corporate which required the corporate to alter up some issues because of the speedy progress price.

In 2022, the German Federal Monetary Supervisory Authority (BaFin) has performed a particular audit at flatexDEGIRO in accordance with part 44 of the Kreditwesengesetz (KWG – German Banking Act), figuring out shortcomings in some enterprise practices and governance, with audit report offered in November 2022.

On account of the audit, BaFin will, amongst different issues, impose flatexDEGIRO to make sure acceptable enterprise group and has issued short-term capital surcharges. flatexDEGIRO has instantly initiated varied measures to adjust to the regulatory necessities inside a specified timeframe and can proceed to work carefully with BaFin. A bunch-wide regulatory program has been arrange at board degree and first measures had been applied, together with the appointment of Dr. Matthias Heinrich as new Chief Danger Officer at flatexDEGIRO Financial institution AG in addition to organizational modifications within the management of the interior controls, threat administration and regulatory reporting departments.

After some scandals in Germany on the monetary aspect, see Wirecard, german regulatory authorities are working exhausting to make sure that no such scandals or comparable ones are dedicated with an organization the place they’ve supervision. I don’t view the present state of affairs, or what’s described above as a serious or important threat in any means.

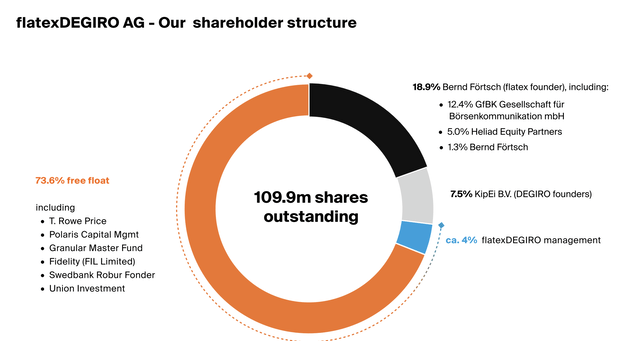

One other optimistic is the excessive quantity of inner shareholding we discover within the firm.

FlatexDEGIRO IR (FlatexDEGIRO IR)

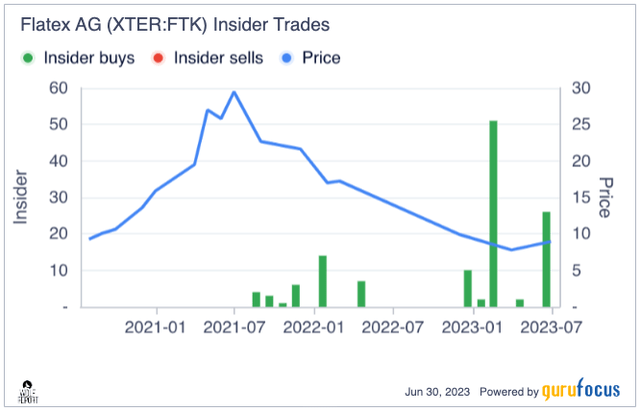

There may be lots of insider exercise as of late, with managers shopping for tons of of 1000’s of shares.

Flatex Insider shopping for (GuruFocus)

As I’ve stated earlier than, this doesn’t imply that the corporate is routinely a “BUY” or a “SELL”, however it does lend some credence to that some view the corporate as undervalued right here.

flatexDEGIRO is a ~€1B market cap Pan-European on-line brokerage with a superb market place. It has declined considerably for the previous 2 years, and I now view it ripe to spend money on, when you’re comfy with the danger/reward ratio – let’s make clear this right here subsequent.

flatexDEGIRO – Loads of Upside within the enterprise

I’m comfy, regardless of it being a progress enterprise, to forecast flatexDEGIRO based mostly on its earnings – not as a typical progress enterprise at a P/S a number of or at a share of income progress, or income multiples. The corporate has what’s my basic requirement for investing – and that’s revenue. It has good revenue.

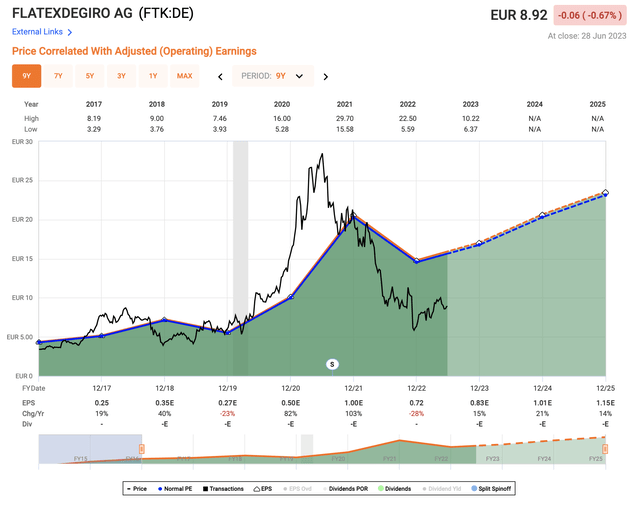

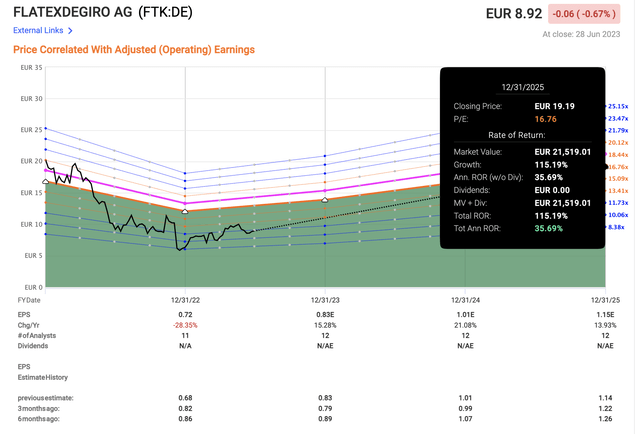

FlatexDEGIRO upside (F.A.S.T graphs)

The corporate had no enterprise buying and selling at 30-38x P/E which is also why I wasn’t within the firm on the time – and previous to 2021, I seen as being too new and unsure.

Now, I view it as being a possible for investing – and a reasonably good one, relying on how issues go within the close to time period. With normalization of buying and selling patterns and revenue, we must always see the corporate’s earnings get better this yr – and considerably, with 1Q23 outcomes already confirming at the very least a few of these indications and traits.

Within the case of normalization to a 16-20x P/E, which I view as related for a corporation with these profitability indicators, it is now doable to forecast triple-digit RoR on the idea of a 16.7x P/E for 2025E. I view this because the “base case” right here.

FlatexDEGIRO Upside (F.A.S.T graphs)

That upside may go as much as 150% if we see the corporate’s normalized premium coming again right here. Because of the firm’s restricted age, forecast accuracy is of some concern right here – we’ve got a 50% damaging miss ratio with a ten% margin of error from FactSet. (Supply: F.A.S.T Graphs)

S&P International road targets are fascinating. 11 analysts with a median of €10.93 observe the corporate, which means 6 have a “BUY” right here with a excessive of €16.6 and a low of €8.3. However lower than a yr in the past, that very same common PT was €32 with 7 out of 9 analysts at a “BUY” or equal ranking for the corporate, indicating an absence of long-term view for this firm, or considerably deteriorating enterprise situations. I do not view the latter as being related on this firm’s case – so the straightforward reality is, the corporate is being undervalued right here, as I see it.

flatexDEGIRO is without doubt one of the fastest-growing European brokerages, in a fragmented market the place different gamers have failed to realize traction for years, and the place the corporate would not have that a lot competitors in sure markets. I consider Scandinavia might be exhausting for the corporate to penetrate – we’re already an “Investing” individuals, and new entrants have a tough time pulling us from our incumbent banks or native brokerages – and these already provide very low commissions.

Nevertheless, there’s a particular case to be made for why the corporate may do nicely within the the rest of Europe – and that is what I am investing in right here. I spend money on Central European and Western European progress from a number of markets. I view €11 as too low for this firm within the long-term.

Based mostly on a mixture of adjusted EPS potential, projected FCF, P/S multiples, and what I view as a sensible and even conservative forecast, I might say lower than 16-17x P/E is just too low-cost for this firm long run. For 2023E, which means a PT of €16 is the logical solution to go right here.

That can be the place I put my preliminary worth goal for FlatexDEGIRO.

Right here is my preliminary thesis on the corporate.

Thesis

- flatexDEGIRO is a really uncommon breed – it is a progress firm that I think about investable based mostly on stable earnings, a basically sound and worthwhile enterprise mannequin, good potential outcomes for 2023-2025E, and good administration with a imaginative and prescient of turning this into a number one dealer in Europe.

- I am “on board” with this imaginative and prescient and technique. And that is the place I give the corporate my ranking of “BUY”, getting into with a PT of €16 and having purchased a stake representing 0.15% of my funding portfolio on the personal aspect.

- I count on to personal flatexDEGIRO for a number of years, and ultimately seeing triple-digit returns for this funding. That is how I spend money on progress shares – selecting worthwhile and well-managed corporations with what I see as a transparent future in a market that is not going wherever.

Keep in mind, I am all about:

- Shopping for undervalued – even when that undervaluation is slight and never mind-numbingly huge – corporations at a reduction, permitting them to normalize over time and harvesting capital positive aspects and dividends within the meantime.

- If the corporate goes nicely past normalization and goes into overvaluation, I harvest positive aspects and rotate my place into different undervalued shares, repeating #1.

- If the corporate would not go into overvaluation however hovers inside a good worth, or goes again right down to undervaluation, I purchase extra as time permits.

- I reinvest proceeds from dividends, financial savings from work, or different money inflows as laid out in #1.

Listed below are my standards and the way the corporate fulfills them (italicized).

- This firm is general qualitative.

- This firm is basically secure/conservative & well-run.

- This firm pays a well-covered dividend.

- This firm is at present low-cost.

- This firm has a sensible upside that’s excessive sufficient, based mostly on earnings progress or a number of growth/reversion.

The one situation the place I’m “okay” with shopping for a progress firm is when the corporate is qualitative, secure, low-cost, and with a sensible upside. flatexDEGIRO has this, and for these causes, it is a “BUY”.

Editor’s Word: This text discusses a number of securities that don’t commerce on a serious U.S. alternate. Please pay attention to the dangers related to these shares.