")

aluxum

Funding abstract

Following my Might report on Embecta Corp. (NASDAQ:EMBC), the inventory hasn’t garnered any extra demand and curled over to the draw back. it now trades 31% under my final article, and primarily based on this rigorous evaluation of the funding info, my evaluation reveals these developments might proceed. For a assessment of the final two EMBC publications, click on right here.

As a reminder, EMBC was fashioned as a carve-out from Becton, Dickinson (BDX) in April final yr, and has languished since its new itemizing. In Determine 1, monitoring the corporate’s weekly efficiency, you’ll be able to see that traders have priced it at decrease market values than 12-months in the past, telling me that expectations have additionally been revised decrease.

The inventory has now set a collection of lower-lows and lower-highs, supporting this view. Moreover, the divergence in EMBC’s fairness line versus the benchmark index (VOO) is noticed in Determine 2. Thus, the chance price of holding EMBC since December final yr has been within the realms of 16%. Internet-net, I proceed to charge EMBC a maintain for causes mentioned on this report.

Determine 1.

Information: Updata

Determine 2.

Information: Updata

Updates to crucial funding info

Intensive evaluation of the prevailing knowledge exhibits EMBC has been fairly busy in proofing up enterprise progress for the approaching years.

For one, it has been deepening partnerships with key prospects, securing most popular model standing, and it signed multi-year agreements with (what EMBC calls) main retailers and payers earlier this yr. Such initiatives appears to be like have yielded constructive outcomes:

- For instance, the corporate was awarded an unique most popular place on the Categorical Scripts Nationwide Most well-liked Formulary, and, it was awarded important contract wins from the US Division of Veterans Affairs (“DVA”). Each of those recommend EMBC has obtained a stage of credibility since itemizing.

- Additional on the collaboration entrance, EMBC lately entered right into a co-promotion settlement with PolyPhotonix to advertise its sleep masks within the UK. That is related because the masks are designed to be used in sleep problems in sufferers with diabetes.

- It additionally signed a take care of Tidepool, to develop an automatic insulin pump for sufferers with Kind 2 diabetes. That is set to apparently embrace EMBC’s patch pump.

Thus, you’ll be able to see EMBC’s proactivity in establishing these agreements, as talked about. Alas, this is not the problem for mine within the funding debate.

The difficulty is shifting ahead is threefold: 1) Financials are weaker, 2) sentiment is absent, and three) valuations are unsupportive of a score greater. In different phrases, there is probably not any mis-pricings with the inventory at 7.6x ahead earnings—fairly the low cost.

For instance:

- The agency booked Q2 revenues of $277.1mm, a acquire of simply 90bps YoY, not conducive to catch a bid for its fairness inventory in my view. Backing out FX headwinds, the expansion was 4%.

- U.S.-dominated revenues have been up 360bps YoY to $146.4mm, in comparison with 440bps progress in worldwide turnover to $130.7mm. These outcomes truly surpassed inner expectations set by administration in earlier intervals.

- It pulled this to working revenue of ~$85mm (31% margin), from gross of 68.5%.

EMBC additionally revised its full-year progress assumptions as properly. It requires progress between 0—1%, however not a lot of a distinction from the earlier vary of destructive 1.5% to 0.5%. This nonetheless leads to $1.1–$1.13Bn on the prime line, and consensus has the identical numbers for FY’23 and FY’24. It sees this on -37.5% and 13% YoY progress in earnings over the identical time, respectively.

I might additionally level out the truth that, since itemizing, the corporate’s guide worth per share has remained destructive [Figure 2]. A part of this stems from the $1.6Bn in debt on the steadiness sheet, resulting in destructive fairness worth of $822mm on the time of writing. That is compounded by the $545mm in amassed deficits since itemizing as properly, pushed by the actual fact post-tax earnings have slipped off highs of ~$112mm in March FY’22, now at $46.4mm within the TTM.

Determine 2.

Information: Creator, EMBC SEC Filings

The query we have now to ask ourselves right here is certainly one of alternative price. Is it actually value shopping for an organization at the moment, that initiatives flat income progress and substantial wind backs in earnings for the subsequent 2 years? Added to that, you are shopping for destructive $14/share in guide worth, regardless of EMBC clipping $94mm in TTM earnings in Q2.

It’s true that the pre-carve-out figures are primarily based on explicit accounting ideas, and thus, “don’t [necessarily] replicate what Embecta’s monetary outcomes would have been, had Embecta operated as a standalone public firm,” in response to the CFO. Nonetheless, it has been all downhill on the basic and valuation entrance since itemizing. By all measures mentioned right here at the moment, these developments look to proceed going ahead, thus supporting a impartial view.

Market-generated knowledge

Within the absence of strong fundamentals, it’s crucial to depend on investor positioning and knowledge gathered from worth research to information worth visibility into the long run. Inspecting the cloud charts under [Figure 3 and Figure 4]— starting with the each day chart, it’s evident that the value and lagging line are located under the cloud and diverging from it.

Except there’s a substantial shift, any bullish outlook is unwarranted primarily based on this presentation. The each day chart offers perception into the weeks forward, main me to keep up a impartial outlook within the mid-term. The weekly chart in Determine 4 appears to be like to the months forward, and equally signifies a non-bullish development. Sadly, no discernible catalysts (past the subsequent earnings report) recommend a reversal is probably going, thereby confirming my impartial stance.

Determine 3.

Information: Updata

Determine 4.

Information: Updata

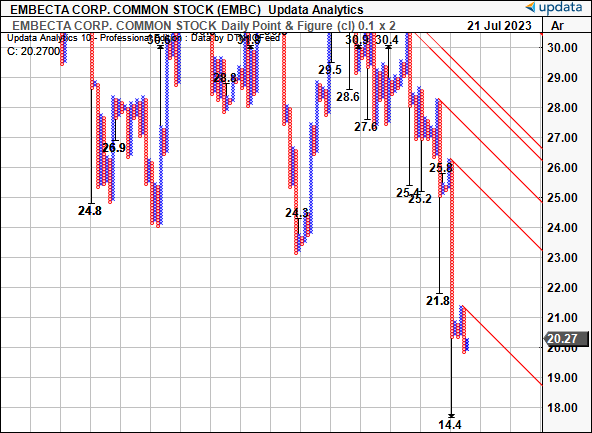

Level and determine research—just like the one proven in Determine 5—are an efficient technique of eradicating extraneous elements and temporal noise to be able to obtain a extra goal view of worth motion. These research noticed the decline within the EMBC share worth from $25 to $20, and at the moment point out a doable draw back goal of $14.40 as proven. In my opinion, ought to the present worth drop additional, this goal can be activated. Due to this fact, in gentle of this, it might be unjustifiable to assign a bullish score presently.

Determine 5.

Information: Updata

Information generated via the choices market offers probably the most complete perception into investor positioning, because it represents precise cash in danger. Evaluation of the choices chain for August expiry reveals that demand is essentially targeting the places aspect. There’s a heavy focus of places with a strike depth starting from $30 all the way down to $22.50, each above the present market worth. These traders subsequently have the choice to promote at these costs within the occasion of an additional downward development. Conversely, there’s a focus of calls with a strike worth of $35, even extending out to $50.

It’s doable these pundits anticipate a transfer in the direction of this mark by August. Nonetheless, it’s evident that the dimensions is primarily dominated by these positioned for EMBC to show decrease, or not less than observe sideways. On that time, we won’t low cost the actual fact a few of this open curiosity might be options-based methods that contain each calls and places, within the occasion of a congested market (in different phrases, when the inventory trades sideways with no directional bias).

Valuation and conclusion

These trying to find deep reductions will probably discover worth in EMBC buying and selling at 7.6x earnings and 7x ahead EBITDA. You’ve got obtained EMBC thus priced at 62% and 48.7% reductions to the sector, respectively. That, and the inventory comes with a 3% trailing dividend yield on the time of writing.

To those factors, I might hyperlink again to the query I raised earlier— is it value shopping for destructive progress for the subsequent 2-years? Mentioned one other manner, when you purchased EMBC at the moment, you would be paying $7.60 for each $1 in future earnings—just for these to lower by 37.5% after which one other 13% over the subsequent 2 years respectively. Then once more ask your self, simply as I’ve carried out, what’s the alternative price of doing this. Based mostly on sound funding logic, and a considerate evaluation of the long run, it might seem the deep reductions EMBC is priced at are justified on a basic foundation. An organization’s inventory worth is solely a set of expectations discounted to a sure mark. If traders imagine the sector will commerce at 20x earnings—because it does for broad healthcare—and EMBC to commerce at 7.66x earnings, maybe it means that EMBC will doubtless proceed this destructive unfold. The narrative can be totally different if we had the basics to say there’s a mispricing, however in my view, the low cost is warranted. This helps a impartial view.

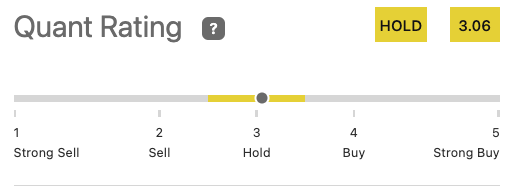

In abstract, the carve-out of EMBC from BDX was probably a horny play to supply traders publicity to diabetes administration. Thus far, nonetheless, and searching ahead, there would not seem like the required basic catalysts to recommend Embecta Corp. will commerce greater within the medium time period. Administration undertaking flat YoY progress this yr and the subsequent, and each Wall Road plus my very own inner expectations echo this view. In that vein, I proceed to charge EMBC a maintain till proof suggests in any other case. Word this view is shared objectively with the quant score system, that charges EMBC a maintain.

Determine 6.

Information: In search of Alpha