S&P 500, Dollar, GBPUSD, USDJPY and Recession Talking Points:

- The Market Perspective: USDJPY Bearish Below 141.50; Gold Bearish Below 1,680

- For the S&P 500, the week has opened to its biggest bullish opening gap since November 9, 2020; but there remains a serious hurdle to fueling conviction

- China has delayed its 3Q GDP release, leaving the fundamental course to drift somewhat – not an inspiring backdrop for establishing a genuine recovery

Recommended by John Kicklighter

Get Your Free Top Trading Opportunities Forecast

S&P 500 – A Rally that Falls Short in Technical, Fundamental and Conditional Support

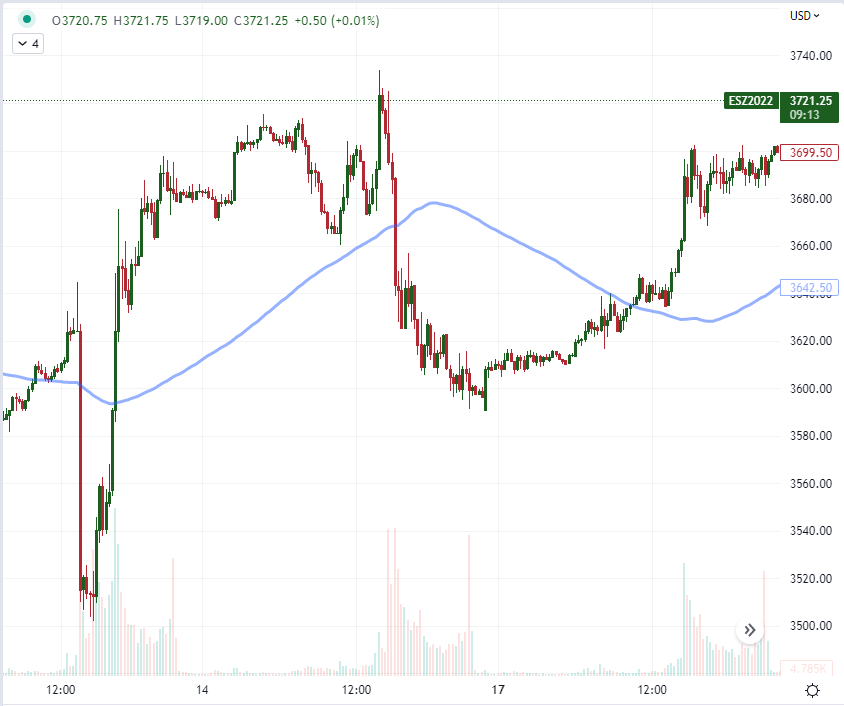

The new trading week has opened to some exceptional volatility – with yet another reversal in the speculative compass. Last week, exceptional volatility led the S&P 500 swing between extreme slide and extreme gains. To start this new week, there was a robust 1.55 percent gap higher to start the New York session – the biggest such charge since November 9, 2020 – but follow through all but fell apart after the ‘pre-market’ charge. The rally was notable, but the lack of technical, fundamental and market condition support exposes some serious contrast in intention. There is no denying the market’s charge Monday, but the lack of follow through from the S&P 500 so close to its two-month channel and the 20-day SMA would seem a prime candidate for a next foothold. The market may very well muster a bid for the speculative favorites, but I remain more than dubious about the intention for follow through given the expectations for volatility, volume and capital asset performance through October in general and the 42nd week of the year in particular.

Chart of S&P 500 with Volume, 20-Day, 100-Day, 100-Week SMAs, and Daily Gaps (Daily)

Chart Created on Tradingview Platform

I’m dubious of the risk appetite that we witnessed to start the week for a number of reasons. Where the traction is the most impressive (technicals), there remains critical overhead for chart observers. While the SPX gapped higher on the open and extended its run through the very early hours of trade Monday, there was almost no follow through to be found which in turn further solidifies the past two months’ range top and the 20-day simple moving average. To add to he lack of technical weight we have working on sentiment, we have the closer view of price action on the emini futures’ performance. The pre-US open rally was well represented, but the follow through all but vanished into active trading. Market conditions at present tend to favor speculative sentiment views but not if they are fueling whiplash on conviction. It is worth noting that while the SPX rallied this past session, activity levels tends to throttle down after the 41st week of the year’s volatility peak and macro fundamental backing is all back absent – at least through the week’s open. Perhaps that explains why the S&P 500 charged higher Monday before the official session open, but follow during active trade all but collapsed.

Chart of Emini S&P 500 Futures with Volume and 100-Period SMAs (15 Minute)

Chart Created on Tradingview Platform

Some Relief from the Financial Extremes

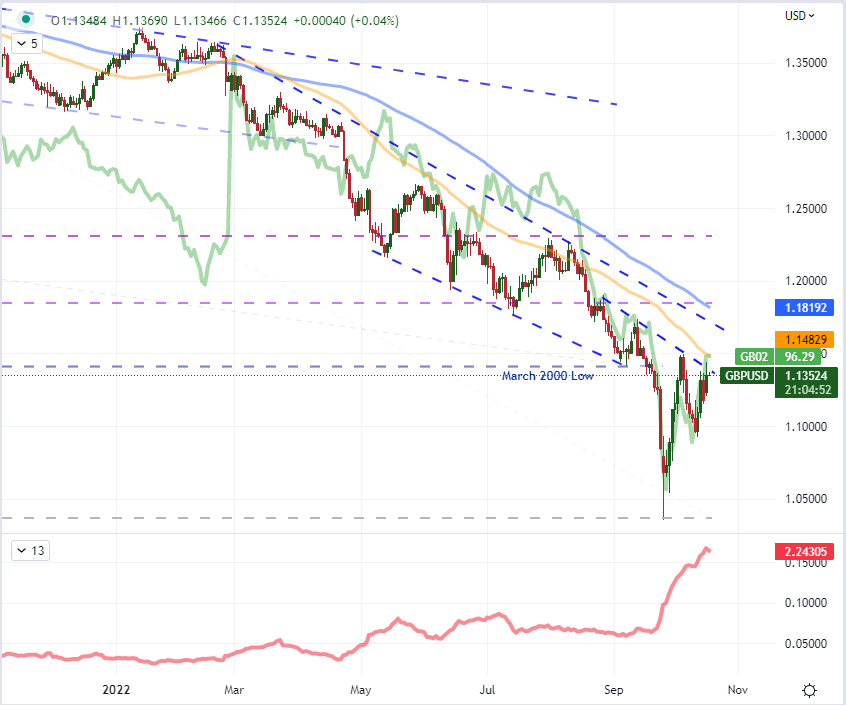

It wasn’t just the bounce in the S&P 500 that stood out this past session. There was a general improvement in risk-sensitive assets, and the bounce couldn’t have come any sooner. At the fringes of the speculative web, the rebound helped fend off more serious financial developments. In the FX markets, the swing in sentiment helped out GBPUSD in a serious way. At the end of this past week, the announced sacking of the old finance minister and walk back on some of the most aggressive mini-budget items (such as the reversal on the corporate tax hike by the Johnson administration) didn’t exactly inspire full enthusiasm. New Chancellor Jeremy Hunt seems to have noticed the underwhelming market response through last week and took the step to more fully reverse the tax cuts on Monday. Is that enough to restore confidence in the UK’s financial stability? Or is there irreparable damage to conviction which merely awaits the next global spark? High volatility (below is the 20-day ATR) and technical overhead makes the risk of a stalled recovery particularly threatening.

Recommended by John Kicklighter

How to Trade GBP/USD

Chart of GBPUSD with 50 and 100-Day SMAs, 20-Day ATR and 2-Year Gilt Prices (Daily)

Chart Created on Tradingview Platform

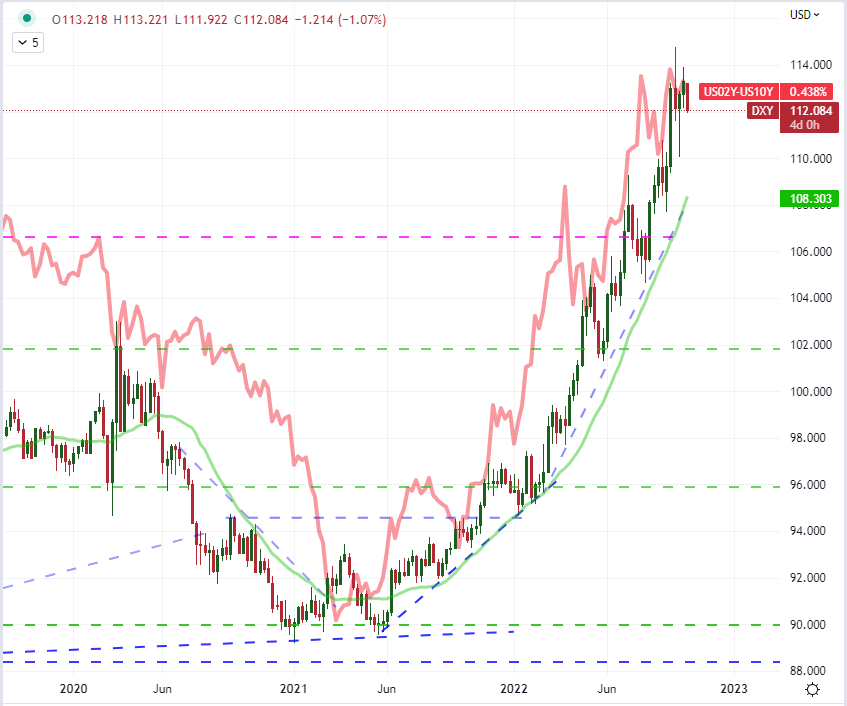

A broader area of relief to the financial system Monday for me was the general retreat from the US Dollar. There are few more pressing matters against financial stability than the multi-decade high from the Greenback. The practical implications for export inflation pressures and the trouble afforded emerging markets looking to finance their massive debt load cannot be overlooked. While the USD retreat is praised for its relief, it isn’t exactly a reliable trend to draw from yet. What was the motivation to the currency’s trip? Rate expectations haven’t faltered thus far, but there is perhaps a watered down safe haven perspective with the bounce in the S&P 500. Another point of influence was the easing of the recession pressure gauge. The 2-10 spread – difference between the 10-year and 2-year Treasury yields which is used to gauge recession risk by the market – moderated Monday. A single day’s retreat is there, but it is far too nascent to call a trend.

Recommended by John Kicklighter

Get Your Free USD Forecast

Chart of DXY Dollar Index with 20-Week SMA Overlaid with 2-10 Treasury Spread Inverted (Weekly)

Chart Created on Tradingview Platform

USDJPY and Event Risk – Don’t Get Too Confident of the Rebalance

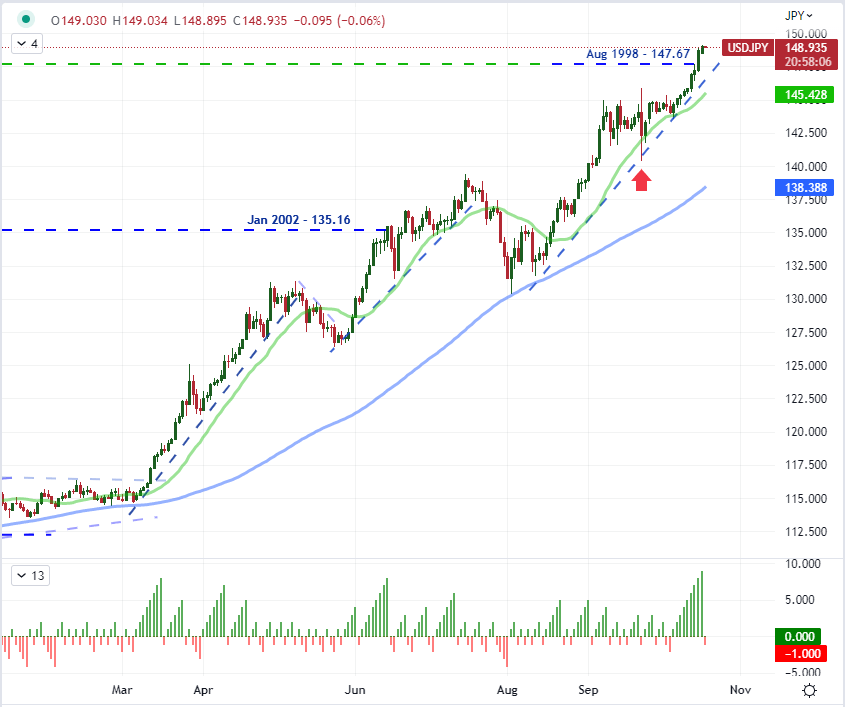

One top measure of financial instability of late that wouldn’t conform to the bounce in US indices and (very notably) the retreat from the Dollar was the further extension of the USDJPY. Those that register their fundamentals in the most literal terms could explain the pair’s further climb on a risk backdrop that would prize carry, but this is such an overt slap in the face to Japanese policy authorities that it simply doesn’t register as respite. With Monday’(admittedly modest) 0.2 percent gain, we are no dealing with the 9th consecutive advance from the world’s second most liquid currency pair int eh world. That is the longest charge in over 11 years and pushes the bounds of the exchange rate’s highs not seen since 1990. The fact that this climb is occurring in spite of Japanese officials’ intervention over three weeks ago warrants serious skepticism.

Recommended by John Kicklighter

How to Trade USD/JPY

Chart of USDJPY with 20-Day and 100-Day SMAs and Consecutive Candle Count (Daily)

Chart Created on Tradingview Platform

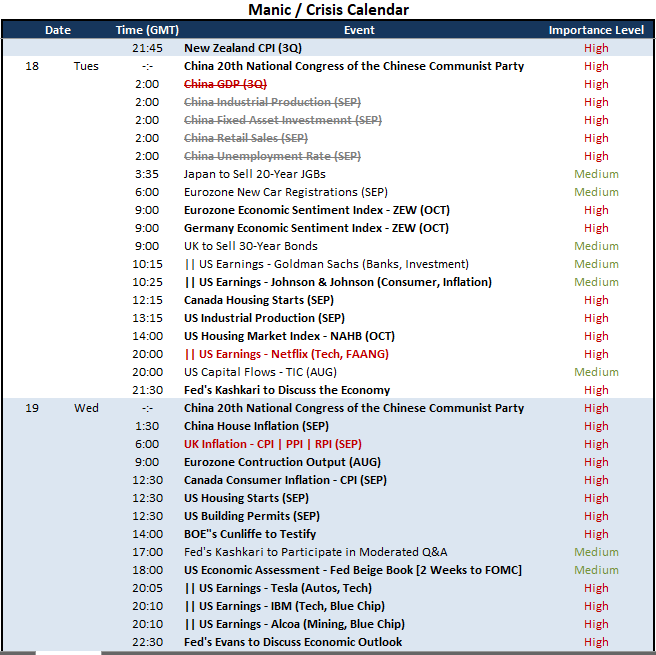

If you are looking for the next tangible fundamental foothold to establish the tentative recovery or to fully snuff it out, the docket Tuesday has dropped perhaps its most potent relief. The 3Q Chinese GDP release seemed a surprise data point given that National People’s Congress is taking place and the data was likely to bring invite a significant extension to the data series’ slide. It is hard to tell what would have been met with the greatest consternation: a further slide in the Chinese economic health series or a miraculous rebound that triggered deep skepticism. In the meantime, there are other measures that should be digested moving forward. The Eurozone economic sentiment survey from ZEW and US NAHB housing market health index are two important readings for the macro watchers – but their market moving capacity is very unclear. I will be watching the evolution of the US earnings session as another opening for skepticism with the Netflix report after the close still swinging the weight of the FAANG behind it.

Critical Macro Event Risk on Global Economic Calendar for Next Week

Calendar Created by John Kicklighter

Trade Smarter – Sign up for the DailyFX Newsletter

Receive timely and compelling market commentary from the DailyFX team

Subscribe to Newsletter