Up to date on November 2nd, 2024 By Felix Martinez

The Dividend Kings are a selective group of shares which have elevated their dividends for a minimum of 50 years in a row. We imagine the Dividend Kings are among the many highest-quality dividend progress shares to purchase and maintain for the long run.

With this in thoughts, we created a full checklist of all of the Dividend Kings. You may obtain the total checklist, together with vital monetary metrics similar to dividend yields and price-to-earnings ratios, by clicking the hyperlink under:

Walmart Inc. (WMT) is a Dividend King, and an American retail big.

In 1974, Walmart paid its preliminary dividend of $0.05 per share, which has been raised yearly for 51 consecutive years, making it a Dividend King. Lately, numerous retailers have confronted challenges attributable to competitors from web retail, spearheaded by Amazon (AMZN).

Nonetheless, by adapting, Walmart has demonstrated its potential to thrive in a quickly altering surroundings. The corporate has made substantial investments in its e-commerce platform. In contrast to many different retailers, Walmart has proven it could compete with Amazon.

This text will focus on the corporate’s enterprise overview, progress prospects, aggressive benefits, and anticipated returns.

Enterprise Overview

In 1945, Sam Walton opened his first low cost retailer, which served as the start line for what later turned referred to as Walmart. Since then, Walmart has expanded to turn into the world’s largest retailer, catering to over 230 million prospects each week. The corporate’s income exceeded $648 billion in 2023, and its market capitalization is roughly $660 billion.

As some of the outstanding employers globally, Walmart has a workforce of about 2.1 million.

Supply: Investor Presentation

Walmart has additionally expanded into quite a lot of totally different providers, making it a real conglomerate. The Walmart U.S. section contains retail shops in all 50 U.S. states, Washington D.C., and Puerto Rico, in addition to Walmart’s digital enterprise. Walmart Worldwide consists of operations in 25 international locations outdoors the U.S.

Lastly, Sam’s Membership is a membership-only warehouse membership that operates in 48 states and Puerto Rico.

Development Prospects

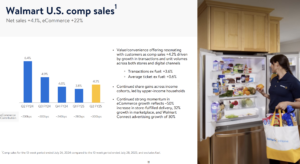

The corporate reported sturdy monetary outcomes for the second quarter of fiscal yr 2025, with whole income growing by 4.8% to $169.3 billion, largely pushed by progress in Walmart U.S. and Worldwide segments. eCommerce was a standout contributor, reaching a 21% enhance globally, whereas Walmart U.S. comp gross sales rose by 4.2%, underscoring the success of Walmart’s multi-channel strategy combining in-store and digital experiences. The corporate additionally raised its full-year outlook, projecting FY25 web gross sales progress between 3.75% and 4.75% and adjusted working revenue progress of 6.5% to eight.0% in fixed foreign money, reflecting sturdy shopper demand and improved operational effectivity.

Walmart’s new companies, together with promoting, market, and membership providers, skilled notable progress, diversifying its income streams and boosting general profitability. Promoting income surged by 26% globally, and U.S. market gross sales noticed a 30% enhance, pushed by enhanced retailer-partner relations and store-fulfilled deliveries. The gross revenue charge improved by 43 foundation factors, attributed to larger membership revenue, decreased eCommerce losses, and price efficiencies throughout Walmart’s Worldwide and Sam’s Membership segments. Stock administration remained environment friendly with a 2% international stock discount, signaling sturdy operational well being and a strategic stability between inventory ranges and demand.

The corporate’s steering for Q3 suggests additional progress, with web gross sales anticipated to rise between 3.25% and 4.25% and working revenue by 3.0% to 4.5% in fixed foreign money. CEO Doug McMillon emphasised Walmart’s dedication to offering worth and comfort, contributing to a 6.4% return on belongings (ROA) and a 15.1% return on funding (ROI) for the quarter. With $8.8 billion in money reserves and a free money circulation of $5.9 billion, Walmart plans to proceed repurchasing shares and investing in progress initiatives, positioning itself effectively in a aggressive retail panorama.

US comparable gross sales have been up 6.4% year-over-year.

Supply: Investor Presentation

After Q2 outcomes, we up to date our estimate to $2.45 in earnings per share. We presently forecast Walmart to develop its earnings per share by 11% per yr over the following 5 years.

Aggressive Benefits & Recession Efficiency

Walmart’s major aggressive benefit is its intensive scale, enabling it to take care of low transportation prices and excessive distribution efficiencies. Consequently, the corporate can go these financial savings to prospects at reasonably priced costs, contributing to its on a regular basis low-price technique.

Promoting is one other power of Walmart that helps keep its model recognition. The corporate’s huge monetary sources enable it to speculate billions of {dollars} yearly in promoting.

Furthermore, Walmart’s aggressive benefit ensures constant profitability, even throughout financial recessions. The corporate carried out remarkably effectively through the Nice Recession, highlighting the resilience of its enterprise mannequin.

It steadily grew earnings-per-share annually in that point:

- 2007 earnings-per-share of $3.16

- 2008 earnings-per-share of $3.42 (8.2% enhance)

- 2009 earnings-per-share of $3.66 (7% enhance)

- 2010 earnings-per-share of $4.07 (11% enhance)

Regardless of the financial recession being some of the extreme in a long time, Walmart’s efficiency was commendable. The corporate delivered sturdy outcomes even through the coronavirus pandemic that led to a recession within the U.S.

Walmart’s progress trajectory signifies that the corporate might doubtlessly achieve from recessions. As a retail chief providing low-cost merchandise, Walmart might expertise a surge in site visitors throughout financial downturns as customers cut back from pricier retailers.

Valuation & Anticipated Complete Returns

Walmart shares presently commerce at a worth of ~$81. Utilizing our earnings-per-share estimate of $2.45 for the present fiscal yr, the inventory has a price-to-earnings ratio of 33.1x. That is above our truthful worth estimate P/E ratio of 25x. Traders must also word that retailers have sometimes not held P/E multiples above 20.

If the valuation a number of have been to revert to our truthful worth estimate within the subsequent 5 years, the corporate’s whole returns would see annual returns decline by 6% per yr. Walmart shares have carried out effectively for an prolonged interval. Whereas this has rewarded shareholders with sturdy returns, we view Walmart as a barely overvalued inventory.

Apart from modifications within the P/E a number of, Walmart must also generate returns from earnings progress and dividends. A projection of anticipated returns is under:

- 11% earnings-per-share progress

- 1.0% dividend yield

- -6% a number of reversion

On this situation, Walmart is projected to generate a complete return of 6.0% per yr over the following 5 years.

Ultimate Ideas

Whereas many retailers have struggled to adapt to the change in commerce buying habits, Walmart has made the right strategic investments. The corporate’s spectacular e-commerce progress displays this view.

The corporate has carried out effectively by producing roughly 18.6% annualized whole returns previously 5 years. We discover the corporate’s dividend observe file to be spectacular, with the latest dividend hikes of 9%.

Walmart is a secure, defensive inventory in occasions of financial hardship, however the modest whole return profile prevents it from being a purchase right now. Consequently, we charge it a maintain.

The next articles include shares with very lengthy dividend or company histories, ripe for choice for dividend progress traders:

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to help@suredividend.com.