Up to date on March eighth, 2022 by Felix Martinez

The Dividend Aristocrats are a gaggle of 66 corporations within the S&P 500 Index, with 25+ consecutive years of dividend will increase. Broadly talking, they’re among the many highest-quality dividend development investments in all the inventory market.

You may see a full downloadable spreadsheet of all 66 Dividend Aristocrats, together with a number of essential monetary metrics resembling price-to-earnings ratios, by clicking on the hyperlink under:

This replace will cowl meals distributor Sysco (SYY). Sysco has a protracted historical past of regular dividends and common dividend will increase. It has paid a dividend each quarter because it went public in 1970.

Sysco has many enticing qualities as a dividend development inventory. It’s the largest firm in its business, which supplies it with larger revenue margins and sturdy aggressive benefits over its smaller rivals. It additionally has development potential, and the power to extend its dividend every year.

Enterprise Overview

Sysco was based in 1969 and went public the next yr. In its first yr as a publicly-traded firm, it has a market cap of $43.1 billion. The corporate has grown steadily over the practically 5 a long time since. Final yr, Sysco had gross sales of greater than $51 billion.

At the moment, Sysco is the most important meals distributor within the U.S. It distributes merchandise together with contemporary and frozen meals, in addition to dairy and beverage merchandise. It additionally supplies non-food merchandise together with tableware, cookware, restaurant and kitchen provides, and cleansing provides.

The corporate has a variety of consumers, which embody eating places, healthcare amenities, schooling, authorities workplaces, journey, leisure, and retail companies. It additionally has a big section of different buyer varieties resembling bakeries, church buildings, civic and fraternal organizations, merchandising distributors, and worldwide exports.

In all, Sysco has roughly 600,000 prospects. Its place atop the meals distribution business supplies Sysco with high-profit margins and future development potential.

Supply: Investor Presentation

Progress Prospects

The working local weather for Sysco was challenged over the previous two years because the coronavirus pandemic pressured closures of eating places and different eating venues that make up Sysco’s buyer base. Additionally, provide chain points throughout the nation.

Happily, Sysco remained worthwhile in 2021 and hopes to see a extra vital restoration in 2022. On February eighth, 2022, Sysco reported second quarter Fiscal 12 months (FY) 2022 outcomes. Gross sales elevated by 41.2% for the quarter, whereas gross revenue elevated throughout all segments year-over-year. For the primary half of FY 2022, gross sales are up 40.5% and gross revenue elevated 35.8%. Over the primary six months of the fiscal yr, earnings-per-share elevated 174.5% for the primary six months of the fiscal yr in comparison with the primary six months of FY2021.

As eating places and different eating institutions open up, buyers are hoping that Sysco will proceed to see its gross sales and revenue steadily improve.

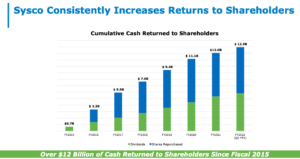

Supply: Investor Presentation

The mix of natural gross sales development, acquisition-added income development, and share repurchases is anticipated to end in ~7% annual earnings-per-share development, in our view. We imagine that is an attainable purpose, as a result of firm’s robust enterprise mannequin and spectacular aggressive benefits.

Supply: Investor Presentation

Aggressive Benefits & Recession Efficiency

The U.S. foodservice business is fiercely aggressive. There are literally thousands of rivals to Sysco, which embody different meals distributors, in addition to wholesale or shops, grocery shops, and on-line retailers. Sysco additionally faces the chance of its prospects negotiating instantly with its suppliers.

Nonetheless, what has saved rivals at bay for therefore a few years, is that Sysco is the most important operator within the business. It controls about 16% of the U.S. foodservice business. Sysco operates over 300 distribution amenities worldwide and serves over 600,000 buyer places. Such an enormous presence permits Sysco to maintain prices low, ant it may well go on the profit to its prospects.

One other good thing about Sysco’s enterprise mannequin is that it’s proof against recessions. Everybody has to eat, which supplies Sysco a sure degree of demand, whatever the situation of the U.S. financial system.

This is the reason Sysco’s income held up nicely throughout the Nice Recession:

- 2007 earnings-per-share of $1.60

- 2008 earnings-per-share of $1.81 (13% improve)

- 2009 earnings-per-share of $1.77 (2% decline)

- 2010 earnings-per-share of $1.99 (12% improve)

Sysco grew earnings-per-share at a double-digit tempo in 2008 and 2010, with solely a gentle dip in 2009. The corporate grew earnings from 2007 to 2010, which was a uncommon achievement.

Sysco’s secure business and high aggressive place, allowed it to boost its dividend every year, even throughout recessions.

Valuation & Anticipated Returns

Whereas the coronavirus pandemic has had a big impact on Sysco, we imagine the corporate has will earn $3.05 per share for FY2022. Based mostly on this, the inventory has a price-to-earnings ratio of 25.2. Our truthful worth estimate is a price-to-earnings ratio of 20, which suggests the inventory is at present buying and selling larger than our truthful estimate.

As a result of Sysco is an overvalued inventory, annual returns may very well be diminished by 5.6% per yr if the P/E a number of declines to twenty over the following 5 years. As a substitute, shareholder returns can be generated by earnings development and dividends.

Happily, Sysco doesn’t have to depend on a number of expansions, as the corporate has a gorgeous development profile and dividend. We anticipate Sysco to ship as much as 7% annual earnings development going ahead, consisting of natural development, acquisitions, and share repurchases.

As well as, Sysco has a present dividend yield of two.2%, which is the next yield than the common yield of the broader S&P 500 Index. This results in complete anticipated annualized returns of three.6% per yr over the following 5 years. It is a weak anticipated charge of return, making the inventory a promote on valuation considerations.

Sysco ought to have little hassle growing its dividend going ahead. The corporate has a projected dividend payout ratio of 62% for fiscal 2022. This means the dividend is greater than sufficiently coated.

Remaining Ideas

Sysco operates on the high of a secure business. It has an entrenched business place and will see regular demand, even throughout recessions. These qualities make Sysco a dependable inventory for revenue.

Sysco is on the unique record of Dividend Kings, a gaggle of shares with 50+ consecutive years of dividend will increase.

The inventory is overvalued, which means proper now is just not one of the best time to purchase the inventory. Sysco shares are at present sitting close to an all-time excessive. We imagine future returns can be passable, however not spectacular, for buyers shopping for the inventory on the present valuation degree.

Nonetheless, we imagine the inventory can generate optimistic returns even at this valuation, by way of earnings development and dividends. Because of this, Sysco stays a high quality holding inside a dividend development portfolio, however the inventory is just not a purchase on the present worth.

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to assist@suredividend.com.