Up to date on January thirty first, 2023 by Aristofanis Papadatos

Chevron Company (CVX) is likely one of the largest and most well-known oil shares on the planet. It is usually one of the crucial secure, having grown its dividend for 36 consecutive years with the newest enhance of 6%.

In consequence, Chevron is a member of the unique Dividend Aristocrats – a gaggle of 68 elite dividend shares with 25+ years of consecutive dividend will increase.

We consider the Dividend Aristocrats are a few of the highest-quality dividend shares in your complete inventory market. With this in thoughts, we created a full record of all 68 Dividend Aristocrats, together with necessary monetary metrics resembling dividend yields and P/E ratios.

You’ll be able to obtain a replica of our full Dividend Aristocrats record by clicking on the hyperlink beneath:

Because of the trade’s reliance on excessive commodity costs for profitability, there are simply two power shares on the record of Dividend Aristocrats – Chevron and Exxon Mobil (XOM). Chevron’s dividend consistency and stability assist it stand out within the otherwise-volatile power trade.

This text will analyze the intermediate-term funding prospects of Chevron.

Enterprise Overview

Chevron is considered one of 6 oil and gasoline supermajors, together with:

- BP (BP)

- Eni SpA (E)

- TotalEnergies (TTE)

- Exxon Mobil (XOM)

- Shell (SHEL)

Chevron is considered one of solely two oil and gasoline supermajors to be headquartered in the USA, together with fellow Dividend Aristocrat Exxon Mobil.

Like the opposite built-in supermajors, Chevron engages in upstream oil and gasoline manufacturing, in addition to downstream refining companies. In 2019, 2021 and 2022, Chevron generated 78%, 84% and 79%, respectively, of its earnings from its upstream section. It’s thus extremely delicate to the costs of oil and gasoline, particularly the worth of oil.

All of the oil producers have been severely harm by the coronavirus disaster in 2020 as a result of unprecedented lockdowns and the resultant collapse of world oil consumption. Chevron was not an exception and thus it incurred an adjusted loss per share of -$0.20 in that 12 months.

Fortuitously, because of the huge distribution of vaccines worldwide, international oil consumption started to get well in 2021. As well as, oil producers have enormously benefited from the invasion of Russia in Ukraine and the resultant sanctions of the U.S. and Europe on Russia. Earlier than the sanctions, Russia was producing about 10% of world oil output and one-third of pure gasoline consumed in Europe. Because of the sanctions, the worldwide oil and gasoline markets grew to become extraordinarily tight final 12 months and thus the costs of oil and gasoline skyrocketed to 13-year highs.

The profit from these exceptionally favorable situations was evident within the efficiency of Chevron in 2022. The oil main greater than doubled its earnings per share, from $8.13 in 2021 to an all-time excessive of $18.83 in 2022.

The costs of oil and gasoline have moderated off their peak however stay above historic common ranges. In consequence, Chevron is anticipated to put up earnings per share of about $15.00 this 12 months. This stage is decrease than the blowout stage in 2022 however it can mark the second-best efficiency within the historical past of the corporate if it materializes.

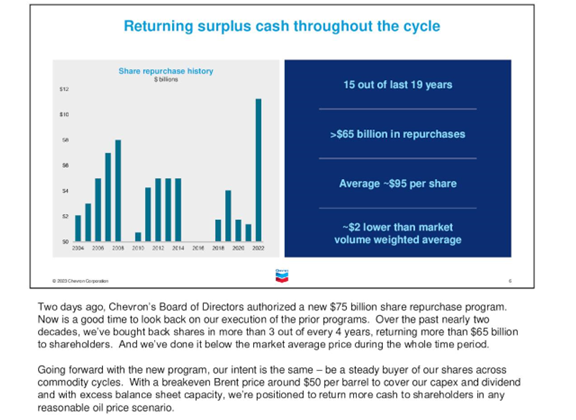

Due to its shiny short-term outlook, Chevron introduced a large share repurchase program of $75 billion for the subsequent few years. This quantity is adequate to scale back the share depend by 22% on the present inventory value. We’re cautious of this unprecedented share repurchase program close to the height of the cycle of the oil trade.

Then again, Chevron boasts of getting repurchased shares effectively all through its historical past.

Supply: Investor Presentation

The oil main has spent greater than $65 billion on share repurchases over the past 20 years, at a median inventory value of $95. As the present inventory value is almost double this value, administration feels vindicated for its execution. Nonetheless, we anticipate oil and gasoline costs to deflate within the upcoming years and thus we consider that share repurchases will improve shareholder worth far more at decrease oil and gasoline costs, which can in all probability be accompanied by a decrease inventory value.

Development Prospects

Chevron is likely one of the largest publicly traded power companies on the planet and stands to profit tremendously from elevated costs of oil and gasoline.

Chevron invested closely in progress initiatives for years however did not develop its output for a complete decade, as oil initiatives take a number of years to start out bearing fruit. Nevertheless, Chevron is now within the optimistic section of its investing cycle.

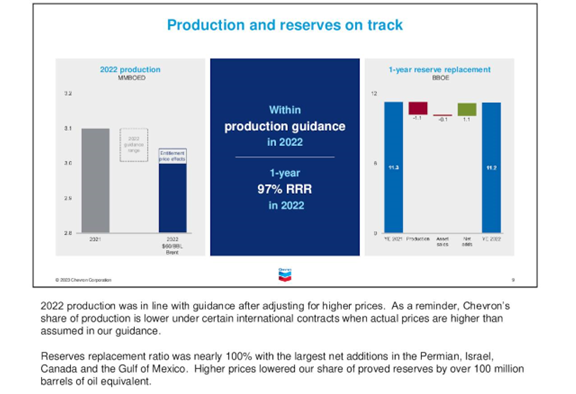

Chevron grew its output by 5% in 2017, 7% in 2018, 4% in 2019, 1% in 2020 and 0.5% in 2021. Its output dipped 3% in 2022 as a consequence of depressed funding throughout the pandemic however Chevron is prone to return to progress mode this 12 months because of its sustained progress within the Permian Basin and in Australia. The corporate has greater than doubled the worth of its property within the Permian within the final 4 years because of new discoveries and technological advances.

Chevron changed 97% of its reserves in 2022. Whereas this quantity is uninspiring from a long-term perspective, traders ought to concentrate on the depressed funding ranges of all of the oil producers over the past three years as a result of pandemic.

Supply: Investor Presentation

Chevron has begun to spice up its funding in progress initiatives and thus it’s prone to return to progress mode this 12 months. Administration not too long ago supplied steering for 0%-3% progress of manufacturing in 2023.

Chevron additionally realized its lesson from the earlier downturn and now invests most of its funds on initiatives that start delivering money flows inside two years.

Nevertheless, we anticipate oil and gasoline costs to deflate within the upcoming years, primarily as a result of file variety of renewable power initiatives which can be being developed proper now on account of the power disaster attributable to the struggle in Ukraine. In consequence, we anticipate the earnings per share of Chevron to lower by 9% per 12 months on common over the subsequent 5 years.

Then again, the dividend ought to proceed to develop, as the corporate continues its 30+ 12 months streak of upper payouts. This doesn’t essentially imply that traders will obtain a dividend increase every 4 quarters. There have been quite a few cases when Chevron held the dividend regular for greater than 4 quarters – with 2020-2021 being a major instance – and ultimately elevated it in order that the year-over-year comparability confirmed enchancment.

The necessary factor to notice is that Chevron is dedicated to a rising dividend in all environments.

Aggressive Benefits & Recession Efficiency

Chevron’s aggressive benefit within the extremely cyclical power sector comes primarily from its dimension and monetary energy. The corporate’s operational experience allowed it to efficiently navigate the 2020 coronavirus pandemic.

As a commodity producer, Chevron is weak to any downturn within the value of oil, significantly given that it’s the most leveraged oil main to the oil value. Nevertheless, because of its sturdy stability sheet, the corporate is prone to endure the subsequent downturn, identical to it has accomplished in all of the earlier downturns.

Chevron’s aggressive cost-cutting efforts have helped the corporate turn into extra environment friendly. Chevron has continued to scale back drilling prices, considerably lowering its break-even expense.

In truth, immediately Chevron claims to be the best-positioned for commodity value uncertainty, because it boasts one of many lowest money circulation break-even costs amongst its main oil counterparts.

Supply: Chevron 2020 Safety Analyst Assembly

Chevron stacks up effectively amongst its friends within the power sector. Nevertheless, the corporate is actually not probably the most recession-resistant Dividend Aristocrat, as evidenced by its efficiency throughout the 2007-2009 monetary disaster:

- 2007 adjusted earnings-per-share: $8.77

- 2008 adjusted earnings-per-share: $11.67 (33% enhance)

- 2009 adjusted earnings-per-share: $5.24 (-55% decline)

- 2010 adjusted earnings-per-share: $9.48 (81% enhance)

Chevron’s adjusted earnings per share declined by greater than -50% throughout the 2007-2009 monetary disaster, however the firm did handle to stay worthwhile throughout a bear market that drove lots of its opponents out of enterprise. This allowed Chevron to proceed elevating its dividend cost all through the Nice Recession. Chevron’s dividend security is way above the common firm within the power trade.

Valuation & Anticipated Whole Returns

Chevron’s anticipated whole returns are tougher to evaluate than many different firms. That is primarily as a result of extremely risky outcomes of the corporate, which end result from the dramatic swings of the costs of oil and gasoline.

With a share value close to $174, the price-to-earnings ratio presently sits at 11.6 occasions primarily based on 2023 anticipated earnings of $15.00 per share. If the inventory have been to revert to our truthful worth estimate of 14 occasions earnings, this is able to suggest a 3.8% annualized valuation tailwind.

Furthermore, the inventory is providing a 3.5% dividend yield. Nevertheless, the valuation tailwind and the dividend are prone to be offset by the anticipated 9% common annual decline of earnings per share. General, the inventory will be fairly anticipated to supply a -1.4% common annual return over the subsequent 5 years off its practically all-time excessive present inventory value.

Closing Ideas

Chevron is likely one of the uncommon oil and gasoline firms that was in a position to navigate via the Nice Recession of 2007-2009, the oil downturn of 2014-2016, and the COVID-19 pandemic with out slicing its dividend.

It has even managed to develop its dividend currently, together with a 6.3% enhance in 2019, an 8.4% enhance in 2020 and a 6.0% enhance in every of the final three years, together with 2023. On account of Chevron’s decrease value construction, it will probably now deal with a a lot decrease common value of oil. Moreover, new initiatives within the U.S. and worldwide markets will assist the corporate proceed to develop. Nonetheless, as we’re close to the height of the cycle of the oil trade, which is notorious for its dramatic swings, Chevron ought to in all probability be prevented round its present inventory value.

Moreover, the next Positive Dividend databases include probably the most dependable dividend growers in our funding universe:

For those who’re in search of shares with distinctive dividend traits, think about the next Positive Dividend databases:

The key home inventory market indices are one other strong useful resource for locating funding concepts. Positive Dividend compiles the next inventory market databases and updates them month-to-month:

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to help@suredividend.com.