")

Natal-is

Funding Thesis

Crocs, Inc. (NASDAQ:CROX) is a Colorado-based world way of life model that designs, produces, and distributes progressive footwear, equipment, and attire. Its mission is to supply everybody with snug, light-weight, and versatile footwear.

This as soon as uninspired, unloved, and unprofitable firm has since turn out to be a money cow with a broad array of thrilling product strains with intense model loyalty and satisfaction. With robust income progress and EBITDA margins as excessive as 30%, rivaling software program firms, we imagine CROX inventory is a Sturdy Purchase because of its robust monetary efficiency, best-in-class margins, and strategic enlargement into new markets and e-commerce.

Enterprise Overview

Crocs’ signature product is the Traditional Clog, a slip-on shoe product of a proprietary closed-cell resin materials known as Croslite. Crocs’ footwear merchandise are in style for his or her sturdiness, consolation, and distinctive designs. The corporate additionally provides a spread of equipment, together with Jibbitz charms that may be hooked up to Crocs footwear, and a line of attire that options the Crocs model.

The corporate sells its merchandise by way of a number of channels, together with its web site, company-owned retail shops, third-party retail shops, and e-commerce marketplaces. Crocs’ geographic presence is diversified, with operations in North America, Europe, Asia Pacific, and the Center East.

Crocs has skilled robust progress in recent times, pushed by its deal with innovation, advertising, and worldwide enlargement. The corporate has efficiently leveraged its iconic model and powerful buyer loyalty to develop its product choices and enhance gross sales. As well as, Crocs has made important investments in e-commerce capabilities, enabling it to higher serve its prospects and drive on-line gross sales. Throughout the 2020 pandemic, CEO Andrew Rees made the smart resolution to drag from bodily retail shops and deal with e-commerce as a driver of gross sales. This guess paid off: as of 2022, e-commerce gross sales now make up nearly 50% of all revenues.

CEO Andrew Rees, This fall 2021 Earnings Transcript:

This yr, we invested in our digital capabilities, together with within the Crocs cell app, world social platforms, resembling Douyin, and digital expertise throughout the globe. We’re assured these investments and our continued focus will drive digital progress globally over the long run.

Wanting ahead, Crocs plans to proceed investing in product innovation and increasing its world presence. The corporate has recognized key progress alternatives in Asia, significantly in China, the place it plans to double its income by 2026. Crocs additionally plans to develop its direct-to-consumer channels, together with e-commerce and owned retail shops, to extend its model visibility and buyer engagement. Crocs additionally plans on specializing in its sandals enterprise, which solely makes up $300m of its income, because it believes it may be a heavyweight participant within the $30B TAM. Total, Crocs’ robust model and product choices, mixed with its strategic progress initiatives, place the corporate for continued success within the world footwear and equipment market.

The Energy of Sturdy Management

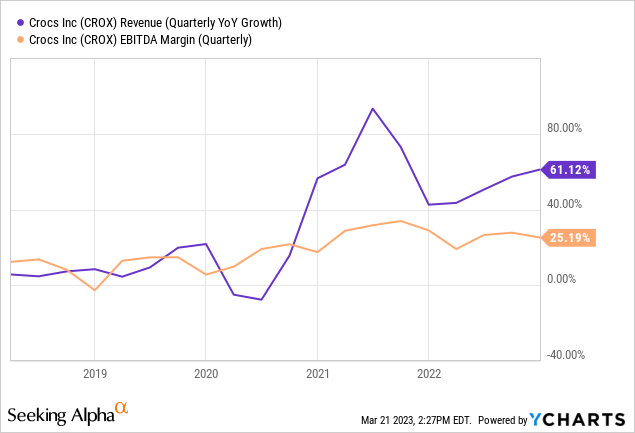

Regardless of preliminary skepticism, the corporate has undergone a outstanding transformation beneath the management of CEO Andrew Rees, who joined in 2014. In 2014, CROX was drowning. Advertising and marketing was lackluster, shops had been struggling, and bills had been uncontrolled. By tapping into the facility of social and digital advertising, he created buzz for the product by teaming up with influencers resembling Publish Malone and Vera Bradley. By bettering model relevance, bettering channels for e-commerce, and chopping pointless bills, he was capable of unlock the untapped potential of CROX. Since Rees took over, the corporate has turn out to be worthwhile with spectacular income progress, averaging 26.71% CAGR over the past 5 years, with a best-in-class 5 yr common EBITDA margin of 19.64%. CROX has additionally seen large progress in its share worth, growing an unbelievable 50.57% CAGR over the identical 5-year interval.

Monetary Statements

Compiled by Creator utilizing Looking for Alpha

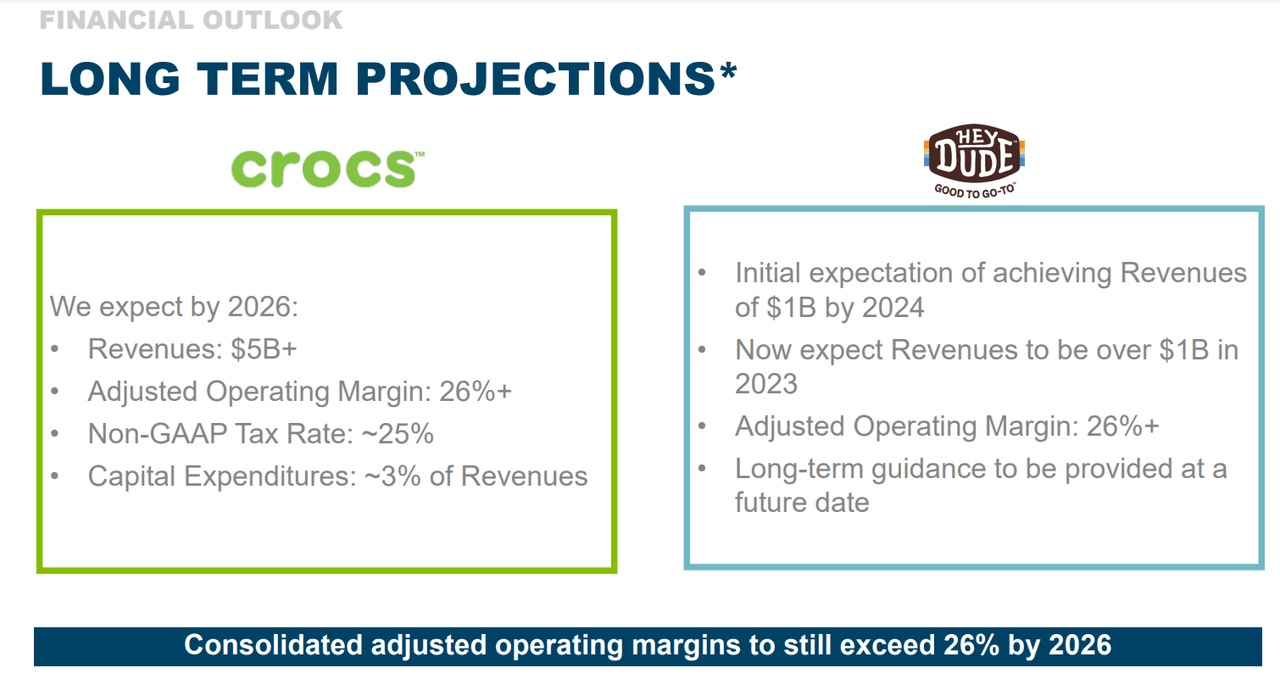

Crocs has exhibited outstanding progress in income over the previous 5 years, boasting a CAGR of 26.71% and a mean EBITDA margin of 19.64% over the identical interval. Nevertheless, it’s value noting {that a} substantial portion of this progress was achieved within the fiscal years of 2021 and 2022, with the latter yr’s progress principally attributed to the HEYDUDE acquisition. Whereas there stays a danger of income progress and EBITDA margins reverting to decrease ranges, administration has repeatedly emphasised that they count on income progress to stay within the low teenagers, with EBITDA margins to remain no less than at 26% for the subsequent few years. Moreover, administration has repeatedly emphasised Crocs’ long-term purpose is to surpass $6 billion in complete revenues by 2026 whereas sustaining a 26% EBITDA margin. Regardless of their spectacular revenue margins, Crocs’ present low 5-year common EV/EBITDA a number of of 15.5x is shocking.

Crocs Investor Presentation

HEYDUDE, what’s that debt?

When analyzing Crocs’ stability sheet, it is unimaginable to disregard their important $2.6B debt, which they acquired in FY22 because of their acquisition of HEYDUDE. The acquisition was initially met with skepticism, as Crocs paid a whopping $2.5B (with $2.05B funded by debt and $0.45B funded by shares) for an organization that was solely producing $600m in income with a low working margin. This 4x P/S acquisition of a shoe firm brought about a 13% drop in Crocs’ inventory worth, because the market punished the administration crew for his or her questionable buy.

Nevertheless, a yr later, the acquisition appears to have paid off for Crocs. HEYDUDE has efficiently built-in with Crocs, and the outcomes are beginning to present. Though Crocs initially guided for $1B in income for HEYDUDE by FY24, HEYDUDE was capable of accomplish almost $1B in revenues throughout FY22. Going ahead, they count on no less than 20% YoY progress for HEYDUDE for the subsequent few years, and as they proceed to combine the corporate, working margins for HEYDUDE are anticipated to enhance to a long run adjusted working margin of 26%+. Moreover, robust money circulation in FY22 has already allowed for a $550M discount in borrowings from $2.9B in Q1 to $2.3B in This fall. Whereas the debt is a priority, the HEYDUDE acquisition has the potential to be a big catalyst for Crocs’ progress sooner or later.

Crocs Investor Presentation

Dangers of the Enterprise

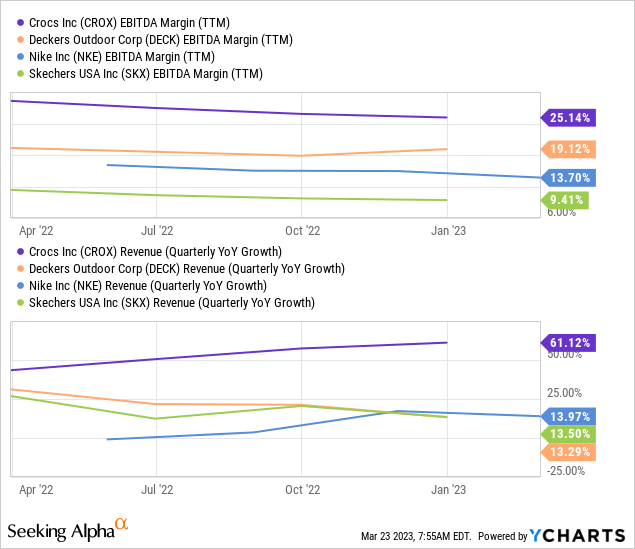

Whereas Crocs has proven robust income efficiency and powerful EBITDA margins in recent times, as a shopper discretionary product, it’s topic to altering tendencies. Whereas Crocs could also be seen as “cool” and trending for now, it’s potential for a shift in shopper sentiment to harm its top-line. Moreover, the corporate faces steady competitors from different shoe firms resembling Deckers Out of doors Company (DECK), Converse/Nike (NKE), and Skechers (SKX). Whereas Crocs has a sizeable benefit over all its opponents, this hole could not final eternally. Moreover, whereas CROX’s administration is extraordinarily bullish on its acquisition, it might nonetheless succumb to failure to combine correctly. The long-term outlook for HEYDUDE could deteriorate if administration is ready to correctly execute on future income progress and EBITDA margin enlargement.

Quantitative Evaluation

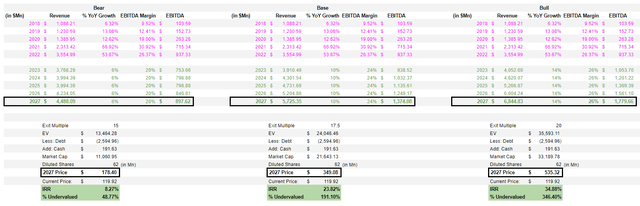

Compiled by Creator utilizing Looking for Alpha

In our bear, base, and bull case situations, we assume Crocs’ revenues will proceed to develop at a CAGR of 6%, 10%, and 14% over the subsequent 5 years, respectively. Moreover, we assume EBITDA margins of 20%, 24%, and 26%, respectively, and apply exit multiples of 15x, 17.5x, and 20x to mirror the income progress and profitability of every state of affairs. It’s value noting that our bull case is according to administration’s repeated steering.

What’s attention-grabbing is that every state of affairs presents important potential upside for CROX, starting from 48% undervalued to 346.40% undervalued. Given the present macroeconomic atmosphere, it could be prudent to scale back our expectations barely to account for potential execution points sooner or later whereas nonetheless leaving room for upside. Even when we’re unsuitable, any further upside can be a welcome bonus.

Our bear case considers the potential of a big slowdown in income progress and a lower in EBITDA margins, probably because of modifications in buyer loyalty or sentiment or elevated working bills. Our base and bull circumstances assume continued enlargement and penetration into new markets by Jibbitz, sandals, HEYDUDE, and clogs, and powerful shopper loyalty. If administration’s forecast materializes as anticipated, CROX can be undervalued by 346%, giving buyers a formidable IRR of 34.88% over the subsequent 5 years. Not too shabby.

The Backside Line

CROX has gone by way of an unbelievable transformation up to now decade. With CEO Andrew Rees main the best way, CROX has skilled robust progress in recent times, pushed by its deal with innovation, advertising, and worldwide enlargement. With administration paving the best way to $6B in income by 2026 with robust 26% EBITDA margins, CROX presents buyers with unbelievable upside, as a lot as 346%, because of its excessive income progress and even larger EBITDA margins. Mixed with HEYDUDE, we discover CROX to be an unstoppable firm, and fee it a Sturdy Purchase.

What are your ideas on HEYDUDE and CROX? The place do you see this firm going within the subsequent few years?