Supatman/iStock through Getty Pictures

Funding Thesis

Coursera (NYSE:COUR) pulled in constructive free money stream for the primary time in 2023, resulting from not solely the robust income but in addition internet earnings development. Though its liquidity and money place have strengthened, its revenue margin has taken a hit, displaying the constraints of its scale up efforts. The present value is sort of double of our most bullish valuation, indicating wealthy premium priced in that is probably not realized within the close to time period. We suggest a promote.

Preview

We beforehand coated Coursera in “Coursera: The Backside Might Be Close to” for the primary time in December 2022. Our thesis was the corporate has robust development momentum, however unfavorable earnings and money stream have been a priority, along with the next price propensity accompanied with the excessive development. We known as for a close to time period bottoming for the inventory to renew development, and gave a maintain advice. Its inventory certainly bottomed out at about $10 in 5 months and began to rise to presently $19.61.

Updates

Coursera’s efficiency in 2023 might be its finest but up to now with income rising on the strongest tempo and reaching the very best worth.

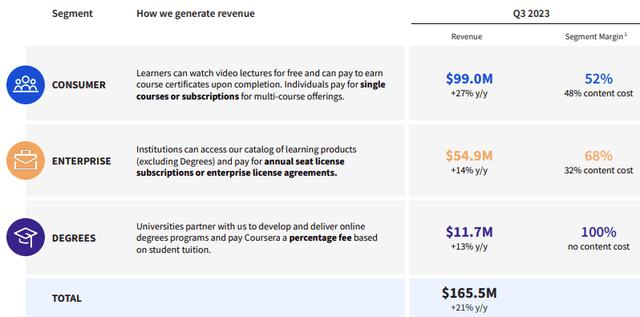

Coursera: Q3 Income By Section (Firm Q3 Presentation)

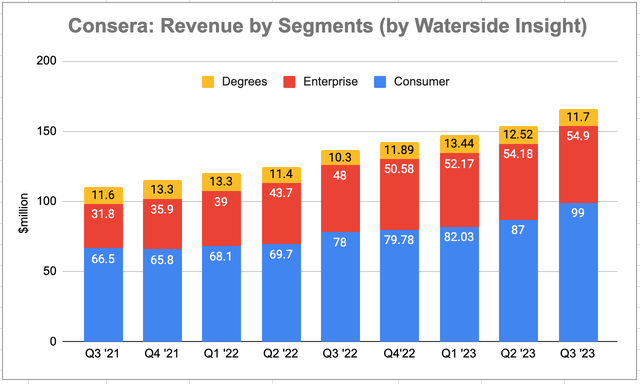

To replace our earlier charts on Coursera’s income by segments, the highest line development fee in 2023 has maintained a median 22% development YoY. The first driver was 25% YoY development from its Client phase, which accounted for 73% of its whole income.

Coursera: Income Historical past By Section (Calculated and Charted by Waterside Perception with information from firm)

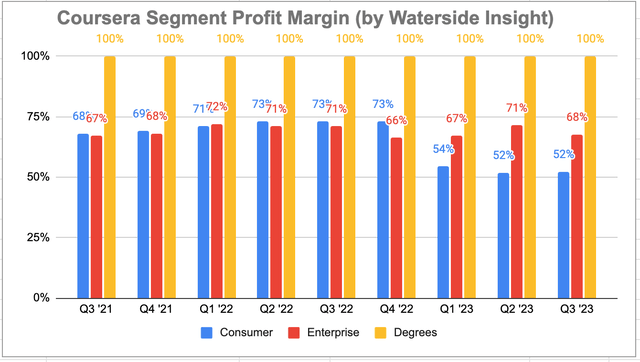

The phase margin, nonetheless, was a slip, most notably in Client, falling from 73% a yr in the past to 52%. This phase bears the many of the content material price as most of its content material was began with catering to particular person learners. The margin in Enterprise held up. We mentioned earlier than that its Diploma phase, which is a reconfiguration of current content material into diploma packages in partnership with universities, bears no content material creation price and is all the time 100% margin. Coursera has been making enlargement for the Levels this yr. The corporate introduced a partnership with the College of Texas to launch a micro-credential program in the summertime, which targets the 240,000 learners within the UT system.

Coursera: Section Revenue Margin Historical past (Calculated and Charted by Waterside Perception with information from firm)

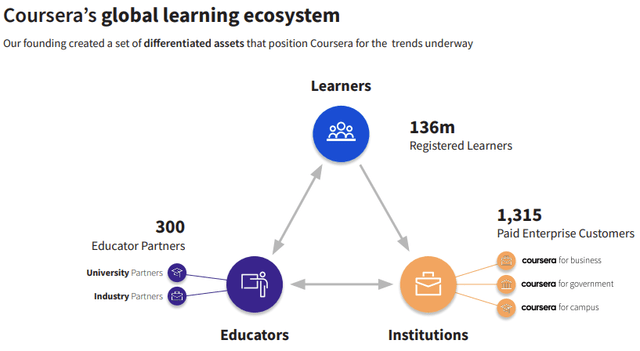

The Client phase is mainly the bread-and-butter to Coursera. With over 136 million registered customers, their preferences and demand drive the location’s content material and development instructions. Most of its content material first getting used and filtered by the person learners’ expertise earlier than being packaged into Enterprise clients or Diploma seekers’ content material, not solely as a result of the person learners replicate extra dynamical shifts in essentially the most in-demand expertise but in addition the route of the place it’s going. So the blunt of this phase’s margin signifies the true price of the content material creation for the corporate. For instance, its platform is AI-powered. The outcomes could comprise inaccuracy or deceptive attributes. When being absent of adequate and cost-effective strategies to detect and stop a few of the dangers, growing new contents is probably not as scale-able and far-reaching to completely different topics with out incurring larger prices. So the most effective path of bettering margin and profitability continues to be but refitting its obtainable content material to completely different sort of customers, corresponding to Enterprise and Universities. The sooner development in these two segments can result in larger general margin, though for this yr their development charges are solely half of the Client phase.

Coursera: International Studying Ecosystem (Firm Q3 Presentation)

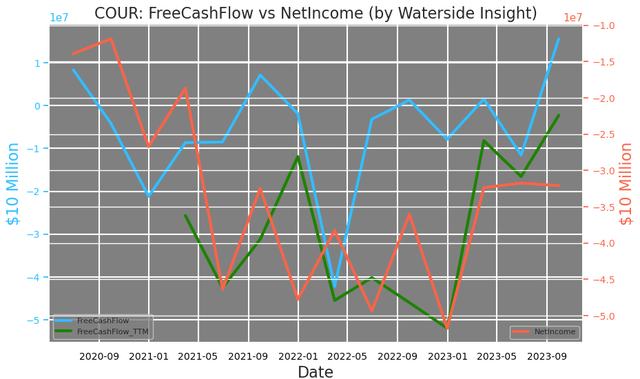

This yr it marked a powerful pickup for Coursera, not solely from decreasing its internet loss but in addition pulling its free money stream decisively into the constructive. The efforts the corporate has made to enhance income.

Coursera: Free Money Move vs Web Revenue (Calculated and Charted by Waterside Perception with information from firm)

It has made no discount in prices of income, however moderated the R&D bills, which resulted in a flattening working bills. However because the income development has been sooner, general prices and bills’ proportion has turn out to be much less by about 4% on a TTM foundation since final yr. This was one of many areas we have been involved about, and it appears to be underneath higher management in help of the margin development.

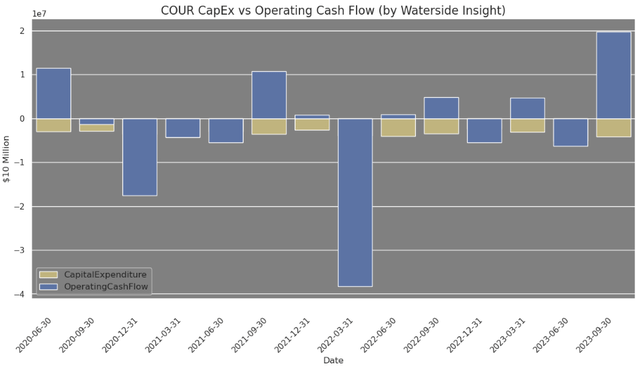

Sturdy working money stream development has pushed the degrees above its earlier vary, however the CapEx stays related. This resulted in a a lot stronger free money stream within the latest quarter. In addition to over 20% discount of internet loss, the corporate additionally has been utilizing extra credit in paying its distributors and contractors, leading to an nearly 70% improve in accounts payable, a provision to its operational money stream. These are the 2 most important components that helped enhance its working money stream. We expect Coursera has a great likelihood to remain free money stream constructive this yr, however not with out related volatility to the previous two years.

Coursera: CapEx vs Working Money Move (Calculated and Charted by Waterside Perception with information from firm)

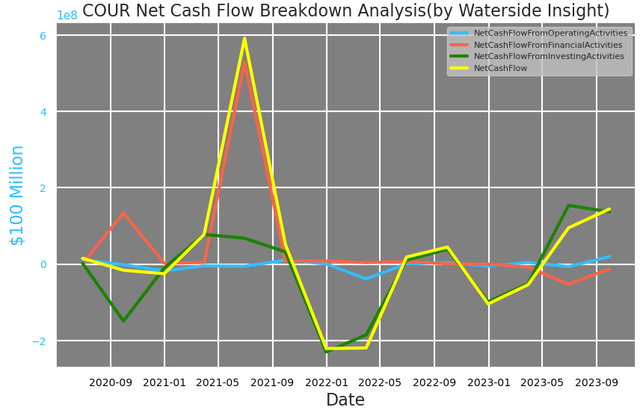

On prime of stronger working money stream, Coursera additionally sees one of many largest will increase of its money stream from investing actions. It had $388 million of proceed from the sale of marketable securities, which helped lifting its whole investing money stream to $240 million. It additionally made about $50 million in inventory repurchase as a reward to shareholders with an authorization to purchase again as much as $95 billion.

Coursera: Web Money Move Breakdown (Calculated and Charted by Waterside Perception with information from firm)

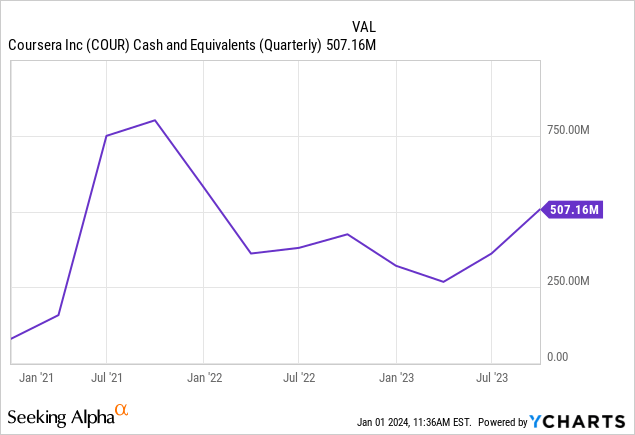

Its cash-at-hand on the finish of the interval has elevated by nearly $200 million because the finish of ’22, or over 80% QoQ in Q3. The replenishment of money place is the results of each stronger money stream and internet earnings. The corporate carries little debt, they’re largely short-term and long-term operational leasing obligations. Completely, its cash-to-debt ratio has risen from 50x to now 85x.

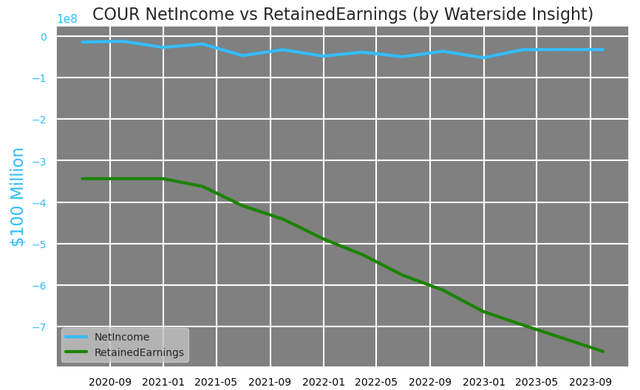

Coursera would not pay dividends, however its retained earnings have continued to say no in comparison with a extra steady internet earnings. By now, it a file unfavorable $700 million retained earnings by Q3 of final yr, 23% of its market cap on a quarterly foundation.

Coursera: Web Revenue vs Retained Earnings (Calculated and Charted by Waterside Perception with information from firm)

In abstract, Coursera’s enchancment in each earnings and money stream got here from each robust prime line development and efficient administration of its financials. Nevertheless, because it quickens development, there is a rise of price impacting it revenue margin. This goes again to our authentic concern that quick prime line development and elevated prices will nonetheless co-exist for the corporate.

Monetary Overview and Valuation

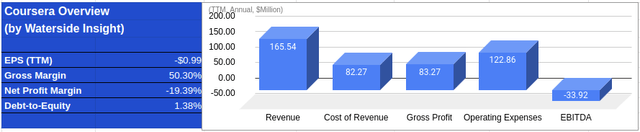

Coursera: Monetary Overview (Calculated and Charted by Waterside Perception with information from firm)

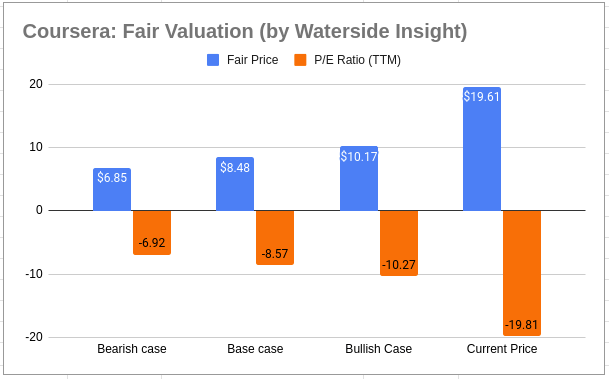

By the point it reviews this quarter, we count on Coursera will present its development in 2023 primarily hit our bullish case state of affairs estimated. We now have up to date our fashions based mostly on their enchancment final yr mentioned above, however stored the long run estimates intact. Honest costs for all three situations have been lifted. The bearish case has moved from $5.89 to $6.85, base case from $7.48 to $8.48, and the bullish case from $9.65 to $10.17. This largely mirrored the constructive free money stream in Q1 and Q3 of final yr whereas count on additionally constructive for This fall. Nevertheless, we’re cautious about the price construction that comes with quick enlargement, which is able to constrain its pace and high quality of development. We consider all above and projecting its prime line and earnings may develop into about 20x greater than its present degree in ten years, but we nonetheless can not match the market’s lofty valuation of $19.61. We expect the inventory is grossly overvalued at this level.

Coursera: Honest Valuation (Calculated and Charted by Waterside Perception with information from firm)

Conclusion

We’re optimistic about Coursera’s development and have been primarily proper to foretell it may get well this yr, leading to a shopping for alternative. However the market has entrance run itself within the inventory value with a excessive premium that’s laborious to match too even when the corporate makes no mistake and has no burden of accelerating price for earnings erosion. We’ll suggest a promote at this second.

{kind=link}