JHVEPhoto/iStock Editorial by way of Getty Photos

Funding Thesis

Concurrently incorporating into your funding portfolio one firm that gives a comparatively engaging Dividend Yield and one that gives dividend progress brings traders the advantages of mixing dividend revenue with dividend progress.

I’ve utilized this technique with the latest acquisitions of Nike (NYSE:NKE) and Exxon Mobil (NYSE:XOM). Together with them in The Dividend Revenue Accelerator Portfolio has been strategically vital.

Whereas Exxon Mobil will primarily contribute to the technology of dividend revenue, Nike will contribute to the technology of dividend progress. Collectively, each firms not solely mix dividend revenue and dividend progress, however in addition they assist to reinforce diversification whereas lowering the portfolio’s sector particular focus threat. Via their incorporations into The Dividend Revenue Accelerator Portfolio, the share of the Financials Sector in comparison with the general portfolio has decreased from 33.07% to 30.56%.

Nike and Exxon Mobil’s strategic incorporations assist us to lower the general threat stage of The Dividend Revenue Accelerator Portfolio, and to boost the chance of attaining optimistic funding outcomes.

I’m satisfied that each Nike and Exxon Mobil strongly align with The Dividend Revenue Accelerator’s funding method. Each firms are well-positioned inside their respective industries, are financially wholesome (Nike reveals an A1 and Exxon Mobil an Aa2 credit standing from Moody’s), have robust aggressive benefits, and I take into account each to be at the moment undervalued (each firms’ P/E [FWD] Ratios stand under their common from the previous 5 years).

All these traits align with the funding method of The Dividend Revenue Accelerator Portfolio and match with its technique to speculate with a margin of security, placing capital preservation in first place.

Earlier than I introduce you to the 2 chosen firms in better element, I want to reiterate the traits of The Dividend Revenue Accelerator Portfolio. Those that are already conscious of the portfolio’s funding method can skip the next chapter written in italics.

The Dividend Revenue Accelerator Portfolio

The Dividend Revenue Accelerator Portfolio’s goal is the technology of revenue by way of dividend funds, and to yearly increase this sum. Along with that, its objective is to realize an interesting Whole Return when investing with a lowered threat stage over the long run.

The Dividend Revenue Accelerator Portfolio’s lowered threat stage might be reached because of the portfolio’s broad diversification over sectors and industries and the inclusion of firms with a low Beta Issue.

Under you could find the traits of The Dividend Revenue Accelerator Portfolio:

- Enticing Weighted Common Dividend Yield [TTM]

- Enticing Weighted Common Dividend Progress Price [CAGR] 5 Yr

- Comparatively low Volatility

- Comparatively low Threat-Degree

- Enticing anticipated reward within the type of the anticipated compound annual charge of return

- Diversification over asset lessons

- Diversification over sectors

- Diversification over industries

- Diversification over international locations

- Purchase-and-Maintain suitability

Nike

Nike was based in 1964 in Beaverton and is the world’s main sporting items producer when it comes to income and market capitalization. At present, Nike’s market capitalization stands at $164.43B, whereas Adidas’ (OTCQX:ADDYY) is presently at $36.20B.

Nike possesses a large number of aggressive benefits, reinforcing my perception that it’s going to maintain its place because the main sporting items producer within the coming years.

Nike’s notable aggressive benefits embrace its robust model picture: in line with Model Finance, Nike is at the moment the 54th most useful model on the earth. The corporate additionally advantages from long-term contracts with top-tier sports activities groups and athletes, its steady give attention to innovation, huge monetary well being (evidenced by an A1 credit standing from Moody’s), its rising focus in direct gross sales, and a world distribution community.

Nike’s wonderful place inside its business is mirrored within the firm’s excessive EBIT Margin [TTM] of 11.32%, which is 50.55% above the Sector Median (7.52%). It’s additional evidenced by a Return on Widespread Fairness of 33.91%, which is 197.77% above the Sector Median of seven.52%.

Nike’s Present Valuation

At this second in time, the corporate reveals a P/E [FWD] Ratio of 29.83. Its P/E [FWD] Ratio at the moment lies 17.25% under its common from the previous 5 years (36.04). This exhibits us that Nike is presently undervalued.

Nike’s undervaluation can also be underscored by the corporate’s Worth/Gross sales [FWD] Ratio of three.19, which stands 19.05% under its 5 yr common.

Nike’s Robust Progress Outlook

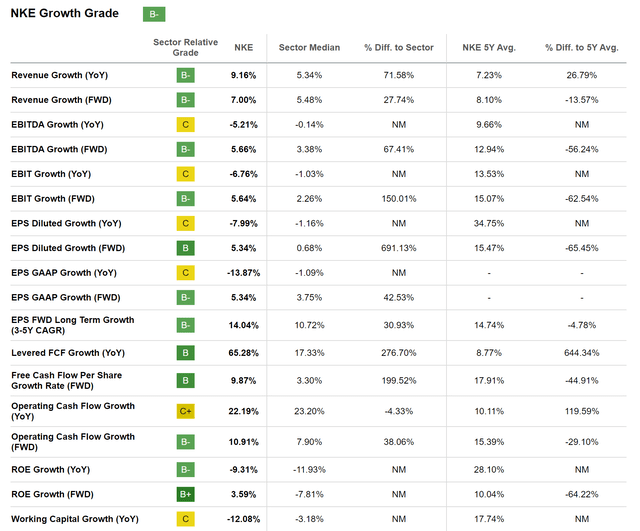

Completely different metrics point out that the corporate can also be a superb decide when it comes to progress: Nike has proven a Income Progress Price [FWD] of seven.00%, which is 27.74% above the Sector Median.

Along with that, it’s price mentioning that Nike’s EPS FWD Lengthy Time period Progress Price [3-5Y CAGR] stands at 14.04%, which is 30.93% above the Sector Median, additional underscoring my principle that the corporate’s progress outlook is optimistic.

Under you could find the In search of Alpha Progress Grade for Nike, which, as soon as once more, reaffirms the corporate’s promising progress prospects.

Supply: In search of Alpha

Nike’s Energy in Phrases of Dividend Progress

Nike’s spectacular dividend progress metrics strongly help my funding thesis, positioning the corporate as a key driver of dividend progress inside The Dividend Revenue Accelerator Portfolio.

Nike has proven a Dividend Progress Price 10Y [CAGR] of 12.32%, which is considerably above the Sector Median (8.14%).

Along with that, the corporate has produced an Common Free Money Movement Per Share Progress Price [FWD] of 17.91%, which additional underlines its potential of being a key driver of dividend progress inside The Dividend Revenue Accelerator Portfolio.

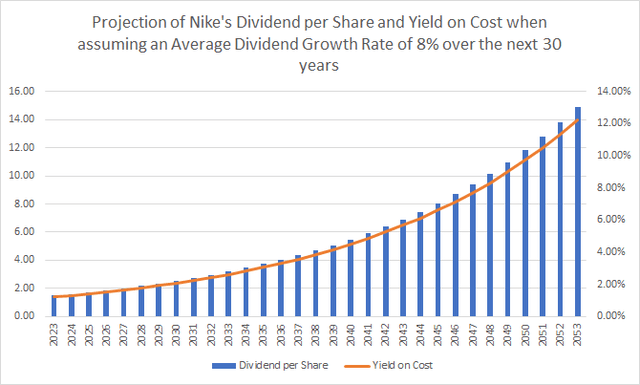

The graphic under illustrates a projection of Nike’s Dividend and Yield on Price when assuming an Common Dividend Progress Price of 8% for the subsequent 30 years. The chart demonstrates that traders may probably obtain a Yield on Price of two.63% in 2033, 5.67% in 2043, and 12.25% in 2053.

Supply: The Creator

Why I Have Chosen Nike Over Its Opponents

Nike’s wonderful place inside its business is mirrored in its greater EBIT Margin [TTM] (11.76%) when in comparison with Adidas (0.62%), Underneath Armour (NYSE:UA, NYSE:UAA) (5.09%) and Puma (OTCPK:PMMAF) (6.43%).

Nike additionally reveals a considerably greater Return on Widespread Fairness (36.03%) in comparison with any of those opponents: Adidas reveals a Return on Widespread Fairness of -2.29%, Underneath Armour’s is 5.09%, and Puma’s is 6.43%.

Along with that, it may be highlighted that Nike has a better Income Progress Price [FWD] (6.06%) compared to Adidas (3.32%), and Underneath Armour (1.75%), reflecting the corporate’s superiority when it comes to progress.

Nike’s 24M Beta Issue of 1.15 additional signifies that an funding comes hooked up to a decrease threat stage when in comparison with Adidas (24M Beta Issue of 1.34), Underneath Armour (1.55), and Puma (1.25).

All of those metrics underline my perception that Nike gives traders with probably the most engaging threat/reward profile, and with the very best chance of attaining profitable funding outcomes compared to its opponents. This strengthens my perception that the corporate is probably the most satisfactory alternative for The Dividend Revenue Accelerator Portfolio amongst its peer group.

Exxon Mobil

Exxon Mobil operates within the exploration and manufacturing of crude oil and pure gasoline. The corporate operates via the next segments:

- Upstream

- Vitality Merchandise

- Chemical Merchandise

- and Specialty Merchandise

Exxon Mobil’s Present Valuation

Exxon Mobil at the moment presents a P/E Non-GAAP [FWD] Ratio of 11.01, which is 31.12% under its common from the previous 5 years. This means that the corporate is presently undervalued. Exxon Mobil’s undervaluation is additional evidenced by a Worth/Money Movement [FWD] Ratio of seven.32, which is under its common from the previous 5 years (7.88).

Exxon Mobil’s Excessive Free Money Movement Yield

It might additional be highlighted that Exxon Mobil presently reveals a excessive Free Money Movement Yield [TTM] of 9.15%, indicating that the corporate gives traders with a lovely threat/reward profile. This excessive Free Money Movement Yield means that Exxon Mobil’s present share value is grounded in lifelike progress expectations, offering traders with a major margin of security.

Exxon Mobil’s Dividend Yield

At this second in time, the corporate gives its shareholders with a Dividend Yield [FWD] of three.75%. A comparatively low Payout Ratio of 34.87% additional signifies that Exxon Mobil has the potential to not solely be a lovely decide when it comes to dividend revenue, but additionally when it comes to dividend progress. This principle is additional underlined by its 10 Yr Dividend Progress Price [CAGR] of 4.11%.

A Projection of Exxon Mobil’s Dividend and Yield on Price

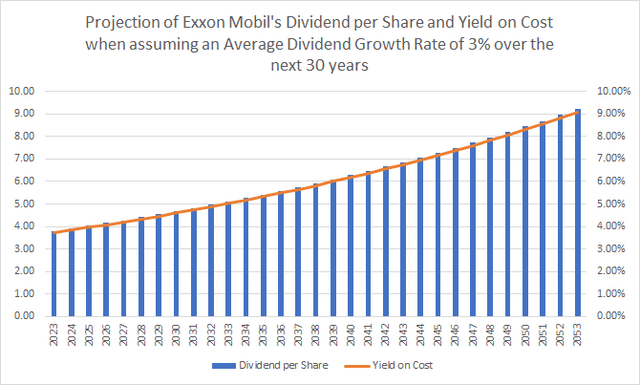

Under you could find a projection of Exxon Mobil’s Dividend and Yield on Price when assuming an Common Dividend Progress Price of three% for the next 30 years. This projection illustrates a possible Yield on Price of 5.02% by 2033, growing to six.75% by 2043, and to 9.07% by 2053.

Supply: The Creator

Why I Have Chosen Exxon Mobil Over Its Opponents

One of many principal causes for selecting Exxon Mobil over its competitor Chevron (NYSE:CVX) is that The Dividend Revenue Accelerator Portfolio is already invested in SCHD (NYSEARCA:SCHD), which holds a major stake in Chevron (the corporate at the moment accounts for 3.94% of SCHD).

Deciding on Exxon Mobil over Chevron for The Dividend Revenue Accelerator Portfolio contributes to sustaining a lowered company-specific focus threat, therewith growing the chance of optimistic funding outcomes.

Nevertheless, this isn’t the one purpose for which Exxon Mobil could possibly be the superior alternative compared to Chevron: Exxon Mobil has the marginally decrease 24M Beta Issue of 0.51 (when in comparison with Chevron’s 24M Beta Issue of 0.57). This means that Exxon Mobil is the selection with the marginally decrease threat stage, which, as soon as once more, will be seen as an indicator of an elevated likelihood for optimistic funding outcomes.

Along with that, I see Exxon Mobil as being barely superior on the subject of Profitability, which is mirrored within the firm’s barely greater Return on Widespread Fairness of 21.17% (in comparison with Chevron’s 15.68%).

Why Nike and Exxon Mobil Align With the Funding Method of The Dividend Revenue Accelerator Portfolio

- Each Nike and Exxon Mobil have vital aggressive benefits and are well-positioned inside their industries. This aligns with the funding method of The Dividend Revenue Accelerator Portfolio to put money into the highest gamers of its respective industries.

- Moreover, it may be highlighted that Exxon Mobil primarily contributes to the revenue technology of The Dividend Revenue Accelerator Portfolio, whereas Nike will predominantly contribute to the portfolio’s dividend progress. Each firms are vital strategic acquisitions for the profitable implementation of The Dividend Revenue Accelerator Portfolio, combining dividend revenue with dividend progress.

- Each Nike and Exxon Mobil are financially wholesome, mirrored by their A1 and Aa2 credit standing from Moody’s respectively. This aligns with the portfolio’s funding method of prioritizing capital preservation.

- Nike and Exxon Mobil’s monetary well being is additional underscored by their Return on Widespread Equities of 33.91% and 21.17% respectively.

- I take into account each firms to at the moment be undervalued, aligning with the funding method of The Dividend Revenue Accelerator Portfolio to speculate with a margin of security, as soon as once more, prioritizing capital preservation for traders.

- Each firms have a optimistic progress outlook, mirrored by their Income Progress Charges [FWD] of seven.00% (Nike) and seven.32% (Exxon Mobil). This matches the funding method of The Dividend Revenue Accelerator Portfolio to put money into firms with engaging progress prospects.

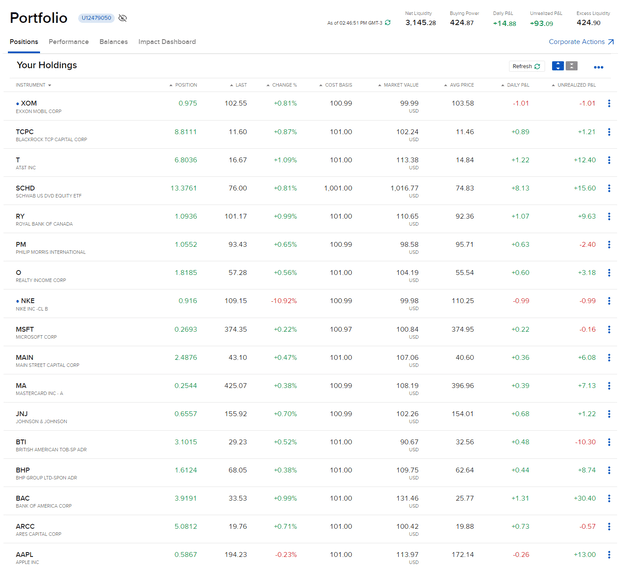

Investor Advantages of The Dividend Revenue Accelerator Portfolio After Investing $100 in Nike and $100 in Exxon Mobil

Under you could find an summary of the present composition of The Dividend Revenue Accelerator Portfolio after incorporating each Nike and Exxon Mobil.

Supply: Interactive Brokers

After the incorporation of Nike and Exxon Mobil, we have now additional elevated the portfolio’s diversification and therewith lowered its threat stage.

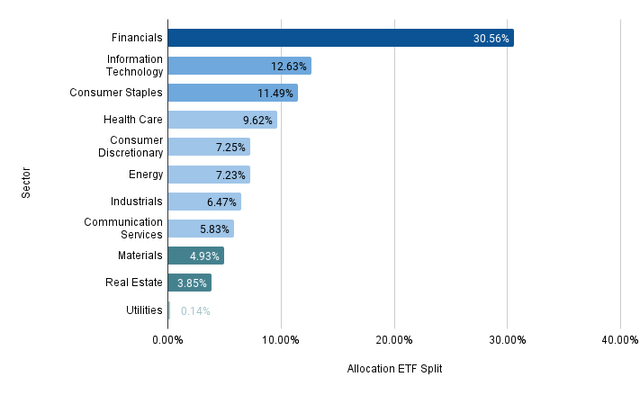

The graphic under illustrates the present sector allocation of The Dividend Revenue Accelerator Portfolio when allocating SCHD throughout the businesses and sectors it’s invested in.

Supply: The Creator, information from In search of Alpha and Morningstar

By including Nike and Exxon Cellular, the share of the Financials Sector in comparison with the general portfolio has decreased from 33.07% to 30.56%. This means that we have now managed to extend the diversification whereas decreasing the sector particular focus threat of The Dividend Revenue Accelerator Portfolio. The Shopper Discretionary Sector has elevated from 3.77% to 7.25% and the Vitality Sector has elevated from 3.51% to 7.23%.

After the inclusion of Nike and Exxon Mobil, it may be highlighted that the Weighted Common Dividend Yield [TTM] of the portfolio has solely barely decreased from 4.56% to 4.40%. The portfolio’s 5 Yr Weighted Common Dividend Progress Price [CAGR] has barely decreased from 9.12% to eight.95%. Regardless of this lower, The Dividend Revenue Accelerator Portfolio continues to offer traders with a lovely mixture of dividend revenue and dividend progress.

Conclusion

I take into account each Nike and Exxon Mobil to be vital strategic acquisitions for The Dividend Revenue Accelerator Portfolio.

With their inclusion, we efficiently steadiness dividend revenue and dividend progress inside The Dividend Revenue Accelerator Portfolio. Along with that, each firms boast notable aggressive benefits and have robust market positions inside their respective industries. Furthermore, each are financially wholesome (evidenced by Nike and Exxon Mobil’s A1 and Aa2 credit standing from Moody’s), and I take into account each firms to be undervalued (their present P/E [FWD] Ratio is under their 5 Yr Common).

Along with that, with the inclusion of Nike and Exxon Mobil, we have now managed to extend the extent of diversification of The Dividend Revenue Accelerator Portfolio. That is the case since we have now managed to cut back the share of the Financials Sector in comparison with the general portfolio from 33.07% to 30.56%.

Via their incorporation, the proportion of The Shopper Discretionary Sector and the Vitality Sector have elevated from 3.77% to 7.25% and from 3.51% to 7.23% respectively, as soon as once more, indicating an elevated stage of diversification for the general portfolio.

Because of Nike and Exxon Mobil’s notable aggressive benefits, their engaging Valuations, and their comparatively low funding threat ranges, I’m satisfied that each firms boast a lovely threat/reward profile. This makes them compelling decisions for traders generally and for The Dividend Revenue Accelerator Portfolio specifically.

Exxon Mobil’s Free Money Movement Yield [TTM] of 9.15% reinforces my view that the corporate presents traders a positive steadiness of threat and reward.

Given Nike and Exxon Mobil’s engaging threat/reward profile, I’m satisfied that each are vital strategic acquisitions, positioned to considerably contribute to The Dividend Revenue Accelerator Portfolio’s purpose of attaining a lovely Whole Return with a excessive chance.

Along with that, I take into account the businesses’ dividends to be comparatively secure, evidenced by Nike and Exxon Mobil’s Payout Ratios of 41.98% and 34.87% respectively. Their comparatively low Payout Ratios point out that the likelihood of a dividend reduce is comparatively low for each, additional underscoring their low threat stage.

In January 2024, I’ll add further firms to The Dividend Revenue Accelerator Portfolio, which can assist us to raise the portfolio’s diversification additional and cut back its risk-level. Doing so will permit us to constantly keep a excessive likelihood of profitable funding outcomes for individuals who implement the funding method of The Dividend Revenue Accelerator Portfolio.

Creator’s Observe: Thanks for studying! I might recognize listening to your opinion on my choice of Nike and Exxon Mobil as the newest acquisitions for The Dividend Revenue Accelerator Portfolio. Be happy to share any ideas about The Dividend Revenue Accelerator Portfolio or to share any suggestion of firms that may match into its funding method! I want you and your households all one of the best for 2024!