")

Sundry Pictures/iStock Editorial through Getty Photographs

Funding Thesis

Most massive banks are riskier than they seem, regardless of regulators and politicians who promise to stabilize a system that crashes with the regularity of a Swiss watch. I typically avoid the sector.

Schwab (NYSE:SCHW) is certainly a big financial institution, however on a unique mission and with different priorities. The belongings on the stability sheet are boring, plain vanilla, which might be held to maturity. Whereas there may be strain on present earnings from “money sorting” depositors, this has been transparently acknowledged by administration for months now. There may be additionally proof that Schwab and different massive establishments are attracting new deposits from accounts fleeing smaller banks.

My buy of the inventory and promoting of coated calls on the place displays my opinion that the pullback in SCHW shares is overdone however may also take a while to get better. A big contagion threat doesn’t exist in Charles Schwab’s banking operations, however a extra widespread market correction might impression its brokerage enterprise.

Banks Are Fragile

Banks have traditionally been led by very conservative-looking administration on the prime ranks, with probably extra down-to-earth tellers with nice smiles greeting depositors. Behind the scenes are primarily opaque stability sheets, typically obscuring unique derivatives, typically vetted by Nobel-winning economists, that generate charges and revenue and ticking time bombs.

I contemplate the time period “banking” to be deceptive because it refers to numerous actions, from offering an alternative choice to mattresses and cookie jars to creating and promoting devices that require a whole lot of pages to doc as a result of they’re so sophisticated.

Even the only type of banking requires the collective confidence of its prospects to perform. The fractional-reserve banking system idea boils right down to this: for each greenback a financial institution receives in buyer deposits, it holds solely a fraction in “liquid” reserves to satisfy common withdrawals. The remaining funds are then lent to debtors primarily based on the financial institution’s evaluation of the riskiness of the loans. Depositors earn curiosity priced on the short-term nature of demand deposits, and debtors pay the next charge to replicate default threat and the longer period of their loans. The financial institution earns the distinction between the curiosity it expenses debtors and the curiosity it pays depositors. In a capitalist society corresponding to ours, this technique accelerates the economic system by shifting the capital from savers to income-producing belongings quicker than these belongings produce revenue. In brief, it leverages capital.

What concerning the fraction of deposits held in liquid reserves? Such liquid funds needs to be short-term and never topic to cost fluctuation. In different phrases, below the financial institution’s mattress or in its cookie jar, presumably in a safer location than my home. Money and U.S. Treasury payments come to thoughts. Understand that the fraction of deposits in such liquid reserves to satisfy potential redemptions is predicated on regulatory necessities and anticipated or forecasted wants.

The truth is that this technique is topic to the cyclicality of the economic system. In a downturn, financial savings decline, inflicting deposits to dwindle. On the similar time, mortgage defaults could improve because the leveraged belongings don’t produce the anticipated revenue. So the underside line is that even a “easy” banking mannequin is topic to threat and that this threat stems from making predictions of the long run returns from the loan-funded belongings and the steadiness of the demand deposits which fund these loans.

What makes this technique much more fragile is the incentives inherent within the system. Competitors amongst banks for depositors leads new entrants to supply increased charges to depositors and prolong riskier loans to debtors. And that’s just for conventional banking operations. As talked about, probably the most outstanding “banks” go far past that easy lending mannequin to create unique merchandise and spinoff securities to generate payment revenue that usually doesn’t even serve the shopper’s curiosity. I plan to broaden on this space in different articles, however for the scope of my thesis on SCHW, it’s tangential.

For this text, the takeaway right here needs to be that even peculiar financial institution operations are topic to cyclicality. The chance of a “run on the financial institution” all the time exists in fractional banking regardless of the numerous previous crises and ensuing rules.

So Why Purchase Charles Schwab?

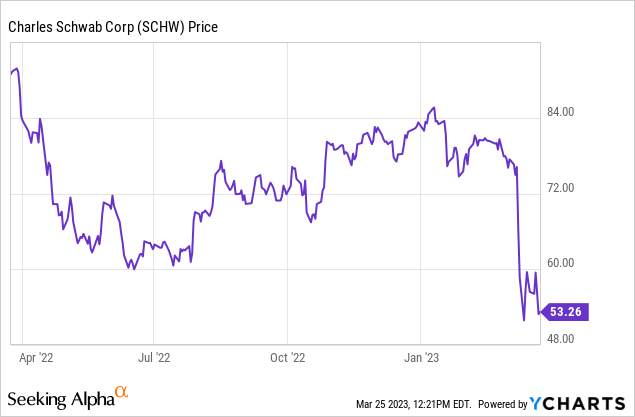

SCHW has been caught up within the general downdraft within the valuation of monetary firms throughout the spectrum.

Earlier than the newest banking disaster ignited by the collapse of SVB, Schwab was already grappling with challenges corresponding to regulatory adjustments to “fee for order circulate” guidelines and “money sorting” prospects shifting deposits to higher-yielding cash market funds. Regardless of these headwinds, the market rewarded the corporate with increased valuations because it grew and attracted extra shoppers and belongings.

As a broker-dealer, SCHW isn’t primarily a financial institution, though it’s labeled and controlled as one. As mentioned above, I don’t maintain particular person common banks in very excessive regard, though I acknowledge that the banking system is significant to the functioning of our economic system. In contrast to conventional banks, Schwab solely invests a small portion of its extra reserves in industrial and actual property loans, as this isn’t the corporate’s most important line of enterprise. As an alternative, 85% of SCHW’s belongings are in high-quality authorities and company securities.

Satirically, these belongings have additionally been scrutinized not too long ago because the concentrate on financial institution portfolios has turned to unrealized losses in held-to-maturity investments. With over 80% of Schwab Financial institution’s deposits totally FDIC insured and 95% of the roughly $7.4 Trillion of AUM at Schwab in segregated custodial broker-dealer accounts, there may be little motive to imagine there could be a “run on the financial institution” prevalence. Subsequently, there may be additionally little or no probability that any of the investments must be bought and the unrealized losses turn into realized.

This is a crucial level. The deposits at Schwab are there to facilitate buyer buying and selling and investing exercise, to not act as a main checking account. So whereas “money sorting” does strain one supply of SCHW’s earnings, the funds should not leaving the agency. The corporate has reported web inflows for the reason that disaster started. With over $7 Trillion in shopper belongings, I’m assured Schwab will discover methods to make cash serving these prospects.

My Commerce

I wakened this previous Friday to the information that credit score default swaps on Deutsche Financial institution (DB) had been rising, pressuring its share value and people of U.S. banks. And this spilled over once more to SCHW shares, regardless of not being an interconnected multinational monetary heart. True, any occasion that additional strains the economic system and monetary markets dangers additionally affecting Schwab’s brokerage exercise. Additionally it is doable that, like different massive establishments, the corporate would possibly proceed to draw web new belongings from smaller, much less well-capitalized banks and finally profit.

That mentioned, I bought SCHW shares within the pre-market (one other factor I hardly ever do) at a median value of $51.80. Throughout common market hours, the inventory recovered its intraday losses, buying and selling as much as $54 and alter. I then wrote (bought) April 21’23 $60 Calls in opposition to my holdings, gathering a web premium of $1.67 per share. This made my efficient web price $50.13, with the potential of the inventory being known as away for a 28-day return of 19.7%. As with all my coated calls, I’ll monitor occasions main as much as the expiration to determine whether or not to roll the choices to an extra date, repurchase them, or let the place go.