")

jetcityimage

Oct. 23, 2023 12:44 PM ET

|

About: The Charles Schwab Company (SCHW)

Cavenagh Analysis

Lengthy/Brief Fairness, Development At A Cheap Worth, Contrarian, Portfolio Technique

Abstract

Charles Schwab reported a 44% YoY contraction in EPS for Q3, confirming issues about earnings stress.

The corporate’s inventory has underperformed the market and is predicted to proceed buying and selling decrease.

Schwab’s earnings are being impacted by refinancing stress and shopper money sorting exercise, resulting in liquidity wants on increased rates of interest.

With Q3 insights and NIM visibility, my residual earnings mannequin suggests a base-case goal value for Schwab inventory of about $42.39 per share.

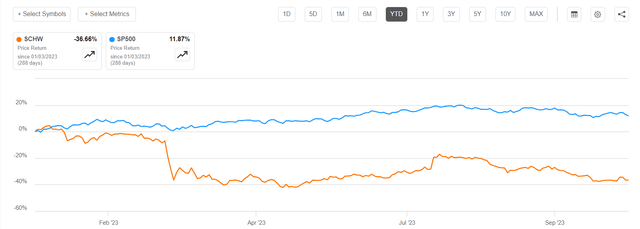

I’ve beforehand argued that Charles Schwab has mismanaged the period in its securities bond portfolio, and refinancing stress at increased charges to satisfy shopper money sorting demand will possible stress the firm’s earnings via 2025. Now, after Schwab reported Q3 outcomes, I revisit my thesis; And with Schwab posting a 44% YoY contraction in EPS, I really feel broadly confirmed in my evaluation that the earnings thesis is enjoying out as anticipated. That mentioned, SCHW inventory has underperformed the broader market YTD, with the inventory down about 37% in comparison with a achieve of 12% for the S&P 500 (SP500). Over the subsequent 12-18 months, I see SCHW inventory step by step buying and selling decrease nonetheless, approaching my newly set goal value of $42.39/ share.

Looking for Alpha

Schwab’s Q3 – Evaluate

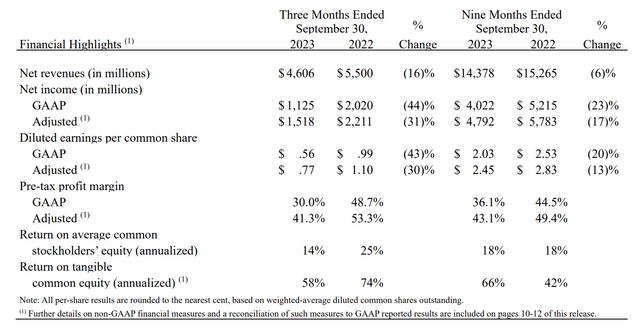

After a tumultuous Q2, Schwab reported a disappointing set of Q3 outcomes, lacking analyst consensus on each topline and GAAP earnings. Throughout the interval spanning June to finish of September, Schwab generated about $4.6 billion of revenues, down 16% YoY in comparison with the identical quarter one yr earlier, and lacking consensus by roughly $10 million (with analyst consensus being already fairly bearish following the SVB collapse). For the trailing 9 months, revenues are down 6% yr over yr.

When it comes to profitability, Schwab posted $1.1 billion of GAAP web earnings, virtually halved in comparison with the $2 billion achieved one yr earlier (-44%, and even decrease than what most – already bearish analysts – anticipated, lacking by about $100 million (-10%). To provide some extra context in regards to the firm’s profitability: pre-tax revenue margin dropped 1,860 foundation factors, to 30% versus 48.7% in Q3 2022; return on tangible frequent fairness dropped 1,600 foundation factors, respectively, to 58%.

Schwab Q3 2023 reporting

Schwab Co-Chairman and CEO Walt Bettinger attributed the muted Q3 outcomes to a

difficult financial and geopolitical backdrop

citing

… a interval the place the U.S. authorities narrowly prevented a shutdown, main fairness markets posted a quarterly loss, and long-term rates of interest touched ranges not seen in a few years.

Whereas connecting Schwab’s underperformance to a difficult financial backdrop could also be convincing to some, I don’t see it that means. I’d remind traders that market turbulences are normally very quantity accretive to buying and selling, whereas uncertainty is accretive to wealth administration, whereas increased rates of interest are accretive to earnings from margin lending. In that context, Schwab ought to have been capable of seize no less than a number of the upside. Different giants within the monetary companies business similar to J.P.Morgan Chase, Citi and Wells Fargo posted very sturdy outcomes for the September quarter. And e-brokerage competitor Interactive Brokers blew earnings estimates out of the park on a 58% YoY soar in web curiosity earnings from margin lending.

On a extra constructive notice, Schwab managed to build up $46 billion in core web new belongings, with a considerable $27 billion inflow occurring in September following the profitable Ameritrade shopper conversion. Yr to this point, Schwab has now captured a formidable inflow of $248 billion in core web new belongings, translating into an annualized natural progress price of over 6% YoY. As of September 30, Schwab’s purchasers have entrusted the corporate with a complete of $7.82 trillion in belongings, distributed throughout 34.5 million accounts.

Financing Stress Nonetheless The Main Headwind, Albeit Easing

Schwab’s earnings are down in Q3 2023 YoY, and that is largely a operate of the financial institution’s refinancing and liquidity want linked to shopper money sorting exercise. As rates of interest began to rise, and billions value of Schwab shopper deposits began chasing higher-yielding funding alternatives, Schwab was left to satisfy the liquidity demand financing its stability sheet with CDs and different devices, reportedly paying nicely above 5% in curiosity. In the meantime, a big share of Schwab’s liquid belongings is invested in securities whose curiosity yield carries reminiscence from the low/-zero price setting main as much as COVID. For sure, this dynamic places stress on Schwab’s earnings.

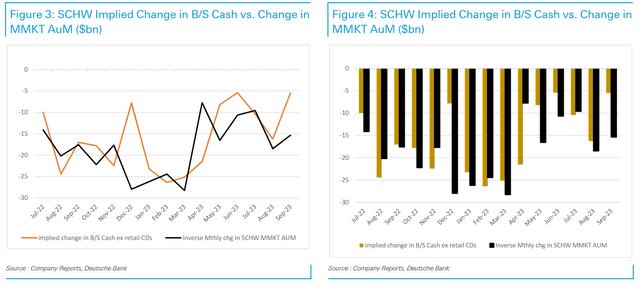

With the body of reference above, Deutsche Financial institution’s fairness analysis staff led by Brian Bedell, CFA (analysis notice on SCHW dated 16 October) did a superb job visualizing how Schwab’s purchasers have step by step and persistently drawn down deposits held with the corporate — and the outflow nonetheless continues, albeit now at a slowing tempo. It’s also fascinating to see how strongly deposit outflows are correlated to cash market inflows.

Deutsche Financial institution Fairness Analysis

To be honest, following a short surge in money sorting actions noticed in August, the speed of exercise considerably decelerated in September. Consumer deposits on the stability sheet solely noticed an approximate $5 billion outflows in September, in distinction to the $16 billion outflow in August. With money sorting exercise additionally considerably supported by the gradual maturing of Schwab’s securities portfolio, the wealth administration and brokerage big managed to cut back the quantity of excellent supplemental funding. By the top of the third quarter in 2023, the FHLB stability stood at $31.8 billion, reflecting a $9.2 billion lower from the top of the second quarter. CDs, nevertheless, nonetheless remained at ranges according to Q2, at roughly $44.5 billion. Thus, general, Schwab’s web curiosity earnings remained pressured, with 3Q NIM being reported at only one.94%. Based on administration steering, it’s going to possible take two years of gradual the “non permanent borrowing” redemption, and resumption of securities portfolio reinvestments, till the corporate’s NIM strengthens again to (hopefully) 3.00% by the top of 2025.

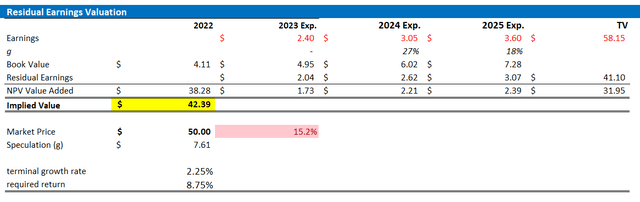

Residual Earnings Mannequin

With stability sheet changes slowing, and administration highlighting a path in the direction of 2025 NIM projections, I really feel assured valuing Schwab inventory primarily based on a residual earnings mannequin. As per the CFA Institute:

Conceptually, residual earnings is web earnings much less a cost (deduction) for frequent shareholders’ alternative value in producing web earnings. It’s the residual or remaining earnings after contemplating the prices of all of an organization’s capital.

With regard to my Charles Schwab inventory valuation mannequin, I make the next assumptions:

- To forecast EPS, I anchor on the consensus analyst forecast as out there on the Bloomberg Terminal ‘until 2025. For my part, any estimate past 2025 is simply too speculative to incorporate in a valuation framework. However for 2-3 years, the analyst consensus is normally fairly exact.

- To estimate the capital cost, I anchor on Schwab’s value of fairness at 8.75%.

- For the terminal progress price after 2025, I apply 2.25%, which I consider is an inexpensive estimate post-2025 (roughly according to U.S. nominal GDP progress).

- Buyers with totally different assumptions relating to Schwab’s value of capital and terminal progress could take reference from the sensitivity desk enclosed.

Given the above assumptions, I calculate a base-case goal value for Schwab inventory of about $42.39/share, suggesting 15% draw back.

Firm Financials; Writer’s EPS Estimates; Writer’s Calculation

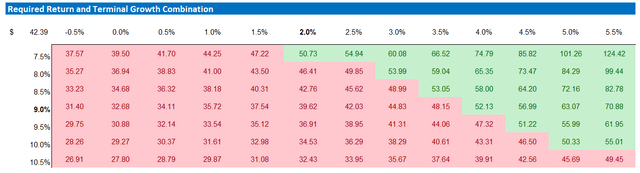

My base case projection for SCHW’s goal value implies draw back. Nevertheless, it’s essential for traders to judge the danger and reward ratio of investing in an organization primarily based on a ‘state of affairs’ view. To evaluate totally different situations primarily based on numerous assumptions, I’ve created a sensitivity desk that analyzes SCHW’s value of fairness and terminal progress price. See under.

Firm Financials; Writer’s EPS Estimates; Writer’s Calculation

Conclusion

In my prior evaluation of Charles Schwab, I raised issues in regards to the administration of the period in its securities bond portfolio and the potential earnings stress ensuing from refinancing wants at increased rates of interest and shopper money sorting exercise. After reviewing Schwab’s Q3 outcomes, my earlier thesis seems to be on monitor, with the corporate reporting a 44% YoY contraction in EPS. The earnings stress continues to be primarily anchored on headwinds from financing, that are anticipated to stay fairly sticky, solely step by step fading via 2025. With Q3 insights and NIM visibility, my residual earnings mannequin suggests a base-case goal value for Schwab inventory of about $42.39 per share, indicating roughly 15% draw back. As a consequence, I proceed advising to keep away from SCHW inventory.

Analyst’s Disclosure: I/we now have no inventory, choice or related spinoff place in any of the businesses talked about, and no plans to provoke any such positions throughout the subsequent 72 hours. I wrote this text myself, and it expresses my very own opinions. I’m not receiving compensation for it (apart from from Looking for Alpha). I’ve no enterprise relationship with any firm whose inventory is talked about on this article.

not monetary advise

Looking for Alpha’s Disclosure: Previous efficiency is not any assure of future outcomes. No advice or recommendation is being given as as to if any funding is appropriate for a specific investor. Any views or opinions expressed above could not mirror these of Looking for Alpha as a complete. Looking for Alpha is just not a licensed securities supplier, dealer or US funding adviser or funding financial institution. Our analysts are third occasion authors that embody each skilled traders and particular person traders who might not be licensed or licensed by any institute or regulatory physique.

I’ve beforehand argued that Charles Schwab has mismanaged the period in its securities bond portfolio, and refinancing stress at increased charges to satisfy shopper money sorting demand will possible stress the corporate’s earnings via 2025. Now, after Schwab reported Q3 outcomes, I revisit my thesis; And with Schwab posting a 44% YoY contraction in EPS, I really feel broadly confirmed in my evaluation that the earnings thesis is enjoying out as anticipated. That mentioned, SCHW inventory has underperformed the broader market YTD, with the inventory down about 37% in comparison with a achieve of 12% for the S&P 500 (SP500). Over the subsequent 12-18 months, I see SCHW inventory step by step buying and selling decrease nonetheless, approaching my newly set goal value of $42.39/ share.

Looking for Alpha

Schwab’s Q3 – Evaluate

After a tumultuous Q2, Schwab reported a disappointing set of Q3 outcomes, lacking analyst consensus on each topline and GAAP earnings. Throughout the interval spanning June to finish of September, Schwab generated about $4.6 billion of revenues, down 16% YoY in comparison with the identical quarter one yr earlier, and lacking consensus by roughly $10 million (with analyst consensus being already fairly bearish following the SVB collapse). For the trailing 9 months, revenues are down 6% yr over yr.

When it comes to profitability, Schwab posted $1.1 billion of GAAP web earnings, virtually halved in comparison with the $2 billion achieved one yr earlier (-44%, and even decrease than what most – already bearish analysts – anticipated, lacking by about $100 million (-10%). To provide some extra context in regards to the firm’s profitability: pre-tax revenue margin dropped 1,860 foundation factors, to 30% versus 48.7% in Q3 2022; return on tangible frequent fairness dropped 1,600 foundation factors, respectively, to 58%.

Schwab Q3 2023 reporting

Schwab Co-Chairman and CEO Walt Bettinger attributed the muted Q3 outcomes to a

difficult financial and geopolitical backdrop

citing

… a interval the place the U.S. authorities narrowly prevented a shutdown, main fairness markets posted a quarterly loss, and long-term rates of interest touched ranges not seen in a few years.

Whereas connecting Schwab’s underperformance to a difficult financial backdrop could also be convincing to some, I don’t see it that means. I’d remind traders that market turbulences are normally very quantity accretive to buying and selling, whereas uncertainty is accretive to wealth administration, whereas increased rates of interest are accretive to earnings from margin lending. In that context, Schwab ought to have been capable of seize no less than a number of the upside. Different giants within the monetary companies business similar to JPMorgan Chase, Citi and Wells Fargo posted very sturdy outcomes for the September quarter. And e-brokerage competitor Interactive Brokers blew earnings estimates out of the park on a 58% YoY soar in web curiosity earnings from margin lending.

On a extra constructive notice, Schwab managed to build up $46 billion in core web new belongings, with a considerable $27 billion inflow occurring in September following the profitable Ameritrade shopper conversion. Yr to this point, Schwab has now captured a formidable inflow of $248 billion in core web new belongings, translating into an annualized natural progress price of over 6% YoY. As of September 30, Schwab’s purchasers have entrusted the corporate with a complete of $7.82 trillion in belongings, distributed throughout 34.5 million accounts.

Financing Stress Nonetheless The Main Headwind, Albeit Easing

Schwab’s earnings are down in Q3 2023 YoY, and that is largely a operate of the financial institution’s refinancing and liquidity want linked to shopper money sorting exercise. As rates of interest began to rise, and billions value of Schwab shopper deposits began chasing higher-yielding funding alternatives, Schwab was left to satisfy the liquidity demand financing its stability sheet with CDs and different devices, reportedly paying nicely above 5% in curiosity. In the meantime, a big share of Schwab’s liquid belongings is invested in securities whose curiosity yield carries reminiscence from the low/-zero price setting main as much as COVID. For sure, this dynamic places stress on Schwab’s earnings.

With the body of reference above, Deutsche Financial institution’s fairness analysis staff led by Brian Bedell, CFA (analysis notice on SCHW dated 16 October) did a superb job visualizing how Schwab’s purchasers have step by step and persistently drawn down deposits held with the corporate — and the outflow nonetheless continues, albeit now at a slowing tempo. It’s also fascinating to see how strongly deposit outflows are correlated to cash market inflows.

Deutsche Financial institution Fairness Analysis

To be honest, following a short surge in money sorting actions noticed in August, the speed of exercise considerably decelerated in September. Consumer deposits on the stability sheet solely noticed an approximate $5 billion outflows in September, in distinction to the $16 billion outflow in August. With money sorting exercise additionally considerably supported by the gradual maturing of Schwab’s securities portfolio, the wealth administration and brokerage big managed to cut back the quantity of excellent supplemental funding. By the top of the third quarter in 2023, the FHLB stability stood at $31.8 billion, reflecting a $9.2 billion lower from the top of the second quarter. CDs, nevertheless, nonetheless remained at ranges according to Q2, at roughly $44.5 billion. Thus, general, Schwab’s web curiosity earnings remained pressured, with 3Q NIM being reported at only one.94%. Based on administration steering, it’s going to possible take two years of gradual the “non permanent borrowing” redemption, and resumption of securities portfolio reinvestments, till the corporate’s NIM strengthens again to (hopefully) 3.00% by the top of 2025.

Residual Earnings Mannequin

With stability sheet changes slowing, and administration highlighting a path in the direction of 2025 NIM projections, I really feel assured valuing Schwab inventory primarily based on a residual earnings mannequin. As per the CFA Institute:

Conceptually, residual earnings is web earnings much less a cost (deduction) for frequent shareholders’ alternative value in producing web earnings. It’s the residual or remaining earnings after contemplating the prices of all of an organization’s capital.

With regard to my Charles Schwab inventory valuation mannequin, I make the next assumptions:

- To forecast EPS, I anchor on the consensus analyst forecast as out there on the Bloomberg Terminal ‘until 2025. For my part, any estimate past 2025 is simply too speculative to incorporate in a valuation framework. However for 2-3 years, the analyst consensus is normally fairly exact.

- To estimate the capital cost, I anchor on Schwab’s value of fairness at 8.75%.

- For the terminal progress price after 2025, I apply 2.25%, which I consider is an inexpensive estimate post-2025 (roughly according to U.S. nominal GDP progress).

- Buyers with totally different assumptions relating to Schwab’s value of capital and terminal progress could take reference from the sensitivity desk enclosed.

Given the above assumptions, I calculate a base-case goal value for Schwab inventory of about $42.39/share, suggesting 15% draw back.

Firm Financials; Writer’s EPS Estimates; Writer’s Calculation

My base case projection for SCHW’s goal value implies draw back. Nevertheless, it’s essential for traders to judge the danger and reward ratio of investing in an organization primarily based on a ‘state of affairs’ view. To evaluate totally different situations primarily based on numerous assumptions, I’ve created a sensitivity desk that analyzes SCHW’s value of fairness and terminal progress price. See under.

Firm Financials; Writer’s EPS Estimates; Writer’s Calculation

Conclusion

In my prior evaluation of Charles Schwab, I raised issues in regards to the administration of the period in its securities bond portfolio and the potential earnings stress ensuing from refinancing wants at increased rates of interest and shopper money sorting exercise. After reviewing Schwab’s Q3 outcomes, my earlier thesis seems to be on monitor, with the corporate reporting a 44% YoY contraction in EPS. The earnings stress continues to be primarily anchored on headwinds from financing, that are anticipated to stay fairly sticky, solely step by step fading via 2025. With Q3 insights and NIM visibility, my residual earnings mannequin suggests a base-case goal value for Schwab inventory of about $42.39 per share, indicating roughly 15% draw back. As a consequence, I proceed advising to keep away from SCHW inventory.