: Core Strengths And Operational Effectivity Allow Margin Growth")

SweetBunFactory/iStock by way of Getty Photos

Cardinal Well being (NYSE:CAH) is a US-based multinational healthcare providers firm, specializing within the manufacturing and distribution of pharmaceutical and medical merchandise.

Cardinal Well being Q3 FY23 Presentation

The corporate positions itself as an integral facet of the US medical provide chain, emphasizing its end-to-end function from manufacturing to the distribution of its merchandise.

Introduction

To optimize development and fulfill the wants of all stakeholders, Cardinal Well being has recognized three strategic priorities; scale development might be pushed by Cardinal’s ‘Medical Enchancment Plan’ initiatives, which goal to leverage the agency’s market place and healthcare megatrends; deal with the core enterprise of prescribed drugs, enhancing client experiences and supporting development throughout specialty segments; and returning worth to shareholders, by a capital allocation mixture of natural development, dividends, and opportunistic buybacks.

Cardinal Well being Q3 FY23 Presentation

Such methods have enabled across-the-board development within the firm’s Q3’23, attaining 13% income development and 6% gross margin development YoY.

Cardinal Well being Q3 FY23 Presentation

Valuation & Financials

Normal Overview

Within the TTM interval, Cardinal Well being- up 50.95%- has seen considerably larger development than the healthcare trade (IXHC)- up 12.81%- and the broad market, represented by the S&P 500 (SPY)- up 5.51% for the 12 months.

Cardinal Well being (Darkish Blue) vs Business and Market (TradingView)

Such worth motion validates Cardinal’s lean organizational technique, which has decreased the corporate’s sensitivity to macro headwinds (i.e., built-in healthcare companies equivalent to UnitedHealth (UNH) are uncovered to medical health insurance, PBM, pharma, and so forth. dangers) and adapt to basic circumstances.

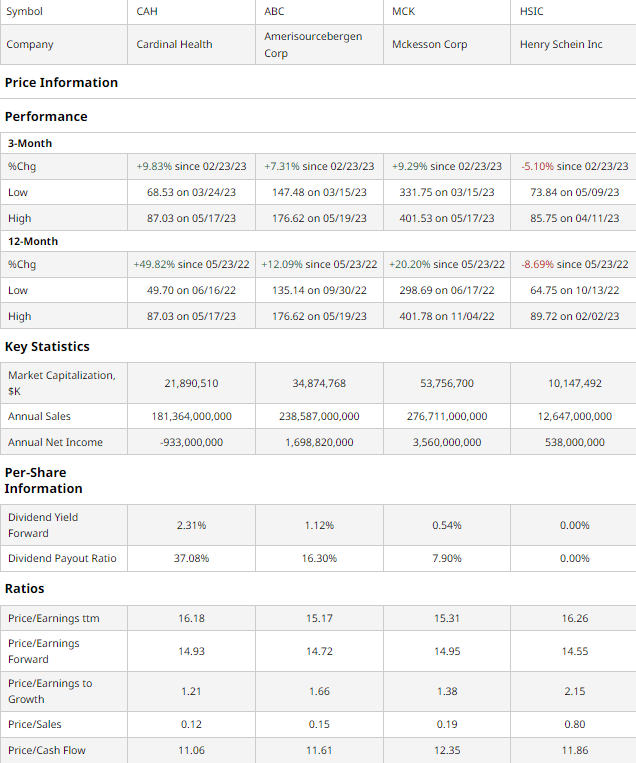

Comparable Corporations

The size benefit needed for efficient competitiveness within the pharmaceutical and medical distribution market helps a extremely concentrated market, with a number of large-cap and specialty mid-cap companies. Amongst these are AmerisourceBergen (ABC) a pacesetter in leveraging ongoing healthcare megatrends, however a lot much less versatile than Cardinal, McKesson (MCK), the most important prescribed drugs distributor, and Henry Schein (HSIC) which carries a big portion of web gross sales in its dental merchandise section.

barchart.com

As illustrated above, Cardinal Well being sustains the perfect quarterly and yearly worth motion, with respective worth will increase of 9.83% and 49.82%. This development comes at the side of the perfect dividend amongst friends, additional demonstrating Cardinal’s dedication to capital return to shareholders.

The agency’s undervaluation is additional emphasised on a multiples foundation; whereas Cardinal is near-median in trailing and ahead P/E ratios, the corporate sustains the bottom PEG, P/S, and P/CF ratios.

On the flip aspect, Cardinal does keep excessive debt ranges owing to historic M&A actions and historic operational deficiencies. The excellent news, nevertheless, is that Cardinal has low ranges of present web debt and has demonstrated an outsized skill to transform its EBIT to money circulate successfully. Furthermore, lots of the firm’s historic misgivings have been rectified, with Cardinal aiming for a leaner enterprise mannequin; for example, in August 2021, Cardinal divested from its cardiology and endovascular machine manufacturing division, promoting it to Hellman & Friedman for $1bn, because the enterprise was non-material to the general success of the corporate.

Valuation

In line with my discounted money circulate mannequin, at its base case, the honest worth of Cardinal is $124.32, that means that the inventory is at the moment undervalued by 31% at its present worth of $85.37.

My mannequin assumes a reduction price of 11%, owing to Cardinal’s debt-laden cap construction and total recessionary impacts, although the inelastic nature of prescribed drugs and medical gadgets reduces any detrimental demand pressures. Moreover, I undertaking gross sales development of ~5% though common income development prior to now 5 years has been ~8.30%, incorporating enterprise threat and inflationary pressures including to the operational bills of the agency.

AlphaSpread

AlphaSpread’s multiples-based relative valuation instrument greater than validates my thesis of undervaluation, calculating Cardinal’s base case honest worth to be $203.38, a 58% undervaluation from its present worth.

Nevertheless, AlphaSpread’s incapacity to include Cardinal’s excessive debt ranges causes a skew upward in valuation.

Subsequently, utilizing a weighted common with extra weight given to my DCF, the honest worth of Cardinal is $133.58, with the corporate at the moment undervalued by 36%.

Simplified Enterprise Mannequin Allows Adaptation to Secular Money Move Streams

At giant, the healthcare trade presents traders with a great proposition, being a recession-resilient trade and development pushed by healthcare megatrends. For instance, the mix of an ageing US inhabitants and accelerated persistent illness diagnoses assist scale enlargement, whereas improvements in specialty medicine, site-of-care shifts, and know-how developments create inherent alternative.

Cardinal Well being Q3 FY23 Presentation

As exemplified above, Cardinal’s nimble group allows them to leverage mentioned development tendencies; the agency is a pacesetter in nuclear prescribed drugs and radio-pharmacies, has expanded its vertical footprint to assist homecare, and continues to spend money on technological enchancment, remaining a key facet of the US pharmaceutical and medical provide chain.

On a extra particular degree, Cardinal has outlined its ‘Medical Enchancment Plan’, delineating its investments in short-term and long-term development targets. Within the quick time period, the corporate plans to speculate ~$300mn in inflation mitigation and provide chain resilience whereas, in the long run, >$75mn, $60mn, and $50mn are being allotted in direction of optimizing and increasing the Cardinal Well being Model portfolio, accelerating its homecare options, and value optimization respectively.

Cardinal Well being Q3 FY23 Presentation

Mixed with a shareholder-oriented capital deployment strategy- with a premium on debt discount (i.e. recording a 67.11% decline in web debt from 2021-22, from $3.31bn to $1.09bn) after which dividend payouts and opportunistic share repurchases (with a $1.2bn remaining repurchase authorization)- Cardinal’s pharma and medical methods have enabled long-term double-digit EPS development and dividend yield development.

Cardinal Well being Q3 FY23 Presentation

Wall Road Consensus

Analysts largely echo my constructive view on the inventory, projecting a median 1Y worth enhance of two.23% to $97.00.

TradingView

Nevertheless, on the minimal estimated worth motion, analysts forecast a worth decline of -11.19%, to a worth of $76.00. I imagine these projections are based mostly on apprehensions about Cardinal’s debt ranges and incapacity to go down inflationary prices.

Dangers & Challenges

Sustained Regulatory Complexity

The healthcare trade intrinsically stays a extremely regulated and bureaucratic market, with excessive ranges of public scrutiny. Elevated complexities or worth restrictions can inhibit Cardinal’s skill to adequately adapt to macro circumstances and dampen profitability and free money circulate technology capabilities.

Aggressive Depth Could Hamper Profitability

Though Cardinal solely straight competes with a handful of prescribed drugs distributors, they face the backwards integrations of healthcare insurers and teams such because the UnitedHealth Group and CVS (CVS), thus furthering aggressive depth and repeatedly reinforcing downward strain on pricing and thus profitability.

Continued Inflationary Stress

Primarily working as a pharmacy and medical machine distributor, Cardinal moreover manufactures a variety of merchandise; as such, Cardinal has been aware of the consequences of inflation, resulting in materials reductions in profitability; the aforementioned enhance in sustained aggressive depth solely reduces Cardinal’s skill to adapt to larger enter prices, thus rising operational bills and lowering margins.

Conclusion

Within the quick time period, I anticipate that Cardinal will proceed to revert from the monetary lows of the previous few years and pay down its web debt.

In the long run, I undertaking that Cardinal’s lean enterprise mannequin will allow adaptability and place the corporate to maximise long-term development.