Brandon Bell/Getty Photographs Information

Shares of Camden Property Belief (NYSE:CPT) have been a cloth underperformer over the previous yr as greater charges have weighed on actual property valuations. On prime of this, a surge of provide has negatively impacted the condo sector, pushing down rents. Final September, I rated CPT a purchase, arguing shares had 10-15% upside. Since that suggestion, shares have returned over 4%, although this has materially lagged the broader market’s 18% acquire. I proceed to focus on an increase towards $105 and would stay lengthy the inventory.

Searching for Alpha

Within the firm’s fourth quarter, reported on February 1, Camden matched consensus with $1.73 of funds from operations (FFO). In This fall, property revenues rose by $12 million to $388 million. Offsetting this, property bills rose by $9 million or over 7% whereas greater charges elevated curiosity expense by $3 million. For the total yr, core FFO was $6.82, up 4.6% from 2022.

The core theme in outcomes has been ongoing expense progress as inflation passes by way of and decelerating income progress. Particularly, identical property rents rose by 2.8% from final yr in This fall; this lags the total yr rental progress fee of 6.6%. Sequentially, rents rose by 0.1%, and it might dip detrimental in Q1. Equally, This fall occupancy of 94.9% was down from 95.5% in Q3, and it’s anticipated to be flat in Q1 2024. Partially offsetting this misplaced momentum, unhealthy debt declined 40bp in This fall to simply over 1%.

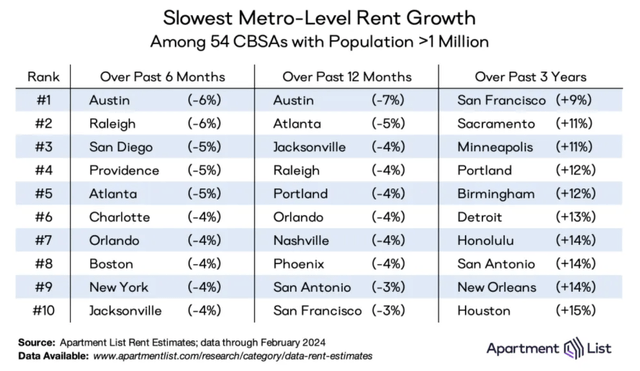

As you possibly can see beneath, new lease charges at the moment are decidedly detrimental whereas renewal charges are solely modestly constructive, pushing blended rents decrease. In February, the corporate boosted advertising and incentives to occupy items that had been vacant for over 30 days forward of the spring season. Basically, CPT is buying and selling decrease charges for elevated emptiness in the meanwhile. CPT can also be seeing variance throughout markets. Particularly, new provide has brought on weak spot in Austin the place concessions have reached 3 months versus a 1-1.5 month norm.

Camden Property

With advertising efforts weighing on February’s lease charges, this month could also be portray a very harsh image of the enterprise. General, for the total yr, Camden is concentrating on core FFO of $6.59-$6.89. CPT expects same-property income progress of 0.5-2.5% with California outperforming whereas markets with elevated new development like Austin and Orlando lag. Bills are slated to rise about 4.5%, leaving web working revenue flat. This can be a bit beneath the $7 I used to be concentrating on in September, as provide headwinds have confirmed stronger.

Basically, income progress can be sluggish, and margins are coming below strain. Working bills are feeling a lagged impression from inflation. Insurance coverage accounts for 7.5% of bills and is forecast to rise by a troublesome 18% in 2024. Insurance coverage contracts typically run 12 months, and as inflation exceeded expectations, many insurers had been saddled with worse than anticipated losses. They’ve subsequently been elevating charges to recoup these prices. I anticipate 2024 to be the worst of the insurance coverage will increase, barring a very unhealthy disaster season.

Excluding insurance coverage, working expense progress is a extra reasonable 3.4%, although this nonetheless outpaces lease progress. On the constructive aspect, property taxes will rise by simply 3%, aided by Texas laws, leaving progress right here at 2.2%. TX is 40% of its tax base, and this slower progress fee ought to assist to sluggish longer-term expense progress. Barring an extra lease decline past mid-2024, this yr ought to signify a nadir for working margins.

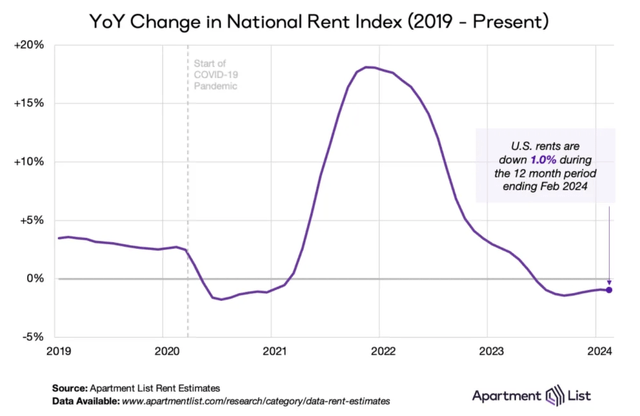

The problem Camden faces is a weaker rental setting. 2021 and 2022 had been banner years for lease progress that continued into early 2023 as post-pandemic migration and stimulus brought on a surge in demand. In line with Condominium Checklist, rents had been rising at a double-digit tempo however have fallen about 1% over the previous yr.

ApartmentList

As Camden laps favorable comps and re-ups leases, income progress will proceed to sluggish. One constructive is that turnover has slowed from 37% to 34%, and renewal charges are typically higher than new lease charges as some occupied flats haven’t had rents rise as rapidly because the market, permitting CPT to proceed growing rents on present tenants. Elevated mortgage charges are additionally seemingly holding tenants as renters with house affordability troublesome. Camden’s common renter is 31 years previous and upon move-in has a mean revenue of $122k and rent-to-income ratio of 19%, which is comparatively low and sure cheaper than shopping for a house and taking out a mortgage.

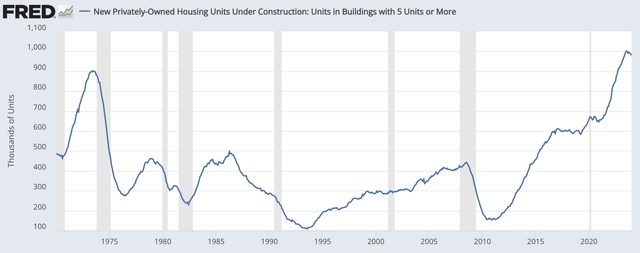

The problem the sector faces is that the surge in rents in 2021-2022 brought on builders to considerably enhance development. Whereas it has seemingly peaked, the variety of flats below development hit a document. A good portion of those items are being accomplished in 2024, which has brought on short-term extra provide in markets like Austin and Orlando, pushing down rents. As a result of new begins have slowed given decrease rents and better charges, provide ought to peak in 2024. Administration sees 400,000 items of web provide to be absorbed in 2024, which ought to fall to the low 200,000s in 2025. About half of nationwide provide will hit its markets.

St. Louis Federal Reserve

Certainly, after main within the rental bull market, Solar Belt markets at the moment are the clear laggards in latest months. They’ve grow to be victims of their very own success with out outsized inhabitants and lease progress resulting in essentially the most significant enhance in development. Locations like Northern California that noticed weak rents post-COVID have held up higher the previous six months as there was little provide. Basically, there was some imply reversion as markets with essentially the most demand have confronted essentially the most provide.

ApartmentList

Camden is basically positioned in progress Solar Belt markets, which is why it faces a lot of this provide strain. Leads to 2024 although can be helped by its materials California presence, which is predicted to generate income progress north of two.5%, given favorable provide dynamics. As a reminder, CPT’s portfolio is majority class B and majority suburban with 58,634 items at a mean lease of $1,994. Aided by CA, CPT expects 1.4% market lease progress vs its 3% long-term assumption.

Camden Property

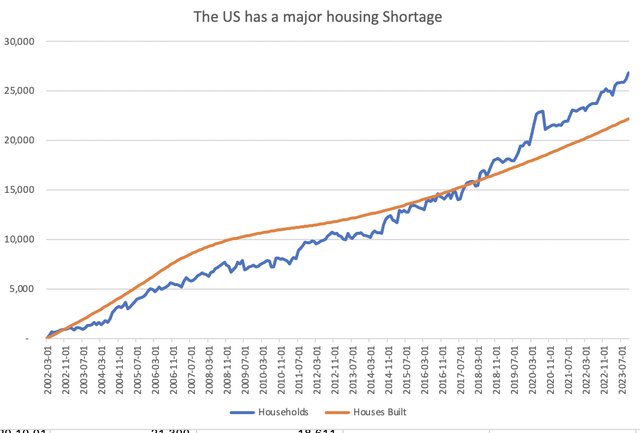

Now whereas provide is clearly weighing on leads to 2024, I agree with administration’s 3% long-term rental goal and do consider 2024 weak spot can be transitory. Whereas new provide can hit rents, I do anticipate this provide to get absorbed as a result of the US market is basically brief housing items as a result of lack of development within the 2010s. We nonetheless have a couple of 4 million unit scarcity, and this could present landlords with stable pricing energy over time. Moreover, elevated mortgage charges are more likely to hold renting a sexy worth proposition vs proudly owning.

my very own calculations, Census Bureau

Whereas the Solar Belt has essentially the most provide, within the medium time period, I consider you need actual property publicity to markets individuals are shifting to, as that demand will drive rental features over time. CPT can also be managing this downturn conservatively, and its latest prioritization of elevated occupancy forward of provide hitting the market in Q2/Q3 ought to defend outcomes. CPT can also be being conservative in its personal enlargement. It has 1,500 items in improvement at a complete price of $546 million with simply $138 million remaining on these initiatives. In 2024, administration targets $250 million of acquisitions and $150 million of improvement begins towards $365 million of gross sales for simply $35 million of web enlargement.

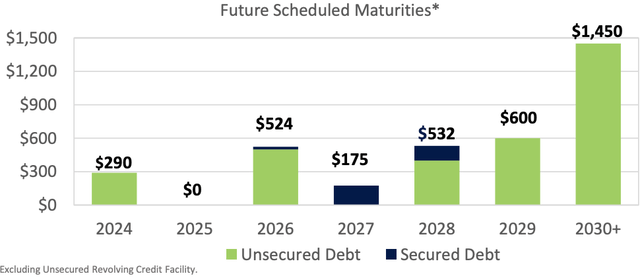

This cautious enlargement program signifies that CPT won’t be including extra provide at a time of weak spot. It additionally has a well-laddered debt profile that limits its publicity to greater charges. Aided by this power, alongside This fall outcomes, CPT elevated its dividend by 3% to $1.03. Its dividend protection can also be a strong ~1.6-1.65x, which may assist ongoing annual will increase even in a subdued rental market.

Camden Property

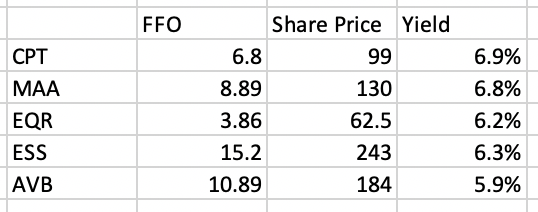

Amongst friends, CPT trades on the cheaper finish by way of FFO yield. In the end, I consider it deserves an analogous valuation to Mid-America (MAA), which has an analogous geographic combine besides MAA lacks a big CA presence. Nevertheless, these two Solar Belt REITs commerce a reduction to legacy gamers. I consider this creates a chance as a result of wanting previous 2024, Solar Belt demographic developments are favorable. With traders centered on 2024 provide, there is a chance to purchase greater progress companies at a less expensive valuation.

Searching for Alpha, my calculations

With a 4+% dividend yield that’s properly lined the power to speed up dividend progress previous 5% as we cross this trough yr, I view CPT as providing a sexy mixture of revenue and progress. At a peer median a number of, shares might attain $108. I don’t anticipate them to get fairly that top given some “Solar Belt provide danger premium.” As such, I’m concentrating on $105, for an ~11% whole return together with dividends, which I view as enticing given favorable long-term rental developments. Downturns can present good alternatives to purchase sturdy companies, and that’s the state of affairs as we speak with Camden.

{kind=link}