Market Recap

The worth-growth divide for the reason that begin of the month continued to play out final Friday, as market contributors pare their publicity in US huge tech and semiconductors, whereas worth sectors held agency with a notable pull-ahead within the power sector (+1.6%).

Some unease had been triggered by the upside shock in US producer costs, however for now, it is going to nonetheless should take far more to persuade markets of a September Fed price hike. Present price expectations from the Fed feds futures pricing remained agency that the Fed’s tightening cycle has already reached its finish, with potential price cuts in Could subsequent yr. To finish final week, US Treasury yields largely resumed their transfer increased, with the 10-year yields bouncing off its 4% stage currently to aim a transfer to a brand new year-to-date excessive.

The day forward shall be comparatively quiet on the financial calendar entrance, which might drive a extra subdued tone to begin the week, however focus shall be turned to Japan’s 2Q GDP launch tomorrow, together with the RBA minutes and a sequence of financial knowledge out of China to drive extra market motion.

One to look at could also be Brent crude costs, which proceed to hover beneath its US$88.00 stage of resistance. A bearish crossover on MACD might level to some near-term exhaustion, however a pull-ahead of its weekly RSI again above the 50 stage currently might recommend patrons taking better management. Any reclaim of the US$88.00 stage might probably pave the best way to retest its November 2022 excessive on the US$98.00 stage.

Supply: IG charts

Asia Open

Asian shares look set for a weak open, with Nikkei -0.33%, ASX -0.38% and KOSPI -0.62% on the time of writing. China’s financial woes resumed with new financial institution loans for July tumbling to finish final week (CNY345.9 billion versus CNY800 billion forecast), whereas a droop in overseas direct funding (April-June quarter) to its file low prompted China authorities to react with a listing of pointers to draw extra overseas investments. That mentioned, having been accustomed to the sequence of coverage responses from authorities to date, sentiments appear to be on the stage the place they are going to need to see supportive insurance policies translating into precise outcomes.

Into the brand new week, contemporary updates on China’s retail gross sales, industrial manufacturing and glued asset funding figures shall be on watch tomorrow. An uneven restoration within the numbers is anticipated to be the story, with industrial manufacturing to stay unchanged whereas retail gross sales are anticipated to rise to 4.7% year-on-year from earlier 3.1%.

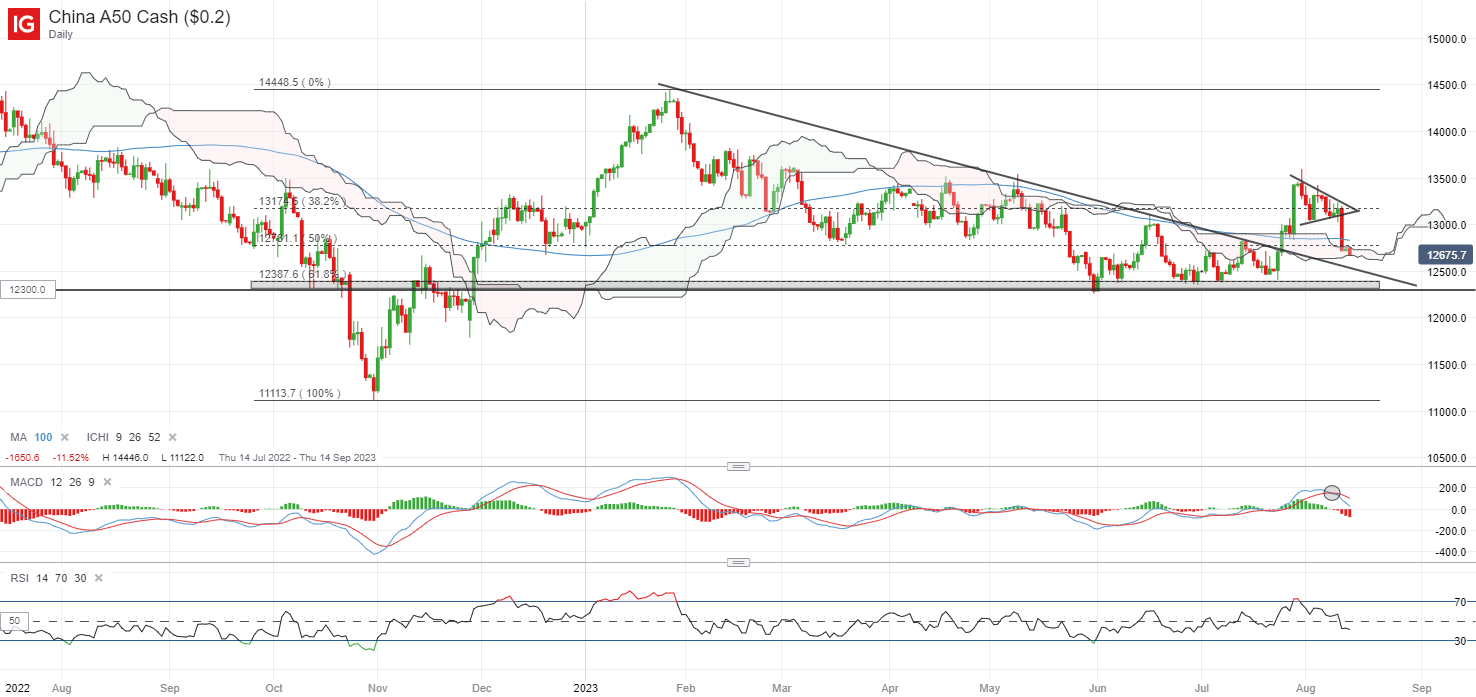

For the China A50 index, a latest bullish pennant formation on the day by day chart failed to search out an upward break, with sellers leaping in final week to place the index on a three-week low. With that, the 13,200 stage shall be a key resistance stage to beat forward, whereas additional draw back might go away the 12,300-12,500 vary on watch, the place a earlier downward trendline stands alongside its year-to-date backside.

Supply: IG charts

On the watchlist: USD/JPY again to retest its year-to-date excessive

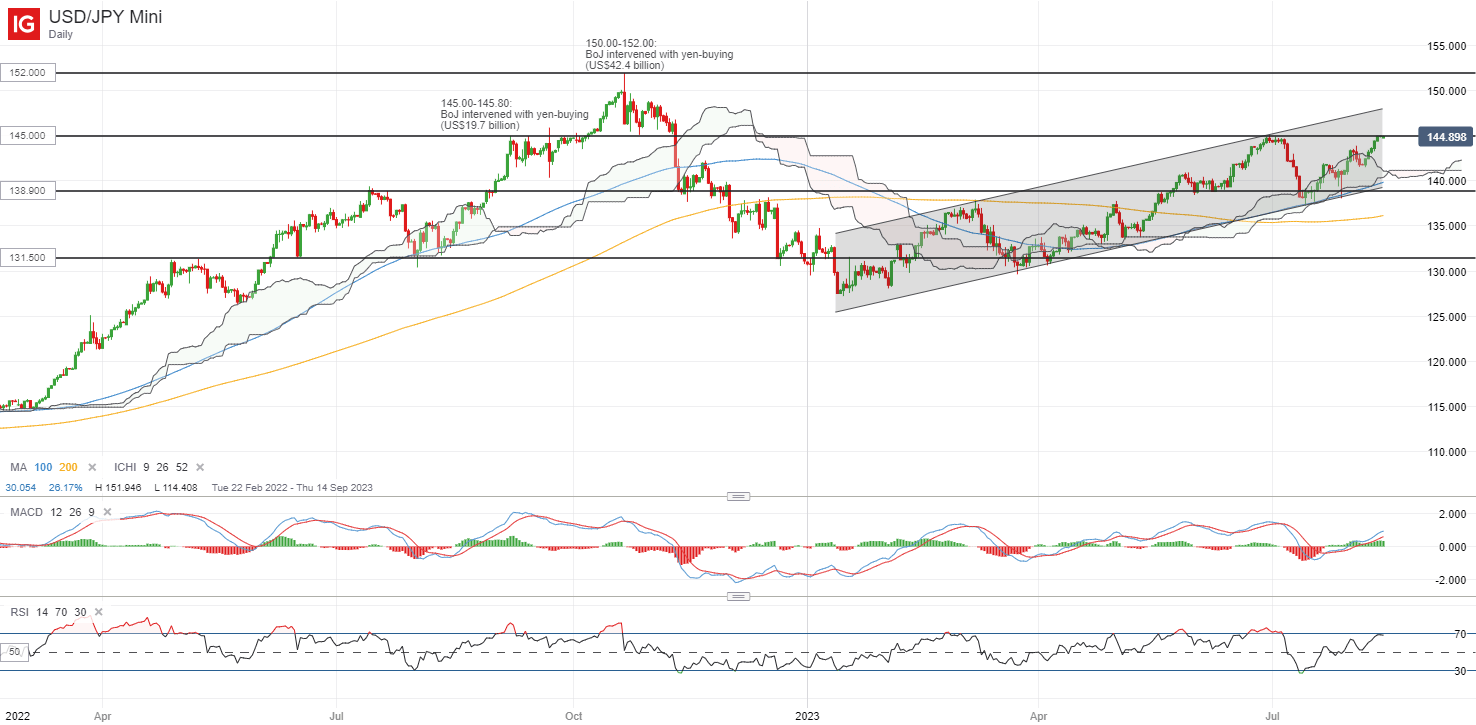

Market contributors have been unfazed by the extra versatile coverage method from the Financial institution of Japan (BoJ) to date, with a continued rise within the US-Japan 10-year bond yield unfold lifting the USD/JPY again to retest its year-to-date excessive on the 145.00 stage. Earlier retest of the extent in June this yr was met with some jawboning of yen intervention by Japanese authorities, however merchants could also be searching for for any concrete follow-through this time spherical.

For now, the general upward bias within the pair stays intact, with the pair buying and selling inside an ascending channel sample for the reason that begin of the yr and its weekly RSI holding above the 50 stage currently. On any draw back, the 138.90 stage shall be on watch as near-term help from its 100-day MA, in coincidence with the decrease fringe of its Ichimoku cloud on the day by day chart.

Supply: IG charts

Friday: DJIA +0.30%; S&P 500 -0.11%; Nasdaq -0.56%, DAX -1.03%, FTSE -1.24%.

{kind=link}