")

MarsBars

Planning for retirement generally is a daunting activity, particularly if one is invested in low-yielding index funds. For some individuals, this creates the necessity to dip into one’s principal, particularly in terms of required minimal distributions in an IRA account.

That’s why having allocation to sectors akin to REITs, MLPs, and BDCs which might be designed for top yield could also be a great choice, with the latter group really benefitting from the upper rate of interest atmosphere that we discover ourselves in now.

This brings me to Blackstone Secured Lending Fund (NYSE:BXSL), which flies below the radar within the BDC sector in comparison with extra standard names like Ares Capital (ARCC) or Essential Avenue Capital (MAIN). I final coated BXSL right here in January, noting the standard of its portfolio and its low cost to NAV. On this article, I present an replace on the enterprise and make an up to date advice.

Why BXSL?

Blackstone Secured Lending Fund is externally managed by Blackstone, which is without doubt one of the greatest asset managers at this time and has a 17-year monitor report in North America direct lending and BDCs.

It additionally has loads of sources and experience to assist BXSL, with 503 credit score professionals throughout 17 international workplaces. Furthermore, BX prices a fairly low administration payment of 0.75% for the preliminary 2 years post-IPO, and 1% thereafter, evaluating favorably to the 1.5% base administration payment that almost all BDCs, together with Ares Capital, prices.

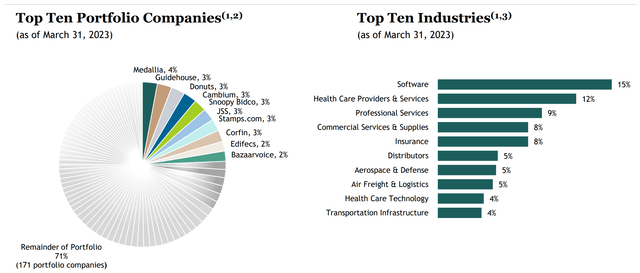

At current, BXSL has a large funding portfolio of $9.6 billion at honest worth consisting of 181 portfolio firms, with a low common loan-to-value ratio of 45%, implying vital fairness buffer. BXSL’s debt positions are additionally properly protected with 98% of them being first lien senior secured debt. As proven beneath, BXSL invests primarily in know-how and defensive industries akin to healthcare, skilled companies, and insurance coverage, with no issuer accounting for greater than 4% of its portfolio.

Investor Presentation

In the meantime, BXSL is benefitting from greater rates of interest with 99.9% of its debt portfolio being floating fee. This was mirrored by web funding revenue rising by 3% quarter-on-quarter to $0.93 per share within the first quarter, pushed by the typical yield on debt investments rising by 70 foundation factors to 11.4%.

The aforementioned NII/share additionally gave administration loads of buffer room to boost the quarterly dividend by 10%, to $0.77 per share, leading to a nonetheless protected 83% payout ratio and an 11.4% dividend yield primarily based on the present worth of $27.04.

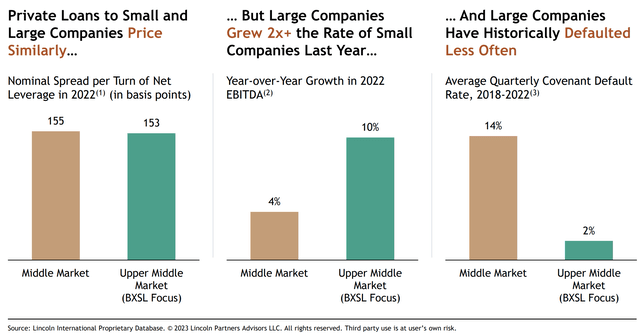

Additionally encouraging, BXSL’s NAV per share rose by 0.7% of a sequential foundation to $26.10, reflecting portfolio stability, and non-accruals stay low, at simply 0.07% of portfolio honest worth. Administration sees worth in lending to the higher center market, which is the place BXSL’s candy spot is. As proven beneath, the higher center market as demonstrated a decrease default fee lately whereas exhibiting greater development final 12 months.

Investor Presentation

Wanting forward, BXSL maintains loads of funding capability, with $1.2 billion value of liquidity comprising of money and undrawn capability on credit score strains. It’s additionally modestly leveraged with a debt to fairness ratio of 1.31x, which is down from 1.34x from the top of 2022.

BXSL can also be positioned to profit from greater rates of interest, with the Fed Chairman not too long ago saying the intent for extra fee hikes this 12 months regardless of the June pause to get inflation again right down to 2%. That’s as a result of greater charges imply the next funding unfold for BXSL, with 58% of its debt being mounted fee, unsecured debt with a low weighted common rate of interest of two.97%, sitting properly below the aforementioned 11.4% yield on debt investments that’s poised to go greater.

Turning to valuation, BXSL doesn’t look like overpriced on the present worth of $27.03 with a worth to NAV ratio of 1.035x. Whereas some buyers choose to purchase BDCs when they’re buying and selling at a reduction to NAV, it’s much better to purchase a top quality BDC that has the aptitude of buying and selling at a premium to NAV.

This indicators investor confidence and offers the BDC the flexibility to boost fairness in an accretive method. Contemplating the size of BXSL’s platform, Blackstone’s backing, and the low administration payment, I don’t discover it to be unreasonable for BXSL to commerce at a worth to NAV goal of 1.1x.

Investor Takeaway

Blackstone Secured Lending Fund continues to show itself as a top quality BDC, with a well-diversified portfolio comprised principally of first lien senior secured debt investments. Furthermore, its portfolio has low mortgage to worth and a really low non-accrual fee. As rates of interest are anticipated to rise extra this 12 months, BXSL stands to profit from greater yields on its debt investments and the next funding unfold. Lastly, whereas BXSL is not low cost, it is not costly both contemplating its well-covered dividend yield and fee-friendly construction, making it a strong alternative for revenue buyers.