")

Marat Musabirov

The Blackstone Lengthy-Brief Credit score Earnings Fund (NYSE:BGX) is an uncommon closed-end fund that income-focused traders can buy to be able to pursue their objectives. The fund definitely manages to do fairly effectively at offering its traders with a excessive degree of revenue, as its 10.26% yield compares pretty effectively with most different debt-focused closed-end funds available on the market. The fund has only a few direct friends, no less than publicly traded ones, as this is likely one of the few closed-end funds that claims to have the flexibility to make use of brief positions. Nonetheless, right here is how its yield compares to that of some credit score funds provided by different different asset managers:

|

Fund Title |

Present Yield |

|

Blackstone Lengthy-Brief Credit score Earnings Fund |

10.26% |

|

Ares Dynamic Credit score Allocation Fund (ARDC) |

9.99% |

|

Apollo Senior Floating Charge Earnings Fund (AFT) |

11.34% |

|

Apollo Tactical Earnings Fund (AIF) |

10.97% |

|

KKR Earnings Alternatives Fund (KIO) |

11.04% |

As we will see, the Blackstone Lengthy-Brief Credit score Earnings Fund compares moderately effectively to those different funds when it comes to yield, however it’s not as excessive because the pure floating-rate fund. This isn’t precisely stunning as a result of the inverted yield curve right this moment has resulted in long-dated bonds having considerably decrease yields than leveraged loans or different floating-rate securities. The Blackstone Lengthy-Brief Credit score Earnings Fund additionally might not use the identical technique as the opposite funds listed as a result of it’s the solely one among this group that has the acknowledged potential to take brief positions in securities that the fund’s administration expects will decline in worth.

As common readers might keep in mind, we beforehand mentioned the Blackstone Lengthy-Stone Credit score Earnings Fund in early December. On the time, the fund was closely weighted to floating-rate loans and comparable short-term securities in distinction to market expectations that rates of interest would quickly decline over the course of 2024. On the time, I steered that this positioning was fairly strong if the market proved to be incorrect with respect to rates of interest. Over the previous three months, the market has begun to understand that it most likely was flawed concerning the pace at which the Federal Reserve will scale back rates of interest and this fund naturally managed to carry out fairly effectively. As we will see right here, shares of the Blackstone Lengthy-Brief Credit score Earnings Fund have appreciated by 6.97% because the date that my prior article on the fund was printed. This was considerably higher than the 0.29% acquire of the Bloomberg U.S. Mixture Bond Index:

Searching for Alpha

That is nearly definitely going to attraction to any investor, not solely those that are centered on maximizing their revenue from the property of their portfolios. We will additionally see that the fund’s shares actually began to take off in January and February when it turned extra obvious that my thesis concerning the unlikelihood of near-term rate of interest cuts could possibly be appropriate. Thus, the fund’s efficiency appears to validate the thesis that was introduced beforehand.

Nonetheless, a easy take a look at the fund’s share worth efficiency solely tells a part of the story. It’s because the Blackstone Lengthy-Brief Credit score Earnings Fund is a closed-end fund. One of many defining traits of closed-end funds is that they usually pay out most or all of their funding income to their traders by way of their distributions. That is completely different from index exchange-traded funds that are likely to rely on share worth appreciation to ship their beneficial properties to shareholders. That is the rationale why closed-end funds are likely to have increased yields than most different property out there. The funds that the fund makes to its traders characterize an actual funding return and as such the fund’s traders usually do so much higher than the share worth efficiency alone would point out. This additionally signifies that we have to take the fund’s distributions under consideration in any evaluation of its outcomes. Once we try this, we see that traders within the Blackstone Lengthy-Brief Credit score Earnings Fund have gained 9.83% because the December 1, 2023, publication date of my earlier article on this fund. That’s considerably above the 1.17% acquire of the Bloomberg U.S. Mixture Bond Index:

Searching for Alpha

The truth that the fund managed to ship this degree of complete return over a interval of simply over three months is definitely going to be interesting to any potential investor. Nonetheless, previous efficiency is not any assure of future outcomes, and it’s all the time essential that we take a look at the fund as it’s right this moment to be able to get an concept of the way it might carry out sooner or later.

As simply over three months have handed since we beforehand mentioned this fund, it will be fairly logical to imagine that a couple of issues have modified. Specifically, the fund launched its full-year 2023 monetary statements that can give us an excellent concept of how effectively it managed to deal with the considerably turbulent credit score markets that existed within the second half of 2023.

About The Fund

In line with the fund’s web site, the Blackstone Lengthy-Brief Credit score Earnings Fund has the first goal of offering its traders with a really excessive degree of present revenue. This isn’t notably stunning contemplating that it is a fund that invests in debt securities. The web site explains the fund’s technique in nice element:

Blackstone Lengthy Brief Credit score Earnings Fund is a closed-end fund that trades on the New York Inventory Change below the image “BGX”. BGX’s main funding goal is to offer present revenue, with a secondary goal of capital appreciation. BGX will take lengthy positions in investments which we consider supply the potential for enticing returns below numerous financial and rate of interest environments. BGX may take brief positions in investments which we consider will under-perform as a result of a larger sensitivity to earnings development of the issuer, default danger or the overall degree and course of rates of interest. BGX should maintain at least 70% of its Managed Property in first- and second-lien floating charge loans (“Secured Loans”), however may spend money on unsecured loans and excessive yield bonds.

The truth that the Blackstone Lengthy-Brief Credit score Earnings Fund invests solely in debt securities makes present revenue essentially the most logical alternative for an funding goal. In any case, credit score securities are by their very nature revenue securities. As I defined in my earlier article on this fund:

As I’ve identified quite a few instances previously, debt securities by their very nature haven’t any web capital beneficial properties over their lifetimes. These securities are each issued and redeemed at face worth, with the one funding beneficial properties over their lifetimes being the common funds that they make to their traders. These common funds function revenue, so it is sensible {that a} fund like this may have present revenue as its main goal in comparison with one thing else.

The truth that credit score securities ship no web capital beneficial properties over their lifetimes doesn’t preclude the potential of incomes capital beneficial properties from these securities if the fund is prepared to commerce them. In any case, bond costs do transfer inversely to rates of interest, so it’s potential to earn some income by shopping for bonds after which promoting them when rates of interest go down. This fund had an 88% annual turnover for the complete yr 2023 interval so that means that it’s doing quite a lot of buying and selling of property. That’s, in spite of everything, the next annual turnover than most debt funds possess. Right here is how the Blackstone Lengthy-Brief Credit score Earnings Fund compares to its friends on this respect:

|

Fund |

Annual Turnover |

|

Blackstone Lengthy-Brief Credit score Earnings Fund |

88.00% |

|

Ares Dynamic Credit score Allocation Fund |

48.34% |

|

Apollo Senior Floating Charge Earnings Fund |

47.20% |

|

Apollo Tactical Earnings Fund |

48.40% |

|

KKR Earnings Alternatives Fund |

58.00% |

Clearly, the Blackstone Lengthy-Brief Credit score Earnings Fund is making an attempt to use the fluctuations in asset costs that accompany rate of interest adjustments to a larger extent than its peer funds. This might definitely counsel that the fund is operating up increased bills than its friends, however admittedly bills should not essentially an important factor for traders.

That assertion about bills could also be complicated to some readers, as I regularly see feedback suggesting that top bills are all the time an issue. Nonetheless, the one actual downside with a fund’s bills is that they create a drag on its efficiency. On the finish of the day, a high-expense fund that manages to ship excessive efficiency continues to be significantly better than a low-expense fund that delivers worse efficiency. All that basically issues is the full return that in the end flows by means of to the traders. As we will see right here, the Blackstone Lengthy-Brief Credit score Earnings Fund has managed to considerably outperform the Bloomberg U.S. Mixture Bond Index and the Bloomberg U.S. Floating Charge Word < 5 Yrs. Index (FLOT) by quite a bit:

Searching for Alpha

As we will see, traders within the Blackstone Lengthy-Brief Credit score Earnings Fund have benefited from a 25.20% complete return over the previous 5 years, considerably beating each of the low-cost index funds. In actual fact, it managed to beat each indices by greater than 1,000 foundation factors over the interval. The fund’s charges clearly didn’t harm its efficiency over the interval relative to the index, though its leverage did trigger it to be rather more risky over time.

Sadly, this fund’s historic efficiency has not in contrast too effectively to its friends. This chart reveals the Blackstone Lengthy-Brief Credit score Earnings Fund’s complete returns in comparison with the above funds provided by competing different asset managers over the identical five-year interval:

Searching for Alpha

We will clearly see that the Blackstone Lengthy-Brief Credit score Earnings Fund was by far the worst-performing closed-end fund of this grouping over the trailing five-year interval as soon as the distributions paid by every of the funds are taken under consideration. Whereas a fund’s previous efficiency is not any assure of its future outcomes, this can undoubtedly scale back the attraction of this fund relative to lots of its friends.

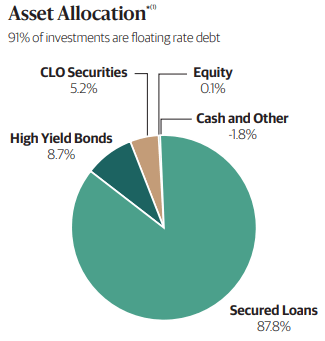

Within the quote from the fund’s web site above, it’s explicitly acknowledged that no less than 70% of the fund’s property shall be invested in floating-rate senior secured loans. The proportion as of the time of writing is considerably increased than this. We will see this right here:

Fund Truth Sheet

As we will clearly see, the fund presently has 87.8% of its property invested in senior secured loans. We will additionally see that 5.2% of the fund’s property are invested in collateralized mortgage obligations, which additionally are typically floating-rate securities. Thus, 93% of the fund’s property right this moment are invested in securities which have variable rates of interest (the 91% proven within the chart above is the results of subtracting the damaging money place because the fund must pay curiosity at variable rates of interest on that place). Clearly, this fund’s administration is anticipating that rates of interest will stay excessive for fairly a while, as it will scale back its publicity to floating-rate securities to nearer to 70% and buy junk bonds if administration believed that rate of interest cuts have been on the horizon. I need to admit that I agree with the fund’s administration on this respect. In a latest article, I made the case that the financial information is presently far too robust to justify rate of interest cuts. Certainly, the 2 most up-to-date inflation reviews counsel that inflation is definitely getting worse, and the correct plan of action is for the Federal Reserve to boost charges additional. Whereas I doubt that the central financial institution will truly take that step, it does appear probably that rates of interest will stay at pretty excessive ranges for fairly a while. The Blackstone Lengthy-Brief Credit score Earnings Fund definitely seems to be effectively positioned for that situation proper now, which is one thing that traders in it ought to have the ability to recognize.

Apparently, the fund appears to be growing its allocation to floating-rate securities. The final time that we mentioned it, the fund had a 15.5% allocation to high-yield bonds and decrease allocations to each secured loans and collateralized debt obligations. On the time, it additionally had a web of 85% of its holdings invested in floating-rate securities. Once we contemplate the dates on the charts proven in each the earlier article and above (October 31, 2023, and December 31, 2023), it seems that the fund was unloading bonds through the euphoria of the ultimate two months of 2023. That was a really good move in hindsight because it allowed the fund to unload bonds in a falling long-term rate of interest setting and thus earn some capital beneficial properties, relying on the worth that it paid to amass these bonds that it offered. The fund’s web asset worth elevated by 4.29% through the closing quarter of 2023 so that means that it did handle to earn some capital beneficial properties because it rotated out of junk bonds and into floating-rate securities.

Leverage

As is the case with most closed-end funds, the Blackstone Lengthy-Brief Credit score Earnings Fund employs leverage as a way of boosting the efficient yield and complete return of the property in its portfolio above that of any of the underlying property. I defined how this works in my earlier article on this fund:

Briefly, the fund borrows cash after which makes use of that borrowed cash to buy senior secured loans and junk bonds. So long as the yield that the fund receives from the bought securities is increased than the rate of interest that the fund has to pay on the borrowed cash, the technique works fairly effectively to spice up the efficient yield of the portfolio. As this fund is able to borrowing cash at institutional charges, that are significantly decrease than retail charges, this can normally be the case.

It is very important notice that the usage of leverage to spice up efficient yields shouldn’t be as efficient right this moment with charges at 6% because it was a couple of years in the past when rates of interest have been successfully zero. It’s because the distinction between the speed at which the fund can borrow and the yield that it receives from the bought property is far narrower than it as soon as was.

The usage of debt on this trend is a double-edged sword. It’s because leverage boosts each beneficial properties and losses. As such, we wish to be certain that a fund shouldn’t be using an excessive amount of leverage as a result of that might expose us to an extreme degree of danger. I usually don’t wish to see a fund’s leverage exceed a 3rd as a proportion of its property because of this.

As of the time of writing, the Blackstone Lengthy-Brief Credit score Earnings Fund has leveraged property comprising 31.23% of its total portfolio. That is considerably lower than the 37.68% leverage that the fund had the final time that we mentioned it, which isn’t particularly stunning. As already talked about, the fund’s web asset worth elevated by 2.84% because the date of our earlier dialogue:

Yahoo! Finance

Whereas that won’t appear to be a enough enhance to cut back the fund’s leverage by such a large proportion, it’s potential that the fund paid off a few of the leverage that it beforehand had. The fund’s annual report does certainly state that the fund diminished its leverage through the yr, though it doesn’t state precisely when the reductions befell. Nonetheless, the combination principal quantity borrowed was $77.200 million on the finish of 2023 in comparison with $82.800 million in the beginning of the yr. Thus, the fund clearly did scale back its leverage sooner or later within the second half of the yr, as the combination quantity excellent as of June 30, 2023, was $79.800 million. That determine was the quantity that was used to derive the fund’s leverage the final time that we mentioned it because it was essentially the most present determine obtainable.

Thus, what we’ve got right here is that the fund each paid down a few of its borrowings and elevated its web asset worth because the time of our earlier dialogue. Total, that is fairly good to see because it brings the fund’s leverage all the way down to the same degree as possessed by its friends. The fund’s leverage can be now below the one-third of property degree that we wish to see from a closed-end fund. Total, there appears to be little to fret about right here because the Blackstone Lengthy-Brief Credit score Earnings Fund is putting an affordable stability between danger and reward with respect to its leverage.

Distribution Evaluation

As talked about earlier on this article, the first goal of the Blackstone Lengthy-Brief Credit score Earnings Fund is to offer its traders with a really excessive degree of present revenue. In pursuance of this goal, the fund purchases floating-rate and fixed-rate debt securities issued primarily by below-investment-grade firms. These securities are likely to pay very excessive coupon charges to their homeowners, particularly in right this moment’s high-interest charge setting. The fund collects these coupon funds and combines them with any cash that it manages to acquire by exploiting the worth fluctuations in some debt securities that accompany rate of interest adjustments out there. This fund then takes issues a bit additional and borrows cash to be able to management extra securities than it may acquire just by relying by itself fairness capital. This enables the fund to gather extra coupon funds and capital beneficial properties and thus enhance the full return that it generates on the fairness capital. The fund pays out the entire cash that it earns from these numerous strategies to its traders, web of its bills. We would anticipate that this may end result within the fund’s shares additionally having a really excessive yield.

That is definitely the case because the Blackstone Lengthy-Brief Credit score Earnings Fund pays a month-to-month distribution of $0.1050 per share ($1.26 per share yearly), which provides it a ten.26% yield on the present worth. As talked about within the introduction, this compares moderately to lots of the fund’s friends, though it’s not the best yield round. Sadly, the fund’s distribution tends to range fairly a bit over time because it has raised and lowered it quite a few instances since its inception:

CEF Join

It will nearly definitely show to be a turn-off for traders who’re looking for to earn a protected and safe revenue from the property of their portfolios. Nonetheless, it’s not precisely uncommon for a fund resembling this to have a variable distribution. Certainly, the fund’s personal documentation states that the distribution will range infrequently. From the March 2024 distribution announcement:

The Funds declare a set of month-to-month distributions every quarter in quantities intently tied to the respective Fund’s latest common month-to-month web revenue. Because of this, the month-to-month distribution quantities for the Funds usually range quarter-to-quarter, and shareholders of any Fund mustn’t anticipate that Fund to proceed to pay distributions in the identical quantities proven above.

The rationale that that is completed is as a result of the quantity of revenue that the fund receives from its floating-rate property varies with rates of interest and the essential purpose is for it to solely pay out its funding income and hold its fairness principal intact. This could be certain that the fund shouldn’t be paying out greater than it might actually afford, however we must always nonetheless examine it to make certain.

Luckily, we’ve got a really latest doc that we will seek the advice of for the needs of our evaluation. As of the time of writing, the fund’s most up-to-date monetary report is its annual report which corresponds to the full-year interval that ended on December 31, 2023. A hyperlink to this doc was supplied earlier on this article. It is a a lot newer report than the one which we had obtainable to us the final time that we mentioned this fund, which is good as beforehand we solely had details about the fund’s efficiency for the primary half of 2023. There have been two broadly disparate markets within the second half of 2023, so it is going to be good to see how the fund navigated them. The primary of those markets occurred through the summer season months, as bond costs declined whereas long-term rates of interest rose as a result of the market was making an attempt to digest the truth that it was flawed a few near-term Federal Reserve pivot and high-interest charges being with us for a really very long time. The reverse occurred within the closing two months of the yr, as traders aggressively bid up the costs of fixed-income property in anticipation of a speedy discount in rates of interest this yr. These environments may have prompted the fund to expertise each beneficial properties and losses and this report will give us a good suggestion of how effectively it navigated these circumstances and delivered income to its shareholders.

For the full-year interval, the Blackstone Lengthy-Brief Credit score Earnings Fund obtained $24,689,003 in curiosity from the property in its portfolio. Maybe surprisingly, it had no funding revenue from every other supply. The fund paid its bills out of this quantity, which left it with $16,070,215 obtainable for shareholders. This was, sadly, not sufficient for the fund to completely cowl its distribution, though the fund did handle to get fairly shut. Over the twelve-month interval, the fund paid out a complete of $17,041,796 to its traders. At first look, this could possibly be regarding because the fund did fail to completely cowl its distribution out of web funding revenue and we usually wish to see a fund resembling this solely paying out its web funding revenue.

With that mentioned, the fund does produce other strategies obtainable by means of which it might acquire the cash that it must cowl the distribution. For instance, it’d have the ability to benefit from the curiosity rate-driven adjustments in bond costs to make some capital beneficial properties income by buying and selling these securities. Realized capital beneficial properties should not thought of to be funding revenue for tax or accounting functions, however clearly, they do present the fund with cash that may be paid out to shareholders.

The fund had blended outcomes at incomes cash by way of these different sources through the interval. It reported web realized losses of $7,329,703 however this was greater than offset by $15,691,034 web unrealized losses. Total, the fund’s web property elevated by $7,389,750 after accounting for all inflows and outflows through the interval. Thus, the fund did total handle to cowl its distributions. This doesn’t imply that we don’t want to fret a few distribution change although as this fund does have a tendency to alter its distributions on a quarterly foundation to coincide with the fund’s revenue.

Valuation

As of March 14, 2024 (the latest date for which information is presently obtainable), the Blackstone Lengthy-Brief Credit score Earnings Fund has a web asset worth of $13.38 per share however the shares commerce at $12.32 every. This provides the fund’s shares a 7.92% low cost on web asset worth on the present worth. This is a reasonably large low cost, though it’s not so good as the 8.60% low cost that the shares have traded at on common over the previous month. Thus, it is perhaps potential to get a greater worth by ready a bit bit, however actually, the present low cost is massive sufficient to justify initiating a place in order for you this fund.

Conclusion

In conclusion, the Blackstone Lengthy-Brief Credit score Earnings Fund is an fascinating credit score fund that seems to be making the proper strikes contemplating that the present interest-rate setting is more likely to persist for longer than many individuals are presently anticipating. The fund has been growing its allocation to floating-rate securities on the expense of fixed-rate bonds that can most likely decline in worth if the Federal Reserve fails to chop charges 4 instances this yr (the most definitely end result given latest inflation information). The fund’s distribution tends to range fairly a bit from quarter to quarter, however that is affordable, and the valuation is enticing.

For now, I’m sustaining my maintain score on this fund. I can’t blame anybody for getting it, however the fund’s underperformance relative to its friends reduces its desirability considerably.