kertlis/E+ by way of Getty Photographs

Thesis

BlackRock Floating Fee Earnings Belief (NYSE:BGT) is a closed finish fund. The car focuses on leveraged loans and has present earnings as its major aim. The CEF comes from the BlackRock household of funds, and presently sports activities a 5 star Morningstar score. One of many defining traits of this asset class is the brief period profile, and the CEF doesn’t disappoint from this standpoint, with an general period of solely 0.27 years.

We’ve got been bullish this asset class for some time now, with Purchase rankings assigned to BGT’s opponents:

- VVR: A ten% Yielding CEF That Is Truly Rising Its Distribution rated a Purchase late final 12 months and up 19% since

- FTSL: Unleveraged Floating Fee Loans, 8.4% Yield rated a Purchase mid 2023 and up since

When a leveraged mortgage CEF you will need to get a way of the analysis capabilities of the asset administration platform, the fund’s leverage ratio, credit score threat profile and historic track-record. BGT comes from a premier international asset supervisor, has a small ‘CCC’ bucket and a conservative leverage ratio of 25% (there are leveraged mortgage CEFs with 35%+ leverage ratios for instance). The fund has a really sturdy historic efficiency and benchmarks favorably with the golden requirements within the leveraged mortgage CEF area.

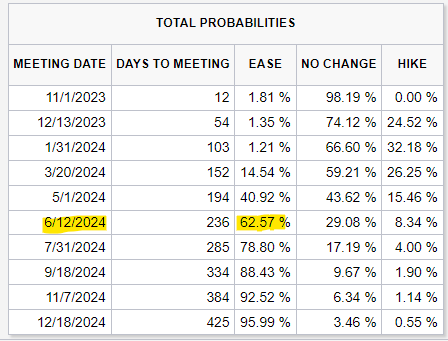

Whereas the Fed is signaling it’s performed elevating charges for now, however knowledge dependent, the markets are pricing a excessive price setting for longer:

Fee Reduce Chances (CME)

If we have a look at the ahead Fed Funds curve and the implied price possibilities, we’ll discover that market individuals will not be pricing in a Fed reduce (above 50% likelihood) till mid 2024. A excessive price setting for longer interprets into floating price property with the ability to cross a excessive price of curiosity to holders till the Fed begins slicing. Moreover, the great thing about the asset class resides in its brief period, therefore even when we’ve an surprising spike in inflation and the Fed is compelled to lift charges once more, floating price loans is not going to have a detrimental worth affect.

At this juncture, with some deteriorating fundamentals however yields larger for longer, leveraged mortgage funds simply make sense as a excessive dividend supplier. Mounted price funds run the danger of upper charges, whereas equities are held in place by the ‘Magnificent 7’ solely. As a retail investor, if you don’t want to attend it out in money, then floating price loans is the place to allocate capital in at present’s setting.

There’s a lot to love about BGT – beginning with the asset supervisor and the profile of the collateral pool, and ending with the floating price nature of the underlying loans and the sturdy historic efficiency. The principle threat issue to pay attention to and take into account is a credit score unfold shock, the place the market sells off and credit score spreads bounce a lot larger, thus affecting the pricing. The identical threat is borne by the fastened price excessive yield market, so all else equal in under funding grade credit, a retail investor ought to select floating price loans given their period hedge on this rate of interest setting.

Analytics

AUM: $0.26 billion.

Sharpe Ratio: 0.83 (3Y).

Std. Deviation: 5.7 (3Y).

Yield: 11.7%.

Premium/Low cost to NAV: -8%.

Z-Stat: 0.47.

Leverage Ratio: 25%

Length: 0.27 years

Composition: Leveraged Loans

Efficiency

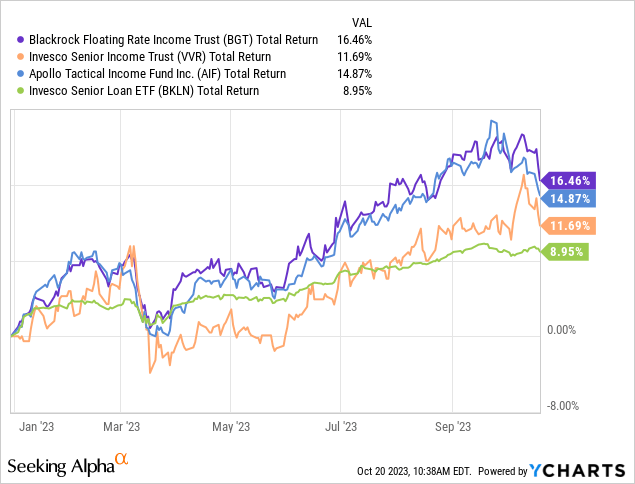

The CEF has outperformed this 12 months when in comparison with its peer-group:

We’re benchmarking the CEF towards a number of the ‘golden requirements’ within the area, specifically the Invesco Senior Earnings Belief (VVR) and the Apollo Tactical Earnings Fund (AIF), in addition to the unleveraged ETF Invesco Senior Mortgage ETF (BKLN). BGT outperforms all its CEF friends, whereas BKLN lags attributable to its lack of leverage.

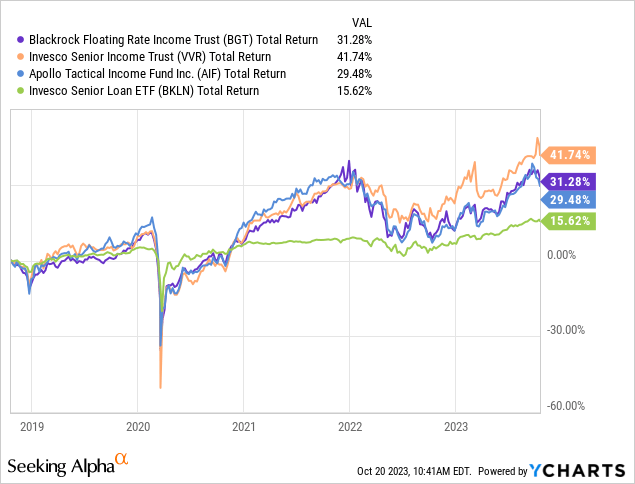

Long run the story is analogous, with BGT managing to publish extraordinarily sturdy whole returns:

On a 5-year lookback VVR is the winner, nevertheless BGT and AIF have related whole return profiles.

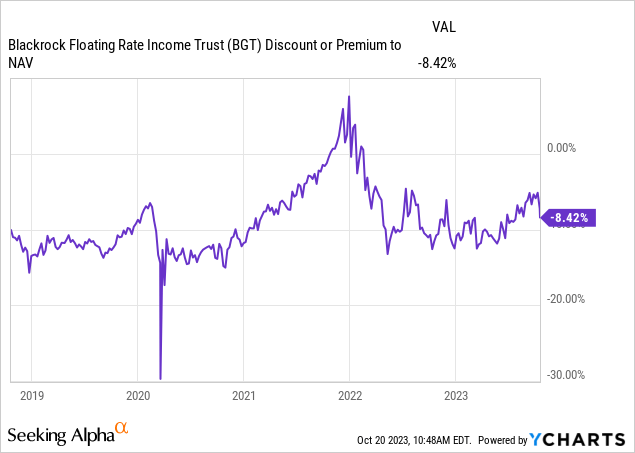

Premium/Low cost to NAV

The fund’s low cost to NAV has an in depth correlation to rates of interest:

Throughout normalized rate of interest environments the CEF has a really secure low cost to NAV that fluctuates round -10%. Throughout the vital financial easing skilled in 2020/2021, the CEF narrowed to flat to NAV attributable to its excessive yield.

We don’t anticipate a lot of a windfall from low cost narrowing within the subsequent 12 months, and wouldn’t have a look at this issue as additive to the CEF’s returns for now.

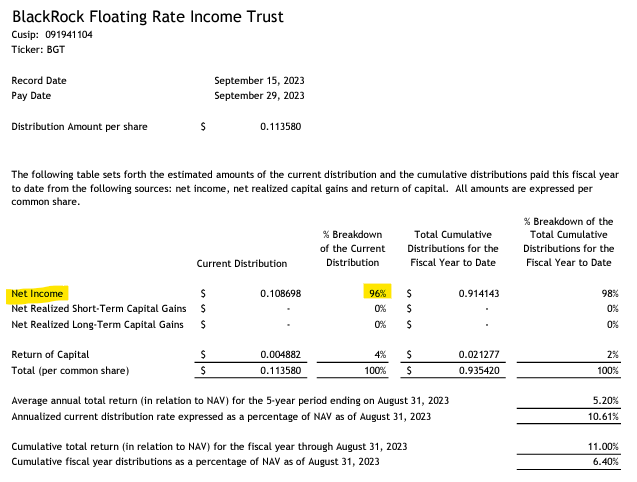

Distributions

The fund does a great job of protecting its distribution yield:

Part 19a Discover (Part 19 Discover)

As of the September cost date, 96% of the distribution got here from the earnings obtained from the underlying loans, with solely a 4% ROC utilization.

The maths is smart, with SOFR at 5.3% and spreads on leveraged loans at roughly 5%. Once you add leverage on prime you possibly can see how the fund obtains its 11.7% distribution yield. As charges keep excessive for longer, anticipate an excellent protection for this distribution yield.

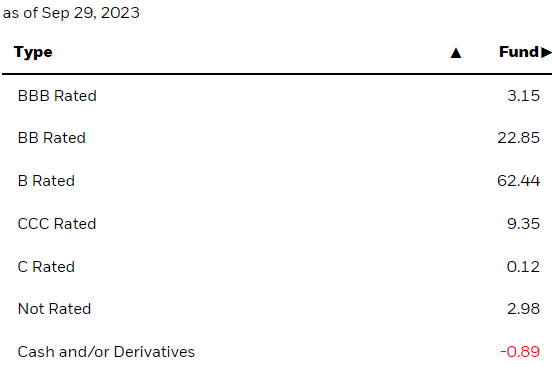

Collateral

The fund is a middle-of the highway one, with no extreme credit score threat:

Scores (Fund Web site)

The identify is chubby ‘B’ names which make up 62% of the portfolio, whereas the riskiest collateral, specifically ‘CCC’ loans, characterize simply 9.35% of the fund.

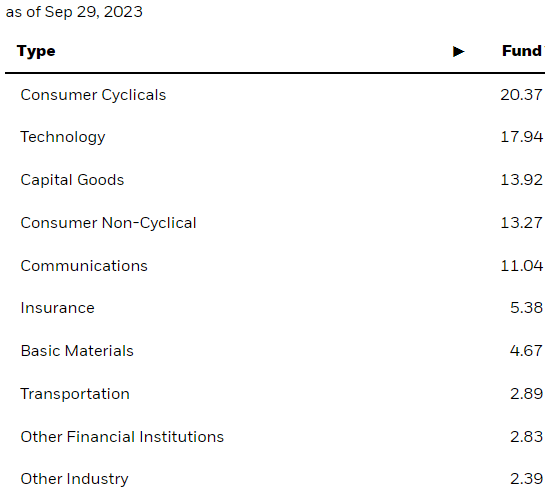

The identical composition characteristic might be discovered within the sectoral distribution, the place the trade focus is balanced out:

Sectors (Fund Reality Sheet)

As an investor you don’t want to see any sector above 25% of a fund, as a result of it might characterize an chubby positioning in a sure sector. Whereas there are numerous funds which specialize on sure corners of the market, they’re very forthcoming about their slim focus and threat elements. In a middle-of-the-road leveraged mortgage CEF you wish to see diversification.

Conclusion

BGT is a hard and fast earnings closed finish fund. The CEF focuses on leveraged loans and comes from a premier asset supervisor. The fund has very sturdy historic returns, matching and even beating different ‘golden requirements’ within the area, specifically VVR and AIF.

The CEF has a conservative composition, with a low 25% leverage ratio and a collateral pool that doesn’t take extreme dangers by way of ‘CCC’ credit. The fund virtually totally covers its distribution, and we anticipate it to proceed to take action till the Fed begins slicing charges. Though the CEF trades at a -8% low cost to NAV, we don’t anticipate vital fluctuations there, and no actual windfall from buying and selling this threat issue right here.

We like BGT for what it’s, specifically a car that extracts a excessive yield from a floating price under funding grade asset class. Each loans and BGT have low commonplace deviations, and have confirmed to be a really worthwhile device for the reason that Fed began elevating charges in 2022. We’re nonetheless bullish on this asset class and like this 5 star mortgage CEF right here.

{kind=link}