")

Dr_Microbe/iStock by way of Getty Photographs

I’ve analyzed Aurinia Prescription drugs (AUPH) on quite a lot of events, most lately on Could 30, 2021 the place I offered a revamped gross sales mannequin which I used to determine a reduced money stream evaluation and inventory goal value. Since that point the inventory has had a wild trip, first buying and selling as much as practically $34 on takeover hypothesis, and now plunging to $10 on investor disappointment for 2022 steering.

bigcharts

(supply)

In right now’s article, I might wish to evaluate the explanations for the current inventory weak point after which replace/evaluate my mannequin to precise gross sales and money stream information. For readers new to the inventory, I extremely advocate studying my earlier articles to higher perceive the corporate and the deserves and security profile of its voclosporin drug (model title LUPKYNIS) which was permitted on the market by the FDA early final yr.

Why AUPH Inventory is Down

Firstly, I believe the inventory is down as a result of biotech shares normally have been hammered over the previous 4 months or so. This is the S&P Biotech index (XBI) over the identical interval because the AUPH graph above. It would not have the spike up that AUPH did, however spherical journey it is about the identical final result.

bigcharts

(supply)

Specific to AUPH itself are two components to elucidate its current descent. First is steering and second is issues about compliance and patent power. Let’s rapidly take a look at every of those.

Aurinia CEO Pronouncements and Precise Steerage

AUPH set itself up for disappointment when, 12 days earlier than earnings, its CEO, Peter Greenleaf, whereas presenting on the Annual Leerink SVB International Healthcare Convention, mentioned the market may count on “aggressive numbers” for its steering within the forthcoming earnings name. On the time, in response to the Globe and Mail, “Wall Road, for its half, was anticipating the halfway level of the corporate’s 2022 income forecast to return in at round $178 million”.

The precise steering supplied by AUPH in its earnings launch on Feb 28, fell method in need of that Wall St quantity:

“For fiscal yr 2022, the Firm is offering web income steering of $115 to $135 million from gross sales of LUPKYNIS. This vary is predicated on assumptions relating to the influence of COVID-19 on the present enterprise atmosphere and represents a rise of greater than 150 to 200% in web income from gross sales of LUPKYNIS in comparison with fiscal yr 2021.”

Discuss NOT managing expectations!

Affected person Adherence and Persistence

The second challenge is that there was some sufferers who’ve both began taking LUPKYNIS and stopped or who’ve been prescribed LUPKYNIS however have by no means crammed their prescription. This was talked about a number of instances on the current earnings name and it was discomfiting for analysts and traders. Here’s a taste of this sort of speak (with my emphasis):

In fact, and sadly, as extra sufferers start remedy with LUPKYNIS, we will count on to see some extra sufferers discontinuations. Whereas it is nonetheless too early to see statistically vital developments in general drop-off charges, to date, discontinuations are aligned with what we tracked in our medical trials, which is about 25% to 30%.

After we take a look at affected person adherence with LUPKYNIS, right here, too, it’s too early to quote rising developments. Keep in mind, the rising LUPKYNIS sufferers on drug began remedy in mid-Q3 and This fall of 2021. Clearly, most often, these sufferers have solely been on remedy between three to 6 months, so we are going to want extra time to know general adherence charges.

[…]

So on discontinuations and adherence, I might let you know that the explanations are throughout the Board. What I might underscore is, they are not payer associated. It is not like we’re getting PSFs that are available after which the payer shouldn’t be paying for the drug. That is not been one of many ones we have seen. However to attempt to vary in on a bunch — from a bunch of various causes as to why sufferers is perhaps discontinuing their product, it is form of throughout the board proper now.

All the pieces from tolerability to sufferers simply not choosing up prescriptions, which we are attempting to flesh out extra. Keep in mind, we’re coping with primarily a affected person inhabitants that is an African-American, Hispanic and Asian feminine inhabitants within the U.S., and we will look to different illness states as analogs to know that adherence and longer-term compliance are a problem with that inhabitants normally.

As we are going to see beneath, my mannequin was extra conservative than Wall Road’s normally, and so all of those points have been already baked into my DCF, therefore what’s disappointing to some, is not to me.

Patents

There was additionally a query about patents raised within the 10-Okay and earnings name. I imagine that is simply an exploratory transfer, so I am presently proud of the reason that AUPH gave on the decision:

We did obtain discover of an inter partes evaluate, or IPR, petition being filed on February 24 with respect to our patent that has claims directed at LUPKYNIS dosing protocol for lupus nephritis utilized in our medical trials.

As you all recall, that patent has a time period extending out to December of 2037. At this stage, it is actually too preliminary to provide a full evaluation of this IPR as a place — a petition that was filed from Solar Prescription drugs who you all might recall, in the event you’ve been studying our Ks, we’re suing for patent infringement in a separate matter, which I am going to discuss in a second, was actually simply obtained.

So we’re it, however we’re assured in our course of to prosecute all our patents. This patent particularly, had vital evaluate, as we have talked about beforehand on the U.S. Patent and Commerce Workplace earlier than being permitted as being precise legitimate patent by that workplace.

I believe that summarizes why the inventory is buying and selling as little as it’s. Now let’s flip to the larger image which is what’s going to gross sales seem like over the lifetime of the drug and what’s that value?

Preliminary Comparability of Gross sales and Money Stream to Mannequin

As I discussed, I offered my full mannequin in an earlier article, so for brand spanking new readers, I might counsel reviewing that to get into the nitty gritty of my assumptions. However as a fast recap, listed below are the fundamental mannequin parameters, adopted by the primary two years of predicted revenues and money flows:

Creator

(supply: Creator’s mannequin)

Creator

(supply: Creator’s mannequin)

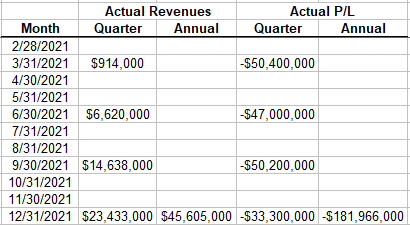

Precise Information

We now have a yr of precise revenues and money flows to match. To be conservative, I am utilizing P/L as a substitute of money flows as a result of the corporate does use stock-based compensation and I do not need that to make the mannequin look higher than it’s.

creator

(supply: Creator’s compilation of earnings information)

The preliminary information means that my mannequin may be very conservative; i.e. it overestimates money burn within the first yr by $20M and underestimates revenues by $29M. Or one other solution to put it, to date precise revenues are monitoring forward of predicted income by about 6 months.

Going ahead, I predict revenues of $105M in 2022 and money burn of about $125M. Each of this are seemingly very conservative, notably given the corporate’s income steering of $115M to $135M cited above. For 2023 I predict revenues of $333M and optimistic money flows of $80M. Provided that the corporate presently has $466M available (as of Dec 31, 2021) it should not have any want to lift money going ahead. Certainly, as talked about within the earnings launch:

[AUPH] [f]urther stabilized stability sheet by the utilization of an on the market providing (ATM), elevating web proceeds of $196.7 million by December 31, 2021, at a mean value of $19.91 and at a mean low cost of two.63%. The Firm has terminated the ATM gross sales settlement with no additional gross sales to happen beneath the ATM.“

As a few validation factors for my mannequin, take into account that

(1) analysts estimates for 2023 revenues presently vary from $275 to $391M which places me within the vary however nonetheless conservative.

in search of alpha

(supply)

(2) That the variety of SLE sufferers identified with LN is estimated to vary between 80,000 and 120,000 (see for instance 10). My mannequin would not have AUPH treating half of the low finish of the vary (i.e. 40,000 sufferers) till March of 2028, by which period the variety of identified sufferers will virtually actually be considerably larger than present estimates (in no small half as a result of efficient remedy will encourage extra correct diagnoses).

Lastly, as one other conservative side of my mannequin, there presently isn’t any accounting for any royalties or milestones from worldwide gross sales, even though Otsuka seems to be making stable progress in Europe.

Conclusion

On account of this train, I am extra satisfied of the worth of my mannequin. Factoring in a single much less yr of unfavourable money flows counterbalanced by a better absolutely diluted share depend provides me the identical value goal I had beforehand, viz. $75 with a 5 yr horizon to get there. Provided that the inventory is now buying and selling beneath $11, I am including to my place at right now’s costs.