Brandon Bell

AT&T (NYSE:T) is probably not essentially the most thrilling firm. Nonetheless, the underside should be shut once I see a 7% dividend and a 6.4 P/E ratio. Given the financial uncertainty, the slowdown impact, and different components, AT&T’s share worth has dropped by roughly 25% over the final 52 weeks. Sadly, we might neglect how necessary AT&T is to the U.S. and the American folks. Within the earlier 5 years, the corporate has invested a staggering $140 billion into American infrastructure. AT&T continues to steer the nation as essentially the most intensive fiber web supplier whereas enhancing America’s “most dependable” 5G community.

Moreover, AT&T is paying down debt and may proceed doing so to safe progress and preserve its dividend. Moreover, now that AT&T is now not in present enterprise, it might deal with its core operations, optimizing effectivity and enhancing profitability because the firm advances. AT&T’s inventory is exceptionally low cost now, and because the firm improves processes, its a number of ought to increase, resulting in a a lot greater inventory worth within the coming years.

Lastly – The Backside Is Shut

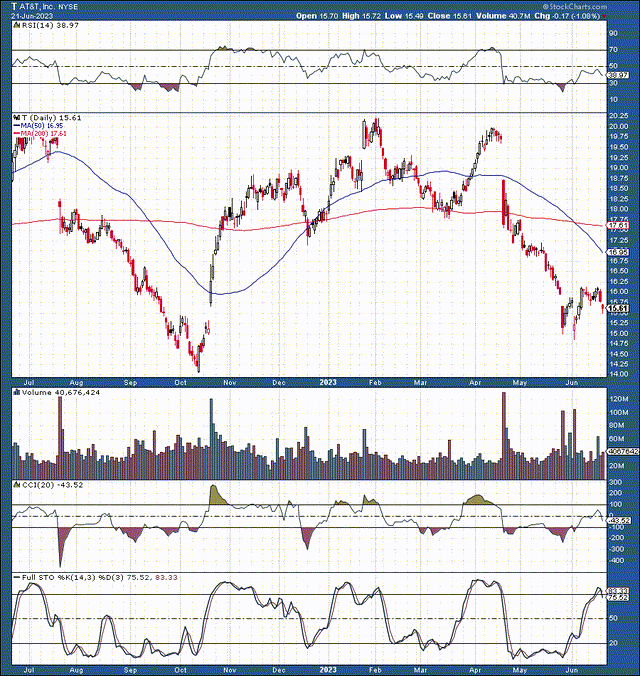

T (StockCharts.com)

$15 is the crucial assist degree. AT&T briefly dipped beneath this important degree through the peak and the panic promoting of the current bear market. Nonetheless, the inventory returned to check the $15 mark in late Might and early June. Thus, we had a take a look at, adopted by a profitable retest and a major reversal on the $15 zone. Due to this fact, the $15 is a major assist level, suggesting the draw back is restricted from right here.

Furthermore, the RSI went significantly beneath the 30 degree, hitting round 20 through the current route. These ultra-low readings within the RSI are across the ranges we witnessed through the bear market backside in mid-October final 12 months. Due to this fact, from a technical standpoint, AT&T’s inventory received deeply oversold lately, has a bullish (potential double-bottom) setup, and may proceed shifting greater as we advance.

AT&T – Paying Down Its Debt

Within the final two years, AT&T bought a 30% stake in its DirecTV unit for $7.1B and spun off WarnerMedia for $40.4 billion in money. Now, AT&T is reportedly working with Barclays to solicit bids for its cybersecurity enterprise it acquired for about $600 million in 2018. AT&T lowered its web debt by about $24B in 2022 and appears to proceed decreasing it to roughly $100B by 2025. Paying down debt is crucial for sustaining AT&T’s dividend and persevering with to develop within the fiber and the 5G house.

AT&T Nonetheless Wants A Administration Shakeup

Let’s face it. An enormous motive AT&T is within the mess that it is in is due to the corporate’s botched merger with Time Warner. After all, it was not a merger of equals, as AT&T acquired the corporate for an enormous sum. AT&T’s administration used a heavy-handed strategy at occasions, stifling Time Warner’s artistic potential and resulting in poorer high quality in its content material (arguably). AT&T’s administration was primarily centered on its agenda and didn’t hearken to the highest managers at WarnerMedia. The outcomes converse for themselves, and 5 years later, AT&T bought its WarnerMedia pursuits for about half of what the corporate paid initially.

How’s That For An Funding?

AT&T wants a administration shake-up. All the pieces has change into so stale and stiff at AT&T that the corporate wants new management. John Stankey has spent his total 37-year profession at AT&T. Now, that is factor, however it is usually a foul factor. How can we anticipate AT&T to reform its company tradition with a lifelong AT&T govt as CEO? A change is required for AT&T to change into extra environment friendly, growth-oriented, and more and more worthwhile. Due to this fact, extra modifications are wanted on the group’s high to enhance its backside line finally. Nonetheless, now that the media spinoff is full, AT&T can deal with its core operations, and its inventory is exceptionally low cost now.

Wait, How Low cost Is AT&T Now?

AT&T trades at a P/S ratio of 0.9 right here, and its P/E ratio is simply above a all-time low of 6.0 now. Furthermore, AT&T supplies a 7% dividend, probably making its inventory as low cost because it will get. This 12 months’s EPS needs to be within the $2.40-$2.60 vary. Whereas consensus estimates are for $2.43, my estimate is $2.50.

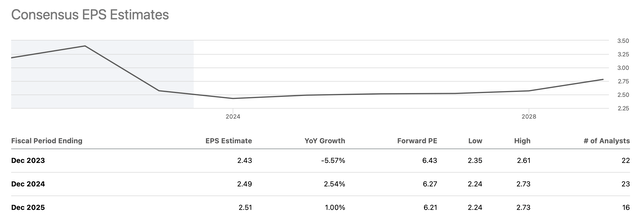

EPS Estimates – Prone to Broaden Extra

EPS Estimates (seekingalpha.com)

Do not thoughts the numerous drop in EPS, as it is not adjusted for the WarnerMedia spinoff. Nonetheless, EPS will probably present a slight decline from final 12 months. 2022 EPS got here in at $2.57, and this 12 months ought to are available in at about $2.50. We will attribute this phenomenon to a tighter financial setting and an financial slowdown, transitory components that ought to fade. Additionally, if we have a look at EPS surprises, AT&T has overwhelmed consensus estimates in its final ten quarters.

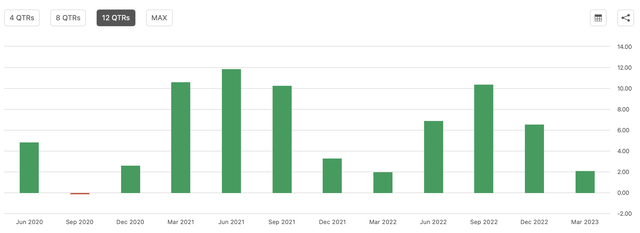

EPS Surprises – Development Prone to Proceed

EPS Surprises (seekingalpha.com)

In its final 4 quarters, AT&T has beat the consensus estimates by a mean of 6.5%. If we apply the same beat charge to 2023 full-year estimates, we arrive at $2.59 in EPS. Additionally, if we use the identical 6.5% beat charge to subsequent 12 months’s consensus determine, we arrive at an EPS of $2.65. If AT&T delivers $2.65 in EPS subsequent 12 months, its inventory is buying and selling at solely round 5.7 ahead earnings. This valuation is remarkably low cost, and AT&T’s inventory ought to transfer greater on modest earnings progress and a number of enlargement within the coming years.

Here is the place AT&T’s inventory might be in a number of years:

| Yr | 2023 | 2024 | 2025 | 2026 | 2027 | 2028 | 2029 |

| Income Bs | $122.5 | $124.8 | $128 | $131 | $134 | $137.5 | $140.5 |

| Income progress | 1.5% | 1.9% | 2.56% | 2.45% | 2.33% | 2.46% | 2.22% |

| EPS | $2.50 | $2.65 | $2.78 | $2.92 | $3.04 | $3.19 | $3.32 |

| EPS progress | N/A | 6% | 5% | 5% | 4% | 5% | 4% |

| Ahead P/E | 5.66 | 7 | 8 | 10 | 11 | 12 | 11 |

| Inventory worth | $15 | $19.50 | $23.36 | $30.40 | $35.09 | $39.84 | $45 |

Supply: The Monetary Prophet

The Backside Line – AT&T Is Grime Low cost

AT&T is exceptionally low cost right here, and its inventory ought to profit from gentle EPS progress and a number of enlargement within the coming years. Whereas preserving my projections modest, we nonetheless see that AT&T’s inventory may triple within the coming years. Due to this fact, AT&T is a robust purchase with restricted draw back danger and substantial upside potential as we advance. Additionally, there’s the 7% dividend to think about, which ought to proceed rising if the corporate meets my projections within the coming years.

{kind=link}