")

Courtney Hale

Abstract

Beforehand, I acknowledged that I used to be optimistic on American Nicely Corp (NYSE:AMWL) progress, which needs to be supported by behavioral well being as a big development driver, and likewise when CVS begins to ramp up. Nonetheless, as a result of lack of awareness, I really useful a maintain score. As I look ahead to the finalization of the Converge implementation, my score on AMWL stays at maintain.

Regardless of my optimism concerning the corporate’s long-term prospects, I’ve given it a maintain score resulting from considerations in regards to the impression that churn can have in 2Q23. I am fearful that the inventory will drop once more if there are any unhealthy headline numbers. Needless to say even with that 25% enhance from the low of $2, the inventory continues to be down considerably from the $4+ firstly of the yr. The “promoting stress forward” continues to be substantial, in my view. Positively (and in keeping with my long-term perspective), nonetheless, administration has emphasised the speedy progress made in migrating to the Converge platform, with income anticipated to renew its upward development in 2H23. Put collectively, it appears clear to me that the most effective time to take a position can be in 2H23 when Converge settles, and administration can begin guiding aggressively when the advantages of Converge surfaces.

Converge implementation in focus

For readers which are new to the title, AMWL is a yr into implementation and execution with give attention to the Converge platform. The excellent news is that implementation is on observe to completion over the following 12 months. Because the variety of new prospects migrating to the legacy platform is anticipated to be negligible after FY24, the total results of Converge will turn out to be obvious at the moment. Whereas all is nice, I wish to this migration similar to many software program corporations that migrated their prospects to cloud (from on-premises). The very fact of the matter is that with every migration, particularly a big one like AMWL, there shall be churn. There are 2 kinds of prospects that can churn, for my part:

- Consumer that aren’t heavy customers and sometimes solely use restricted features like video conferencing. AMWL doesn’t present loads of worth to those group of customers, and they’re prone to swap out when it will get “troublesome”.

- Customers which have been sad with AMWL options, service, and so on., however stayed on as a result of it’s simpler to proceed utilizing than consider and migrate. These teams of customers will seemingly churn when they’re pressured to judge different decisions (on this case is AMWL migration to Converge).

For these two teams, they are going to be onerous to retain and upsell additional merchandise anyway, so I view them as low-quality prospects that can finally churn. Luckily, administration reported that that they had seen solely somewhat churn within the center market and none in any respect amongst their most beneficial strategic shoppers.

Margin

I’d be looking out for elevated gross and working margins after the migration. With respect to gross margin, it ought to profit from the sunsetting of the legacy platform (which saves ~$5-10 million a yr), and I count on gross margins to profit as combine shifts away from Go to income (~50% of whole income). Since Go to sometimes have gross margins within the mid-20% vary and subscription companies sometimes have margins within the 60+% to 70% vary, the latter impression would have a better cumulative impact over time (subscription will finally take up many of the combine).

As for EBIT margin, I count on the R&D line to say no because the Converge transition is accomplished. This is a vital level to notice and mannequin as there’s a sizable quantity of R&D spend tied to the event of Converge that’s going to move out of the system. If we take a look at administration’s information, they reiterated that R&D in 4Q23 shall be greater than 20% beneath the prior yr stage – which is a tell-tale that AMWL will see better working leverage from then on. All in all, I consider margin goes to inflect sooner or later, and that shall be a catalyst to the share worth growing.

Valuation

Probably the most troublesome a part of modeling AMWL right now, in my view, is figuring out what a number of it is going to be value as soon as development accelerates with a extra seen path to earnings. Begin from the income forecast, as I discussed earlier, FY23 goes to be just about a muted yr, however development will begin inflecting in FY24 as AMWL sees no extra incremental churn.

Following the migration, administration will be capable to dedicate all of their efforts to driving development. The difficult half is modelling earnings that are nonetheless in damaging territory right now. It is going to take a while for margins to inflect to optimistic territory, which I consider the market is closely discounting. Nonetheless, given the higher development outlook and margin profile (FY21 income grew solely 3.1% with a -58% adj. EBITDA margin), I consider the inventory can be valued at the very least on the identical a number of because it was in late FY21. Nonetheless, I reiterate that the most effective time to purchase is prone to be in 2H23 and even FY24, because the migration shall be practically full by then.

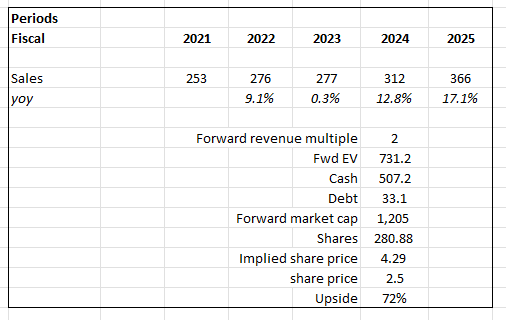

Personal mannequin

Conclusion

My present score on AMWL stays at maintain. Though I’m optimistic in regards to the firm’s long-term prospects, I’ve considerations in regards to the potential impression of churn within the second quarter of 2023. The inventory has already skilled important downward motion, and I fear that any damaging headline numbers might trigger additional decline. Nonetheless, administration has highlighted the progress made in migrating to the Converge platform, with expectations of income development resuming within the 2H23. As such, I consider the most effective time to spend money on AMWL can be in 2H23 and even in FY24 when the Converge migration is almost full and administration can present aggressive steering primarily based on the advantages of Converge. Moreover, I anticipate elevated gross and working margins after the migration, which might act as a catalyst for share worth enhance.