KenWiedemann

Funding Thesis

Slate Grocery (SGR.UN:CAD and USD ADR SRRTF) is a REIT specializing in retail area anchored by grocery shops. Slate owns 117 properties throughout 24 states, averaging $12.37/sqft in hire throughout 15.3 million sqft.

Grocery-anchored retail is uniquely positioned to climate financial hardships. The need of grocery procuring ensures regular shopper visitors and constant spillover into different stores close by. Slate’s steady property portfolio, geographic variety, and superior 9.7% distribution make it a superb buy for the defensive revenue investor.

Estimated Honest Worth for SGR.UN in Canadian {Dollars}

EFV (Estimated Honest Worth) = EFY24 FFO (Funds From Operations) occasions P/FFO (Value/FFO)

EFV = E25 FFO X P/FFO = $1.54 X 10.5 = $16.20

|

E2024 |

E2025 |

E2026 |

|

|

Value-to-Gross sales |

2.2 |

2.2 |

2.2 |

|

Value-to-FFO |

5.8 |

5.6 |

5.3 |

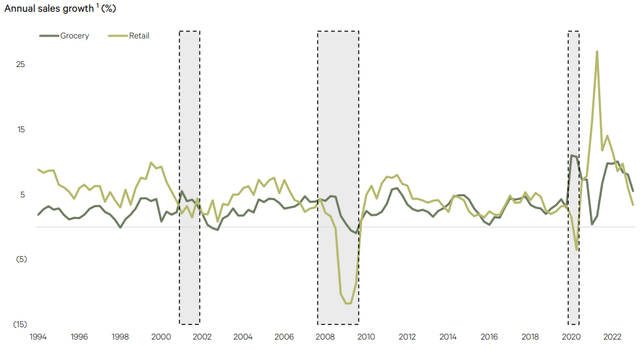

Market Circumstances

Grocery-anchored retail outperforms the sector throughout occasions of financial hardship. Even throughout occasions of financial hardship, customers require meals. Regardless of the uptick in supply and different distribution channels, 94% of grocery demand is fulfilled by bodily storefronts. Retail close to grocery anchors induces important spillover, with an estimated 49% improve in visitors to retailers inside 0.1 miles of a grocery retailer.

Retail has been affected by the identical headwinds as residential actual property, with restricted new development leading to robust demand and excessive costs. Given the lengthy leases on the grocery anchors, SGR has excessive occupancy charges, renewal charges, and stability in AFFO (adjusted funds from operations) throughout financial situations and geographies.

Slate

Portfolio Overview

The portfolio is all grocery-anchored retail and is 47% grocery leasable space. Of complete leasable area, 69% is taken into account important tenancy – offering items and providers which can be revenue inelastic, which means customers will at all times demand them no matter financial situations. At the moment, Slate has 94.1% occupancy and 99.3% grocery occupancy.

Occupancy charges have elevated 90bps yr over yr, reaching the best degree since earlier than the pandemic.

|

Sort |

% of complete Leasable area |

Weighted common lease time period (years) |

|

Grocery (Anchor) |

43.8% |

5.2 |

|

Retail (non-anchor) |

48.3% |

4.2 |

|

Vacant |

5.9% |

– |

Portfolio enlargement is concentrated within the fast-growing sunbelt, making up 45% of the portfolio. Since 2021, Slate has acquired about $900 million in property. These acquisitions have a monetary profile averaging $12.54/sqft in hire and 42.8% grocery area, which aligns with the present portfolio.

Throughout the entire portfolio, 43.2% of leases expire in 2028 or later, which gives important stability to operations whereas additionally permitting for some short-term will increase in hire. At the moment, 25% of leasable area is up for renewal within the subsequent 3 years. This has elevated the rental unfold, with present hire averaging $12.37/sqft, new leases averaging $18.76/sqft, and $12.95/sqft for renewals.

|

Sort |

Sqft |

Common Base Lease |

Unfold (distinction between outdated hire, and new hire) |

|

Renewal |

<10,000 |

$23.18 |

10.1% |

|

Renewal |

>10,000 |

$9.63 |

8.3% |

|

New Lease |

<10,000 |

$21.40 |

24.3% |

|

New Lease |

>10,000 |

$13.00 |

1.0% |

Moreover, 98% of Slate’s tenants are on web leases, requiring them to pay at the very least a part of the property’s upkeep and taxes, which considerably reduces Slate’s working prices.

Danger

Slate has a positive threat profile concerning tenants, with no tenant making up greater than 7% of complete hire. The highest 15 tenants account for 45.5% of leasable area and 35.2% of base hire. On condition that all the high 15 tenants are anchor grocers, it’s unlikely that any single tenant will go away Slate’s places and trigger vacancies for a major time.

The Kroger-Albertsons merger could pressure some former Kroger places to change into vacant. If the merger is authorised, Kroger-Albertsons states they are going to unload roughly 400 retail places in the course of the merger. Slate doesn’t presently consider this can meaningfully have an effect on operations, given they’d be bought to different grocery retailers.

Complete debt is 96.1% fixed-rate debt at 4.2% rate of interest. The debt protection ratio (curiosity to EBITDA) is just 2.9x. This low ratio is suboptimal for an setting with increased rates of interest as debt rolls over. Nonetheless, Slate has important web revenue will increase on the horizon as increased renewal rents enhance revenues.

Outlook

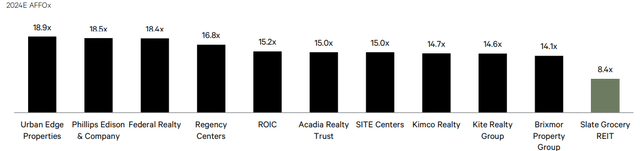

Slate trades at 8.4x adjusted funds from operations, considerably decrease than the sector common. Slate presently has a capitalization fee of 8.5% on the finish of the quarter ending September. In comparison with friends, 8.5% capitalization may be very favorable, with the typical US REIT sitting at round 7.3%

Slate

It has a 9.7% yield for the September quarter, distributing 80% of FFO (funds from operations) quarterly, placing it firmly on the high of its friends.

The identical property’s web revenue has elevated 2% over the earlier 12 months, with the weighted common new hire being 16.4% increased than the expiring hire within the quarter ending September. We consider that same-property web revenue will improve quicker than 2% over the following 3 years, given the expiring leases and important leasing unfold skilled up to now in 2023. Slate has a positive 100% renewal/retention fee on its anchor tenants, giving a weighted common renewal fee of 94.1%.

|

Quarter ending September |

Variety of Tenants |

Weighted Common Lease ($/sqft) |

Change |

|

Renewals |

68 |

$12.95 |

9.1% |

|

New Leases |

31 |

$18.76 |

– |

|

Complete / Weighted Common |

99 |

$13.82 |

16.4% |

In conclusion, Slate gives important recession resistance and has secular tailwinds with restricted new growth, particularly in non-growth markets. Slate gives a compelling funding proposition, particularly for defensive revenue traders. Its give attention to important, grocery-anchored retail gives a buffer towards financial downturns. The REIT’s robust occupancy charges, diversified portfolio, and favorable financials place it nicely for sustained web revenue development and stability throughout the present portfolio, making it a lovely selection in the true property sector. Furthermore, the mix of upper yield and decrease valuation than its friends makes the present value compelling.

Editor’s Observe: This text discusses a number of securities that don’t commerce on a serious U.S. change. Please concentrate on the dangers related to these shares.

{kind=link}