jetcityimage

It’s laborious being an AT&T (NYSE:T) shareholder. It doesn’t matter what AT&T does, it is by no means sufficient. Over the previous decade, shares have declined -42.36%, and if that is not sufficient, shareholders have seen Warner Bros. Discovery (WBD) shares drop -55.32% because the spinoff. The newest shoe to drop was the report that Amazon (AMZN) was contemplating providing cell service to its Prime prospects. AMZN is the final firm shareholders of T ought to need to collide with as they outspend the competitors and have a loyal Prime membership base that is not leaving. Whereas I really feel AMZN getting into the communications house could be a catastrophe for each competitor within the communications house, I feel it’s unlikely they’ll embark on that endeavor. The market wasn’t pleased with the outcomes from Q1 2023, however should you consider administration projections, AT&T seems to be extraordinarily undervalued. It is laborious to remain bullish, and I’m conscious that AT&T has been an enormous worth lure. I’m adverse on my funding, and I’m certain many different shareholders are additionally. I really really feel greenback value averaging beneath $16 is a long-term reward, and if in case you have time in your aspect, AT&T could also be value hanging on to.

In search of Alpha

Why Amazon getting into the communications house could be a nightmare for communication corporations

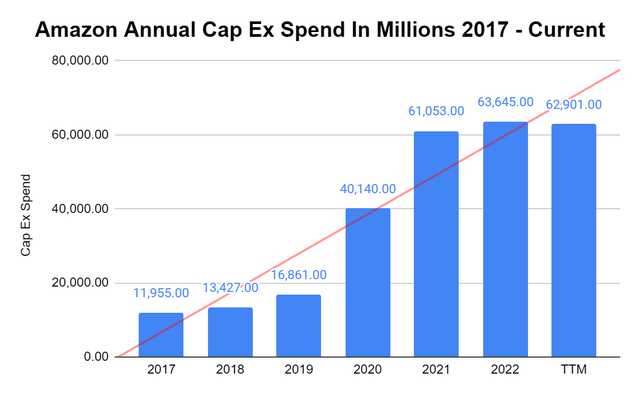

AMZN is prepared to spend as a lot because it takes to win. If AMZN decides to enter the communication house I consider it will likely be devastating for the present communications corporations. In 2020, AMZN’s capital expenditure (CapEx) spending elevated from $16.86 billion to $40.14 billion. Then in 2021, the CapEx spend elevated to $61.05 billion, and in 2022 AMZN allotted $63.65 billion towards CapEx. That is vital as a result of CapEx is the pool of cash that an organization allocates towards buying, upgrading, and sustaining bodily belongings, which may embrace property, crops, buildings, expertise, or gear.

Steven Fiorillo, In search of Alpha

Have a look at what occurred within the retail house. AMZN realized that the buyer was valuing effectivity and the way rapidly they obtained merchandise increasingly. By constructing a best-in-class logistical community, AMZN was capable of dominate the e-commerce house, and provide same-day supply in some main cities, whereas providing next-day delivery to many areas for Prime members. This occurred by AMZN outspending its rivals and constructing probably the most in-depth logistical community.

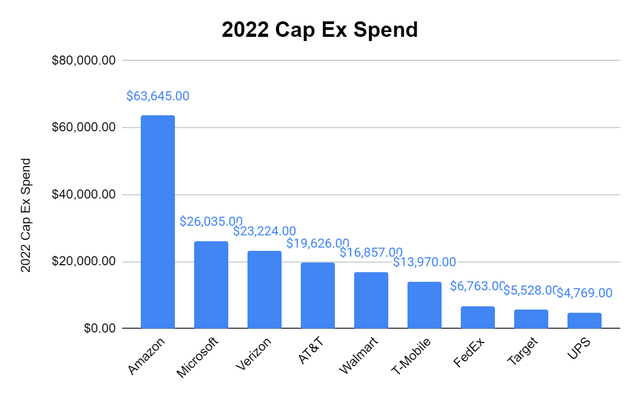

Along with taking over Microsoft (MSFT) within the cloud house, AMZN determined to regulate its personal future and never depend upon FedEx (FDX) or United Parcel Service (UPS) for delivery its merchandise when competing within the client items house in opposition to Walmart (WMT) and Goal (TGT). In 2022 the mixture of MSFT, WMT, TGT, FDX, and UPS CapEx was $59.95 billion, and AMZN outspent these 5 entities by $3.69 billion. Whereas AMZN went head-to-head with MSFT, it additionally went head-to-head with the incumbents in delivery and made Prime the go-to methodology for a lot of Individuals.

Steven Fiorillo, In search of Alpha

Now the query turns into, if AMZN does enter the communications house, will they spend to win? I feel the reply could be sure, however that is an opinion. In 2022, Verizon (VZ) allotted $23.22 billion towards CapEx, whereas AT&T spent $19.63 billion, and T-Cellular (TMUS) spent $13.97 billion on CapEx. That is hypothesis, however after 3 years (2020 – 2022) of AMZN allocating $164.84 billion towards its CapEx, what if it may spend much less on sustaining the logistical community because it’s already constructed? What if AMZN is able to minimize CapEx by $15-$20 billion and determine as a substitute of saving that capital and rising its free money movement [FCF], they will enter into the communication house and allocate $15-$20 billion towards constructing out a communication community? I do not know what AMZN goes to do, however historical past exhibits that AMZN is prepared to spend to win, and if they’re ready to maintain CapEx on the 2022 ranges and reallocate to new tasks, they might turn out to be a powerful competitor within the communication house rapidly.

Fortunately, there isn’t any laborious proof that AMZN goes to enter the communications house. Proper now, AMZN is stating that there are not any present plans in place to enter the communications house, and Maggie Sivon, who’s a spokesperson for AMZN, stated that AMZN doesn’t have plans so as to add wi-fi companies to Prime at present. TMUS additionally got here out and stated that they don’t seem to be in discussions about together with its wi-fi companies right into a Prime bundle, and TMUS is already a Prime companion.

My opinion on whether or not or not Amazon will enter the communication house

Previous to giving my present opinion, I need to say that I’m a shareholder of AMZN, VZ, and AT&T. As of now, I do not consider AMZN will enter the communication house. I do not assume the upside is there until AMZN is prepared to go all the best way. I do not assume a partnership deal is smart, and it might simply be too messy for AMZN to include wi-fi in its prime bundle. This is able to additionally cannibalize whoever is their direct companion, as it might more than likely have a adverse impression on the buyer rely for the main gamers.

The one manner I see this working is that if AMZN was to purchase one of many huge 3, and AT&T would take advantage of sense. AT&T has a market cap of $108.74 billion advert an enterprise worth of $284.39 billion. By buying AT&T and consolidating its debt on AMZN’s steadiness sheet, they acquire an immediate 5G community, a big buyer base, and $16+ billion of annual FCF. This is able to enable AMZN to maintain packages for non-prime members whereas making a Prime bundle that included wi-fi for its Prime members. This additionally would give AMZN a enterprise wireline enterprise that they might embrace within the AWS choices. After I take into consideration the verticals, it’s really attention-grabbing, however I do not assume the FTC or the Federal Authorities would enable AMZN to accumulate AT&T, TMUS, or VZ.

In the end I do not assume it might be an excellent use of AMZN’s capital or time to enter the communications market, until they had been to purchase one of many huge three communications corporations. I do not assume we’ll see Prime Wi-fi, and these stories are simply hypothesis and rumors. I may very well be incorrect, and AMZN could also be denying it for now whereas they work out the main points. For now, I’m not apprehensive, and whereas it’s doable, I do not assume this can be a possible endeavor for AMZN.

Q1 wasn’t what the market wished, however I’m nonetheless very bullish on the long run

On 4/19/23, shares of AT&T closed at $19.70. As soon as Q1 earnings had been launched, AT&T offered off and closed at $17.65 on 4/20/23. Since then, shares continued to say no, closing at $15.67 on 6/6/23. Since 4/19, shares have fallen -20.46%, and they’re quickly approaching the 2022 lows of $14.46. AT&T spooked the market as income missed estimates by -$80 million, subscriber development slowed, and FCF got here in at $1 billion, considerably decrease than the analyst estimates of $2.6 billion.

In search of Alpha

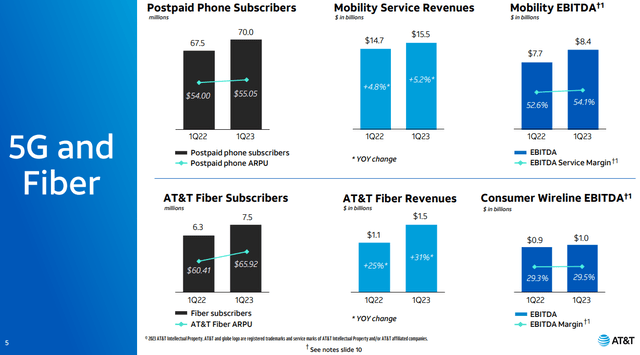

I consider that there are numerous traders who would disagree with me, however I see AT&T as a price play, not a price lure. Simply because AT&T hasn’t been capable of shake the adverse stigma, and it has declined by -42.36% over the previous decade, doesn’t suggest that it’ll stay within the doghouse. AT&T was in a position so as to add 424,000 postpaid cellphone provides, which is now 11 consecutive quarters of including not less than 400,000 internet provides. AT&T additionally added 272,000 Fiber internet provides, and this was the 13th consecutive quarter of including not less than 200,000 internet fiber provides. AT&T is much from a useless firm because it generated $30.1 billion in income for Q1 2023 and is on observe to attain $6+ billion of run-rate value financial savings earlier than 2024.

When taking a look at AT&T’s Q1 2023 metrics on a YoY it is a combined bag. AT&T added 2.5 (3.7%) million postpaid cellphone subscribers YoY. This made its income from mobility improve by 5.44% ($800 million) YoY and its EBITDA from mobility improve by 9.09% ($700 million) YoY. On the fiber aspect, AT&T added 1.2 million subscribers (19.05%) YoY and elevated fiber income by 36.36% ($400 million) and EBITDA from fiber by 11.11% ($100 million). General income YoY elevated by 1.35% ($400 million), whereas its adjusted EPS declined -4.76% to $0.60, and its money generated from operations declined -11.84% (-$900 million) YoY.

AT&T

The elephant within the room was that AT&T generated $1 billion in FCF quite than the $2.6 billion analysts had been searching for. This was addressed on the earnings name, and it nonetheless amazes me how rapidly individuals react and that the market does not really belief that administration can ship. Pascal Desroches (AT&T CFO) particularly addressed AT&T’s FCF and said that the corporate is assured in its full-year outlook of producing in extra of $16 billion FCF for 2023. Capital investments had been $6.4 billion within the quarter, and AT&T had anticipated that Q1’s FCF could be low resulting from seasonal and anticipated working capital impacts. The impacts on FCF got here from the timing of capital investments, system funds, and incentive compensation, which all peaked in Q1.

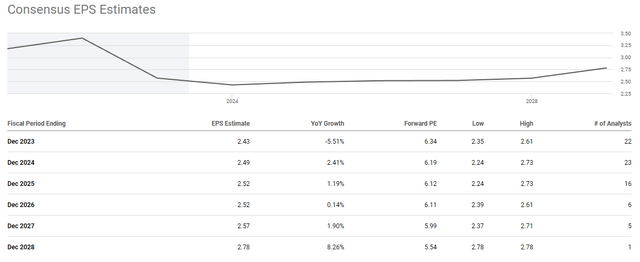

If AT&T does generate $16 billion in FCF, as they’re indicating for 2023, it might put their ahead worth to FCF ratio at 6.79x, which is low. There are 22 analysts who’ve AT&T’s EPS for 2023 pegged at $2.43, which places its ahead P/E ratio at 6.45. For 2024, there are 23 analysts which have AT&T producing $2.49 in EPS, which places their 2024 ahead P/E at 6.29x, and in 2025 there are 16 analysts which have AT&T producing $2.52 in EPS, placing their ahead 2025 P/E at 6.22x.

In search of Alpha

From a valuation standpoint, AT&T may be very low-cost. Sure, it has been a price lure through the years, however these are actual {dollars}, and AT&T generates tens of billions in FCF yearly. Right this moment, primarily based on the TTM numbers, AT&T trades at 8.01x its TTM FCF, in comparison with 9.45x for VZ, and 46.34x for TMUS. TMUS generates half the money from operations, but its FCF a number of is 4.9x bigger than VZ’s and 5.79x bigger than AT&T’s. If I have a look at AT&T from a ahead perspective, primarily based on the $16 billion of FCF that administration says might be delivered, AT&T trades at a ahead worth to FCF a number of of 6.8x. From the TTM to the 2023 annualized FCF, AT&T is projecting there might be 17.86% of FCF development as they add $2.42 billion in FCF over the following 9 months. I do not understand how lengthy it’ll take, however the valuation is simply too low, and sooner or later, AT&T’s share worth ought to be vindicated.

Steven Fiorillo, In search of Alpha

Conclusion

It’s totally powerful to be a shareholder of AT&T because it simply goes down, even WBD simply goes down. I feel the response to the Q1 numbers and the potential of AMZN getting into the communication house are each overdone. AT&T trades at a all-time low valuation at simply 8.01x its present FCF, 6.8x its 2023 projected FCF, and a ahead P/E of 6.45 its 2023 EPS. AMZN denies getting into the communication house, and the transfer strategically does not make a lot sense until they purchase one of many huge three corporations, which is unlikely to happen. AT&T’s dividend yield has crossed the 7% stage, and now might be an excellent time to greenback value common. I consider that finally, shares of AT&T will exceed $20.

{kind=link}