Celsius Holdings (CELH) replace, earnings — insider shopping for this week

Goosehead, PAR Expertise and Galaxy Digital have been unlocked, Lock Field returns have improved… however are additionally trailing a lot worse now, largely as a result of they’ve missed out on a lot of the semiconductor surge this 12 months (aside from our InTEST place, which has joined the “virtually doubled” membership in that portfolio). Which as a minimum reminds us that it’s robust to beat a market cap-weighted index, and tougher nonetheless when momentum shares are doing properly (or when, as I actually did with a number of of those Lock Field positions, you overpay for the unsuitable shares).

I’m holding PAR in my common portfolio, although proceed to consider that we’re “on maintain” and I gained’t be shopping for extra till we see if they will actually create the sustainable software program enterprise that they’ve been promising — it’s getting nearer, however on the identical time that traders are pretty dramatically shedding their persistence with PAR, and with small software program shares typically.

However I don’t assume we have now the expansion to maintain holding PAR within the Lock Field portfolio, and it will likely be helpful to take some extra losses to offset good points, so I’m promoting that one.

Goosehead is an effective story that hasn’t confirmed it could actually compete in a shifting and always-competitive insurance coverage gross sales market. They’ve accomplished some excellent issues, and been by way of a troublesome reorganization that took a pair years, they usually have some actual ambition to construct a platform for on-line insurance coverage comparability buying and promoting, on high of a franchised community of insurance coverage salespeople. It’s admirable that they’ve been in a position to get progress going, at the least just a little bit, regardless of the a lot decrease degree of house gross sales, since house gross sales are their core “new buyer” enterprise and the realtors and mortgage brokers are the supply of most of their leads. And it would work out… however given the competitors within the insurance coverage area, and the robust working surroundings proper now, I don’t assume that Goosehead has the power to construct this enterprise quickly, that will simply take dramatically extra advertising spend than appears prone to come out of this very capital-light and family-controlled enterprise. I just like the company enterprise, and I actually just like the capital-efficient franchise enterprise they’ve constructed on high of that, it had (and doubtless nonetheless has) the potential to work out magically properly… but it surely hasn’t but, and I believe the competitors has gotten a lot better for these core particular person insurance coverage insurance policies (auto and householders), together with the direct-sales competitors from main operators like Progressive, who can spend extra on promoting in every week than Goosehead can generate in gross sales in a 12 months, and I simply assume the percentages of success are a lot decrease now than was my perception 5 years in the past.

Possibly I’m unsuitable, time will inform… however a lot as I’m additionally involved about their potential progress, I would even think about shopping for Lemonade (LMND) over Goosehead as of late, simply because they’ve at the least constructed out a direct gross sales enterprise that has some significant progress, and have begun to layer just a little little bit of rational spending management on high of that.

Galaxy Digital I personal not simply because I wished some cryptocurrency publicity within the Lock Field, however as a result of I assumed they have been well-positioned to be an actual gatekeeper for cryptocurrency funding by establishments. That gatekeeper position has actually develop into a lot much less apparent now, with so many very simple methods to purchase into all the most important cryptocurrencies, so I now not have a number of confidence that Mike Novogratz is constructing one thing which may develop into a “Goldman Sachs of Crypto” sort firm, there simply isn’t a lot proof to assist that right now.

And that’s most simply evidenced by the relative efficiency of Galaxy Digital and Bitcoin since I added Galaxy to the Lock Field. Regardless of the increase of (ultimately) getting that NY itemizing, which got here a lot later than we had anticipated, and regardless of an honest restoration in Bitcoin costs and customarily rising acceptance of Bitcoin as a “actual” asset amongst institutional traders, Galaxy Digital has failed to essentially create shareholder worth… and that’s although their belongings underneath administration have ballooned throughout these 5 years, from simply over $1 billion to greater than $5 billion.

It’s not a horrible firm, it has virtually stored up with Bitcoin by way of the collapse and restoration in the course of the previous 5 years… but it surely’s additionally not worthwhile, and to my eyes it has not confirmed a capability to spend money on nice firms or be an unusually robust asset supervisor throughout the crypto area, so I’ll take my (modest) revenue and go house. It’s most likely nonetheless cheap to have some speculative crypto funding in any type of long-term progress portfolio, so it’s a disgrace that we lack that now, however I don’t see any nice causes to maintain this funding locked up.

In order that’s three extra gross sales from the Lock Field… and sure, I’m additionally potential buys for that portfolio, however none that have been bought this week — I’ll have a brand new Lock Field candidate to speak about quickly.

I’ve written some common feedback about worrying about market valuations this 12 months, as some markets lunge into bubble territory and enthusiasm for the riskiest belongings picks up, and the market booms on… however the causes for warning maintain popping up each week, too. Inflation stays scorching and is usually getting just a little worse, although traders appear very keen to look previous the present struggle and picture the good, clear restoration, with oil costs falling sharply.

Greater residing bills have helped bank card and auto mortgage delinquencies creep steadily upward, with bank card delinquencies specifically virtually again to the extent they hit on the worst of the good monetary disaster, and with auto mortgage delinquencies at new twenty first century highs already (unemployment lingered close to 10% for some time in 2009-2010, so it’s surprising that delinquencies are piling up at comparable or larger charges when unemployment is at 4%, with about 13% of bank card balances and greater than 5% of auto mortgage balances greater than 90 days delinquent… actually reinforcing how overextended the entire nation bought within the wake of COVID and the huge stimulus applications, and the way unprepared all of us have been for the stress of the large spike in inflation that adopted). Persons are maybe not broadly in disaster, mortgage delinquencies stay traditionally low and un-worrisome… however house possession amongst these underneath 50 can be traditionally fairly low proper now, even after it bounced again a bit in the course of the pandemic, earlier than mortgage charges climbed in 2023, and bank card and auto loans really feel like a harbinger of inflation stress.

And the inventory market is in a historic increase — not fairly an all-time bull market, however fairly shut, and the indicators of a possible bubble forming in some extraordinarily standard sectors are in every single place. We’re positively in an “exuberance” stage, pushed largely by enthusiasm for the AI funding cycle, rising protection spending, and the considerably associated area and aerospace increase, although I don’t know if we’ve reached the “irrational exuberance” a part of the cycle simply but.

What do I need to personal in my portfolio? I need to construct a portfolio that compounds in worth over time at a charge meaningfully above inflation, and is extra resilient than the S&P 500 throughout market downturns… and for that, I’m keen to danger a portfolio which may develop lower than the S&P 500 throughout increase occasions (like now), even when that increase would possibly proceed for years earlier than it runs out of steam.

That’s principally simply because we’ve hardly ever by no means seen the market increase like this, and the probability of a reversion to the imply could be very excessive, ultimately. The common complete return of the S&P 500 over the previous ten years is a hair above 15%/12 months now, which isn’t greatest market of the trendy period, that title belongs to the extraordinary market of the late Nineties, when a few the rolling ten 12 months durations generated complete returns of 20%/12 months… but it surely’s getting fairly shut, and the previous six years have offered common annual returns within the 18% neighborhood.

There are few historic parallels to this type of market increase, aside from the tech increase of 1995-2000… and for individuals who are at some extent of their lives the place a 40% market drop would meaningfully reshape their monetary plans (which principally means “anybody inside 5 years of retirement, or in retirement”), that’s doubtlessly worrisome, as a result of the 2000s have been primarily a misplaced decade. Traders who purchased into the S&P 500 in 2000, would have checked out their account in 2010 and seen nearly the identical sum of money they began with.

Everybody over a sure age is aware of that intuitively, I suppose, however shifting household priorities have introduced that into clearer focus for me of late. Which implies that though I do assume that my portfolio is already fairly resilient, I’m not closely chubby the AI story and haven’t double down on probably the most speculative stuff, I made a decision this week to do some rebalancing across the edges. Which means lowering my inventory market publicity just a little bit, starting so as to add some extra non-correlated asset publicity, and boosting my optionality for regardless of the future brings.

Due to the truth that my portfolio has grown extra stock-heavy over time, rebalancing means promoting some positions, both in complete or partially, that I like and would favor to carry. The candidates for culling which come to my consideration most are the shares with significant outperformance which are buying and selling above my “max purchase” value, and, as I look over my portfolio with a extra jaundiced eye, the shares that are providing me “fairness danger,” together with significant danger of decline and everlasting lack of worth, however little or no hope for near-term significant good points. Each of these are judgement calls, however I’m making an attempt to even be just a little bit mechanical in my judgement.

So I sifted by way of these candidates, tried to have a look at them with new eyes, and determined to promote 10% every of half a dozen “profitable” positions which are above my purchase vary, and 100% of the massive place through which I’ve the least confidence. Probably the most rational methods to promote down some positions to generate capital to rebalance are both promoting overvalued positions with robust current efficiency, or promoting positions which have hit cease loss ranges, particularly if my evaluation about any of these firms has turned extra unfavorable… and I’ve successfully accomplished a little bit of each. That clears up sufficient money so as to add some optionality to the portfolio, and in addition to start to construct a place in a properly non-correlated asset class that I hope will develop into significant over time.

This era of reflection has additionally referred to as my consideration to some actually weak efficiency in some mutual fund positions that I’ve principally held and ignored for a really very long time, so there’s additionally been just a little shuffling in that space (extra on that on the finish, for the few who care about that portion of my portfolio).

There are some caveats to all of this, since I didn’t simply undergo and promote 10% of each inventory that sits above my “max purchase” value. And the 2 “exclusions” to that rebalancing, actually, are the 2 main sector exposures that I personal that are already designed to melt market cycles, property & casualty insurance coverage firms and pure assets royalty firms (at the moment, meaning principally gold and oil).

I’m not going to promote any of my property & casualty insurance coverage holdings, as a result of these positions play a essential position in each compounding worth at low beta (usually 1 / 4 to a 3rd much less risky than the market), and providing comparatively non-correlated returns, (since their ups and downs are pushed rather more by climate and rates of interest than by GDP progress, they usually present publicity to well-managed bond portfolios), and that’s roughly 20% of my general portfolio, which is definitely just a little beneath what I’d like (I consider 25% as my common goal). A number of of my P&C shares are above my “max purchase” value, since I prefer to be a cautious purchaser on the subject of these long-term positions that have a tendency to not have main progress spikes (with one actual exception in that group, within the type of Kinsale Capital (KNSL), however I don’t assume that any of them are dramatically overvalued.

Likewise, I’m not promoting any gold publicity, although I most likely gained’t totally train my choices to construct on my gold royalty positions (these will most likely be partially exercised, as we head into expirations for these contracts later this 12 months). Gold royalty firms are about 12% of my fairness portfolio proper now, and gold general, together with each bodily metals and royalty firms, is about 15% of my complete portfolio. I’d possible increase that if we get beneath 10%, and rebalance if we get above 20-25%, which got here near occurring close to the height of the gold and silver costs… however we’re proper within the vary the place I need to be, and most of these positions nonetheless signify fairly compelling long-term worth so long as gold doesn’t fall extra meaningfully from right here (it would, the market remains to be absorbing the large run to $5,500 and has already come down shut to twenty% from that current excessive… but when it does fall extra, most likely a number of different holdings can be doing properly).

And I’m additionally not promoting something that’s model new to the portfolio, added throughout the previous 12 months or so.

There may be additionally some consideration to be made for taxes. If all else is equal, it’s higher to promote worthwhile positions inside my tax-sheltered accounts, and shedding positions inside taxable accounts.

The main points? In any case of that top-down pondering, which I admit might be harmful if over-indulged, I’m promoting to take revenue on 10% of my holdings in every of Alphabet (GOOGL), BWX Applied sciences (BWXT), Keysight (KEYS), Brookfield Corp. (BN), and Shopify (SHOP).

And I’m additionally promoting all of my place in Exor (EXO.AS, EXXRF).

That profit-taking amongst my positions, a few of that are within the top-ten holdings and have wonderful returns, is simply mechanical — I don’t have something unhealthy to say about these firms, past the valuation being past what I’d need to pay, and I anticipate that if the market continues to do properly, these shares may even do properly. And if market valuations fall meaningfully, I’d possible be fairly keen to purchase extra of those identical companies sometime sooner or later. However rebalancing means promoting good things, often, and shopping for stuff that folks like quite a bit much less, so I’ll confess that even doing it across the margins like this can be a little bit painful. Which might be good for me, since I can are usually complacent with long-term holdings.

However Exor is extra of a company-specific sale, so let me go into that in a bit extra element.

Exor (possibly rethink? — present weak point of Ferrari is only a story, and it’ll most likely fade… however possibly not, and a model is actually nothing however a narrative and concerning the feeling that model generates, so it’s disappointing to see a fairly avoidable misstep, with Ferrari releasing an EV that primarily seems like each different EV. Even when that works out OK, the restoration of Stellantis will take longer, and to me it looks as if the hope is now survival, not progress, so possibly I don’t have room for that in my portfolio any extra, not when the market is at traditionally elevated valuations and I’m involved a few comparatively low-return future (sure, if the market crashes, it gained’t simply be the highfliers who come again to earth, the awful performers will most likely crash, too — when individuals promote, they promote the whole lot).

NAV per share for Exor has fallen about 10% simply this 12 months, and there was no indication in any respect that shareholders are displaying any curiosity in shrinking the valuation low cost — I began shopping for Exor about 4 years in the past, and have been working underneath the assumption that it will be honest for this conglomerate to commerce at maybe a 20-25% low cost, given a great historical past of NAV progress, and it was trying fairly near sticking to that degree once I began shopping for… however ongoing weak point in Stellantis, notably, and a transparent insecurity amongst traders that Exor’s going to have the ability to repair that chief or drive significant progress at different main investments like Philips has been sustaining stress on this inventory for a very long time, stress which at this level is just getting worse — the low cost actually bottomed out round 30%, solely briefly getting beneath that, and has usually been extra like 50-60% over the previous 12 months.

Exor’s progress in NAV per share has now dropped to about 9%/12 months in the course of the time I’ve owned shares, and my place is sitting on an annualized lack of about 2%. Looking back, it seems like what occurred is that I used to be tempted by the truth that the low cost had widened going into 2022 (once I purchased), regardless of fairly robust NAV progress underneath present administration (John Elkann took over in 2011), and I assumed each that NAV progress could be good and that the low cost was prone to shrink.

Now, I anticipate the NAV progress will proceed to be weak, given my understanding of the potential for Stellantis, Philips and Ferrari, that are by far their most vital holdings. And I’ve misplaced any confidence that the previous a number of years of additional widening of the low cost goes to show round throughout the subsequent 5-10 years.

I need to maintain this, I like the best way they speak about their investments and I like the concept of outsourcing some persistence to a “generational wealth” asset supervisor… however I can’t say that I like how issues are going for European heavy producers who aren’t within the protection enterprise, and I haven’t seen any indicators of traction on the subject of Elkann making an attempt to show across the faltering efficiency at Stellantis, particularly. In the meantime, Ferrari, the crown jewel of the enterprise (and a holding that’s itself price roughly 80-90% of Exor’s present market cap), is belatedly dealing with not only a PR backlash for his or her newest automobile, but in addition the identical stress as the opposite luxurious names, and I believe I’ll not have the posh of ready them out whereas the NAV is in long-term decline and the low cost is in a long-term pattern of widening.

Possibly it’s simply my age speaking, as I slip into the latter half of my 50s in a pair months, however I discover that underneath the floor, I’ve been shedding confidence in Exor administration really performing strongly sufficient to avoid wasting Stellantis (notably as Chinese language EVs come to dominate Europe), or generate any progress of their different firms (outdoors of the Lingotto asset administration enterprise, which is doing very well — however is just too small to maneuver the needle).

Consideration has continued to come back to Exor from main monetary writers a pair occasions a 12 months, declaring the large low cost and what’s primarily a chance to purchase Ferrari on a budget… however I believe I’ve given it sufficient time, and as I de-risk a number of the portfolio I believe I’ve different locations the place I need to put some long-term capital, with maybe a greater probability of providing me some steadier compounding and/or some higher diversification.

So it’s time to half methods — I had hoped to be proudly owning Exor for many years, however after 4 years I don’t see any of the progress I anticipated, which implies it’s time for me to confess I used to be unsuitable to belief the method with this one. Significantly if I’m seeking to construct in some extra resilience within the portfolio and do some rebalancing. I believe Exor could be very prone to underperform… and, sadly, I believe the massive positions in Ferrari, Stellantis, Philips and CNH are prone to collapse fairly sharply if we have now an actual market crash, since crashes are usually fairly indiscriminate, so it doesn’t even provide that degree of “safety.”

So what am I doing with that money? Nicely, I’m including flexibility, which comes within the taste of a considerably bigger money place that I can put to work as alternatives current themselves (in addition to some extra into my “virtually like money” quick time period bond ETFs)… however I’m additionally going to place a few of that capital to work constructing a place in a low-growth sector that I’ve been pondering of for some time, and couldn’t fairly speak myself into shopping for final week: Timber.

And why am I just a little extra keen to dip my toes right into a timber place than was the case every week in the past, once I began to put in writing to you in some element about Rayonier? A part of that’s the advantage of chewing on the concept for a bit longer and excited about portfolio diversification some extra this week… however I confess that a few of that impetus additionally comes from studying Porter Stansberry’s quick new e-book.

That e-book, titled 2029: The Finish of America : Why the Age of Paper Cash Is Ending And Tips on how to Survive the Coming World Financial Reset, was launched final month as an replace to his long-running “Finish of America” thesis, however can be a meaningfully higher learn, and extra attention-grabbing, than his authentic “Finish of America” work in 2011.

I disagree with Porter’s public feedback and opinions on a number of issues — I’m nowhere close to as libertarian as he’s, and I do know that he’s a lightning rod, principally by design (being a author and writer means you’re incentivized to say excessive and outlandish issues, and that sticks in my craw, which is one cause why I’m not a way more profitable author). Many individuals hate Porter Stansberry, for quite a lot of causes (I’ve talked to him just a few occasions, however don’t actually know him), and that’s OK, you get to have your emotions concerning the particular person or the general public persona. However for my functions, I discover his funding evaluation to often be attention-grabbing, and we do have some widespread floor on that entrance, together with a keenness for utilizing P&C insurance coverage shares as a foundational bulwark for a portfolio, and a want to all the time keep a fairly excessive gold publicity (and favoring gold royalty firms as one of the simplest ways to get some progress out of that place over time).

So I learn the e-book, largely as a result of it was free in my Kindle Limitless account, and the primary half of it was kind of the identical stuff I’ve been studying from Porter on Twitter and in emails over a few years, with a number of commentary about societal and foreign money decline (and an assertion that the previous is attributable to the latter), which is attention-grabbing but in addition closely weighted by his perspective and his historical past of assertive advertising on these matters.

However one of many belongings you be taught after studying dozens of funding promos a day for 20 years, is that hyperbolic commentary which makes your pores and skin crawl and cheap (and even insightful) evaluation can and infrequently do coexist within the thoughts of a pundit… which is why I spend a lot time making an attempt to assist readers sift by way of the advertising of funding concepts and assume as a substitute concerning the concepts themselves.

And I discovered Porter’s the part on timber to be notably attention-grabbing, since I’ve been spending a while on that asset class this 12 months… and, maybe extra importantly, his evaluation gave me some helpful valuation instruments for contemplating how I would need to construct and handle a place in timber shares. (The portfolio development concepts he shares within the e-book are additionally attention-grabbing, together with his interpretation of Harry Brown’s Everlasting Portfolio, one thing he has written about many occasions prior to now, and his concepts about constructing a “honeycomb” of fairness holdings which are designed for non-correlated returns, however these are additionally longer-cycle “maintain your wealth” concepts, usually talking, and lean closely on the mathematics within the case of that “honeycomb,” and I do know traders are often extra fascinated about “construct wealth” concepts, so we’ll go away these apart for now.)

You should purchase the e-book if you happen to’re , the digital version is just 5 bucks (or like me, you will get it free if you happen to’re a Kindle Limitless subscriber), however I’ll share with you just a little little bit of what he stated about timber:

“Timber develop at a charge that doesn’t rely on the Federal Reserve. Yearly, with out exception, in each financial regime, underneath each Fed chair, throughout each struggle and each peace and each increase and each bust, the Douglas firs in Weyerhaeuser’s Washington tract add one other 12 months’s progress to their trunks. A stand of Douglas fir in prime rising years — the sort that dominate Weyerhaeuser’s 11 million acres — places on between 3% and 5% biomass per 12 months. Yearly. The board ft within the firm’s stock develop. Yearly. The stumpage worth, measured in precise lumber, grows. Yearly. A forester calls this progress the organic progress increment. It’s the single most vital idea in timber economics. However what’s much more vital for traders is that this: it has no analog in every other asset class.

“Because of this timberland has been, throughout the final century, the best-performing main asset class in the USA. It has compounded at roughly 13% to 14% nominal per 12 months over the past hundred years — larger than equities, larger than bonds, larger than actual property, larger than gold — with the bottom correlation to any of these different asset lessons. Jeremy Grantham, founding father of GMO and one of many nice long-duration traders of the trendy period, revealed a paper in 2005 displaying that timber had delivered an actual return of roughly 8% per 12 months from 1900 by way of 2005, beating each different institutional asset class over the century. And the reason being not mysterious. The reason being organic. Timber develop. Paper doesn’t. And what gold does for preservation, timber does for compounding.”

I believe it’s fairly unlikely that we’re going to see actual returns averaging 8% from timber within the subsequent 100 years, since actual pricing has most likely risen fairly meaningfull as this has progressively develop into a significant institutional asset class prior to now few many years of that point… but it surely’s attainable. And extra importantly, I believe an actual return is probably going, even given what I anticipate to be fairly significant inflation ache over the subsequent 20 years. Even half of that, 4% per 12 months, could be a significant return if the worth additionally retains up with inflation.

And the particular timber funding he talks about is the largest one, Weyerhaeuser. Right here’s how Porter describes them:

“Because of Weyerhaeuser’s determination to restructure as an actual property funding belief in 2010, there may be now a selected technique for investing in that forest that’s, in my judgment, the one most vital concentrated fairness place an investor could make right now….

“I need you to pause right here and acknowledge what is accessible to you, proper now, that was not accessible to any earlier technology of American traders. You’ll be able to right now, for the value of a single share of inventory — about $24 on the day I’m scripting this — buy a fractional possession curiosity in 11 million acres of American timberland. Actual land. Actual bushes. Actual organic progress. Land that may live on, and bushes that may proceed to develop, it doesn’t matter what occurs in Washington. And the dividend yield on that share, at present costs, is roughly 3.25% — paid quarterly, in actual {dollars}, when you look ahead to the underlying biology to do its work. Frederick Weyerhaeuser paid $6 an acre in 1900. You’ll be able to, as of this writing, purchase an efficient proportionate share of the trendy Weyerhaeuser Firm at a valuation that works out to roughly $2,000 per acre — not low cost in absolute phrases, however properly beneath substitute worth for productive Pacific Northwest timberland, and enormously low cost relative to the organic compounding machine you’re shopping for into.”

However we’ve talked about timber REITs earlier than, and also you principally know that — the explanation this part of his e-book caught with me was Porter’s easy approach to assess purchase/promote ranges for the corporate:

“I’m not telling you to purchase Weyerhaeuser inventory indiscriminately at any value. I’m telling you that Weyerhaeuser, on the proper value, is the one most tasty long-duration holding I do know of within the public fairness markets….

“Weyerhaeuser’s inventory value cycles — meaningfully, usually, predictably — round its underlying e-book worth. The e-book worth itself is inconspicuous, as a result of the REIT’s timberland is carried at historic price slightly than at market worth, and the market worth of American timberland has risen considerably over the past twenty years. However even permitting for that understatement, the inventory’s price-to-book ratio fluctuates in repeatable patterns, increasing throughout housing booms when lumber demand is powerful and contracting throughout housing busts when lumber demand is weak. The rationale this cycle is exploitable is that it has virtually nothing to do with the long-term worth of the asset.

“A stand of Douglas fir doesn’t care whether or not single-family housing begins in a given quarter have been 1.1 million or 1.5 million. It is going to be there subsequent quarter, and subsequent 12 months, and subsequent decade, rising at its personal organic tempo. However the market — which in its short-term temper swings is ruled by quarterly earnings slightly than century-long biomass accumulation — punishes Weyerhaeuser’s inventory throughout housing downturns as if the underlying forest have been evaporating. However it’s not evaporating. It’s rising.

“The suitable method, subsequently, is to construct a cycle-aware place. You need to accumulate shares when the price-to-book ratio is within the decrease quartile of its historic vary — that’s, when the market has given up on housing and is providing you the forest at a reduction to substitute worth. You need to maintain these shares by way of the total cycle, accumulating the dividend alongside the best way, and also you need to trim or promote when the price-to-book ratio is within the higher quartile of its historic vary — that’s, when the market has quickly fallen in love with housing and is providing you a premium to substitute worth for a similar forest.”

OK, so what sort of returns does he say that will have generated?

“Over the interval from January 2011 by way of April 2026 — all the 15 years since Weyerhaeuser’s REIT conversion — a disciplined cycle-aware method to this single inventory has delivered roughly 20% annualized returns towards the S&P 500’s roughly 14% annualized returns over the identical interval. That’s roughly 600 foundation factors of annual outperformance from a single holding, generated not by way of intelligent buying and selling or inside info however by way of the easy self-discipline of shopping for organic belongings at a reduction and promoting them at a premium.”

We are able to quibble with the information just a little, since WY introduced its intention to transform to a REIT in December of 2009, and really transformed in 2010, with the conversion retroactive to January 1, 2010 for tax functions, and with a giant particular dividend (paid in inventory) to make that conversion attainable… however that solely actually makes a distinction as a result of the valuation shifted fairly sharply throughout that first 12 months of conversion, which is cleaned out by the averages, to a big diploma, within the fullness of time.

For our functions, and utilizing knowledge going again 25 years, these common pointers would have us shopping for when WY is beneath 1.85X e-book worth and promoting when it’s above 2.75X e-book worth. Which strikes me as a wise technique, largely as a result of it’s simple to handle.

E-book worth per share at WY is $13.09, as of March 31. So right now, it’s possibly not totally into “distressed” territory, however within the $24-25 vary the inventory is fairly near the highest of that “buyable” vary of lowest-quartile valuation, at about 1.85X e-book worth. There’s nothing magical to that ~1.85X e-book quantity — If we use the 2010-present timeframe as a substitute, the proper cutoff is perhaps 1.7X e-book… and if you happen to return additional, say, 30 years, to seize the late Nineties decline in timber values, then the underside quartile is perhaps decrease nonetheless, one thing extra like 1.5X e-book. The highest quartile equally fluctuates a bit, relying in your timeframe.

However I’m fairly comfy with utilizing newer historical past, notably as a result of timber has develop into a extra mainstream funding in current many years and is usually depressed proper now due to low homebuilding exercise, and since REITs virtually all the time commerce at larger value/e-book valuations than in any other case comparable working firms, largely as a result of they pay out larger dividends (which takes away from e-book worth compounding, all else being equal), and simply due to their extra engaging tax standing.

So I’ll simplify that, and say that we will fairly plan to purchase WY beneath 1.9X e-book worth, with a choice for a value a bit decrease, we’ll say beneath 1.7X e-book… and promote someplace above 2.8X e-book, which is roughly the highest quartile of the valuation vary and has traditionally indicated “cyclical peaks,” usually pushed by robust housing begins. With the intention of proudly owning the inventory more often than not, reinvesting dividends so long as it’s beneath that 2.8X e-book degree, and having the self-discipline, after we promote throughout a comparatively overvalued interval, to purchase again in throughout that subsequent dip.

That places our “max purchase” value at ~$24.87… so we’re simply barely within the “we will begin shopping for” neighborhood right now. Over the previous 12 months, WY has dipped down into the $20-22 vary just a few occasions, so we’ll most likely see a shopping for alternative in some unspecified time in the future beneath 1.7X e-book worth (right now, that will be $22.25). These numbers are usually not carved in stone, and you may tweak them to give you a distinct vary… however I do assume it’s vital to have some self-discipline, notably for a inventory that could be very unlikely to ever put up dramatic progress numbers.

What if we did the identical math for Rayonier (RYN)? It’s a bit completely different as an organization, principally as a result of they’ve traditionally been rather more targeted on simply promoting uncooked timber and fewer on processing that timber, although that’s altering with the addition of PotlatchDeltic. It’s additionally a considerably completely different portfolio, with most likely completely different land values to a point.

How else do these firms and their portfolios differ? Rayonier has about 23% of its timberland within the Pacific Northwest, however that land is usually in Idaho, and is not as traditionally useful as Weyerhaueser’s land in Washington and Oregon, on the Pacific aspect of the mountains (for good cause, bushes develop quicker within the temperate areas nearer to the coast than they do within the larger elevations in Idaho)… although Rayonier owns some land within the higher areas, too, and their bigger Idaho portfolio, like WY’s northern timber land, remains to be extra useful than the southern timberlands, usually talking — they’re nonetheless principally harvesting species like Douglas Fir that carry a better worth than southern softwoods, have an extended progress cycle, and are used primarily for lumber, they only don’t develop as quick or massive because the closer-to-the-coast variations.

Weyerhauser, like Rayonier, additionally has most of its timber land within the South, unfold from Arkansas to Florida, and that’s additionally the place a lot of the “Greater and Higher Use” land gross sales can goose returns a bit, principally resulting from photo voltaic and housing demand (although WY additionally has a great variety of quarries on its land, which is an attention-grabbing little increase for royalty income from combination, despite the fact that it’s not notably a giant enterprise, they worth these “mineral rights” at about $175 million and it most likely solely caught my eye due to our possession of Amrize, which has me excited about quarries).

However for WY, that “southern publicity” is just about 60%, and it does have extra publicity to northern forests. Weyerhaueser has 2.5 million of its 10.4 million acres within the Pacific Northwest, in order that’s just like RYN’s 23% in Idaho and Washington, and it additionally owns one other (virtually) million acres in New England, principally in Maine, together with a bit in West Virginia.

For RYN, the mathematics works out to place their lowest value/e-book quartile at beneath about 1.4X e-book, and the best quartile at 1.9-2X e-book. If we limit that to only the interval throughout which RYN has been a REIT, beginning in 2004, then the numbers would transfer to about 1.5X and a couple of.2X, that means that if we port over Porter’s WY technique we’d purchase beneath 1.5X e-book and promote above 2.2X e-book. Rayonier has a e-book worth per share of $17.67 as of final quarter, which does embrace the PotlatchDeltic belongings (and better share rely), so that will imply shopping for beneath $26.50. That’s our “Max purchase” degree, and for “most popular purchase” we’ll hope for just a little greater low cost, 1.3X e-book, which might be $23. We’re properly beneath that right now, because of an absence of curiosity within the inventory after their massive merger replace and, almost definitely, some concern concerning the persevering with weak point in housing and worries about larger rates of interest, which implies that going by present e-book worth, Rayonier is not only cheaper than Weyerhaueser proper now, but in addition cheaper than it has ever been, even when we return to the pre-REIT days within the Nineties.

Right here’s the historic value/e-book valuation chart for each of those surviving timber REITs — be aware that they each went by way of massive modifications within the comparatively current previous, with Rayonier spinning off its superior supplies enterprise in 2014 and Weyerhaueser changing to a REIT in 2010. (You can even see that RYN bought a carry once they transformed to REIT standing, in 2004)

Once more, that’s going by e-book worth, and we all know that’s most unlikely to be very near the true worth of their timberland belongings, since that land is carried on the e-book at buy value and in addition depreciated over time.

Altogether, Weyerhauser values its timber land at price, minus depreciation, of about $11 billion. In the event that they have been to promote it to a timber investor, that will possible be price rather more — most likely a median of $1,800-2,000/acre for the southern stuff and the Maine land (totaling virtually $14 billion at $1,800/acre), and fairly probably extra like $4,000/acre within the Pacific Northwest (totaling $10 billion). Take these values and subtract $5.5 billion in debt, and also you get to $18.5 billion… which is fairly near the market cap of $17.7 billion, and we’re not giving them any worth for his or her giant wooden merchandise enterprise or any “HBU” potential from their land.

So WY might not be at traditionally extreme-low valuations, but it surely’s fairly simple to justify shopping for the inventory close to the present degree, at a few 5% low cost to the possible internet worth of their timberland, ignoring the vertically built-in wooden merchandise enterprise they’ve constructed on high of that, which generates a great chunk of their earnings (they’re the most important or one of many couple largest producers in each lumber and engineered wooden merchandise within the nation, and in addition distribute these merchandise in main homebuilding areas, so that they profit from each scale and vertical integration), and ignoring their giant leases in Canada.

And, in fact, the purpose is to get publicity to the organic progress of timber, and to the tendency of productive timber land to carry its worth over generations, which implies it ought to usually at the least sustain with inflation and in addition share the worth they get from harvesting and processing that timber with shareholders, largely within the type of these annual dividends. Weyerhaeuser modified its dividend coverage in 2020, transferring to a “common plus interim” technique, so the bottom dividend has grown slowly, from 17 cents/quarter in 2021 to 21 cents, the place it has been for just a little over a 12 months, and once they have surplus money (they purpose to distribute 75-80% of their “adjusted funds accessible for distribution”), they both pay a supplemental dividend, which they final did in early 2024 (with a lot bigger ones in 2022 and 2023), or they purchase again inventory. They’ve decreased the share rely by 4-5% because the REIT conversion, so that is sluggish… however sluggish and opportunistic is OK.

I might anticipate the dividend to most likely be unchanged till housing begins decide again up, which should result in sufficient demand progress to generate some further money movement, however we’ll see, they did constantly increase the dividend by a 4 cents a 12 months every year (roughly 5% growht, on common), till they let it sit flat over the previous 12 months… and, in fact, I don’t know when the subsequent dividend enhance would possibly come. All I do know is that extra individuals need to purchase houses and there aren’t sufficient of them to go round, and new houses are the largest marketplace for WY’s lumber and wooden merchandise (about 2/3 of gross sales over the previous 5 years), so residential development ought to decide up in some unspecified time in the future once more. And the historical past of money returns is fairly robust, with WY returning a complete of greater than $6 billion to shareholders over the previous 5 years (mixed dividends and buybacks), so there may be some snapback potential if traders ultimately see a pathway to dividend progress rising.

Like Rayonier, most of Weyerhaueser’s land is within the South, roughly 6.5 million acres, however they’re extra diversified and, because of a a lot bigger wooden processing enterprise, with a number of sawmills and wooden merchandise services and distribution facilities, they get greater than half of their income from the West. And I haven’t talked about {that a} fairly good chunk of that’s from land they don’t personal, which makes it rather less attention-grabbing however remains to be a contributor of worth — Weyerhaueser has timber administration leases on thousands and thousands of acres of presidency land in Canada, which isn’t seen as tremendous useful proper now, partially due to low housing begins and partially due to larger tariffs on lumber imports within the US, but it surely would possibly generate some good money movement at occasions (they bought their BC leases final 12 months, however nonetheless maintain leases in Alberta, Saskatchewan and Ontario, and function a pair mills in that nation).

That very same math for “present land worth” for Rayonier would give us 930,000 acres in Idaho and Washington, and we most likely give {that a} haircut relative to the WY land in that area however let’s name it $3,000/acre. That’s $2.8 billion. The three.2 million souther acres, at $1,800/acre, could be $5.8 billion. So our complete is $8.6 billion — subtract $1.38 billion in debt, and that’s a present worth, timber land alone, of $7.2 billion. The market cap is about $6.4 billion right now — so, once more, not a “disaster” valuation, however some margin of security in there, and an affordable valuation from which to anticipate some long-term appreciation, once more with out giving them credit score for his or her housing developments or HBU land gross sales or their lumber processing capability, despite the fact that that’s much less vital for RYN than it’s for WY… and, in fact, it’s a smaller firm that simply went by way of a giant merger, so we’d prefer to assume there’s some alternative to develop into just a little extra environment friendly, and for RYN to possibly get some credit score for that bigger land place within the northwest that got here from PotlatchDeltic, and it already pays a considerably larger dividend than WY, which is its solely actual near-peer within the public markets.

So I’m going to purchase a really small place in Weyerhaueser, actually simply to get myself excited about it extra and to place that “max purchase” of 1.9X e-book worth into the portfolio so it catches my consideration. And I’m going to go in a bit greater with a purchase order of Rayonier (RYN). Given the relative valuation enchantment of the 2, I’d prefer to construct this as a 2/3 RYN, 1/3 WY place, totaling 5% of my portfolio (so roughly 3.3% RYN/1.7% WY), however we’re not going to get there in a single week — I’ll tentatively plan to construct this out roughly in thirds, so we’ll begin with 1.1% in RYN, and I’ll look ahead to that WY valuation to get extra interesting however will maintain to that “thirds” concept simply to make this method simpler to observe, in order that’s simply over 0.5%. These are usually not high-growth tales, they usually actually solely have the potential to have a significant diversification and compounding impression on my portfolio in the event that they’re of significant measurement, so even this “begin with 1/3” buy makes this a bigger dedication to timber than I might sometimes make as an “entry” purchase for extra speculative or growth-driven investments, the place I’d often begin out at 0.5-1%.

Right here’s a bit extra from Porter’s argument that I discovered attention-grabbing:

“Gold and timber are the 2 best-performing actual belongings of the trendy period. And here’s what is even higher: they’re the 2 belongings with the bottom correlation to one another. Gold rises when greenback credit score expands. Timber rises when housing and industrial manufacturing develop. Gold protects you within the monetary-debasement quadrant of the disaster. Timber protects you within the productive-scarcity quadrant. Over the past 50 years, the correlation between gold and timber has been virtually precisely zero. They transfer independently, they usually shine in several phases of the credit score cycle. That’s not a coincidence. It’s a structural function of what every asset is. Gold is a financial hedge. It costs the inventory of dollar-denominated guarantees. Timber is a real-economy compounding engine. It costs the demand for bodily shelter and bodily items in a rising financial system. A portfolio that holds each holds two of probably the most potent diversifying devices accessible to traders.”

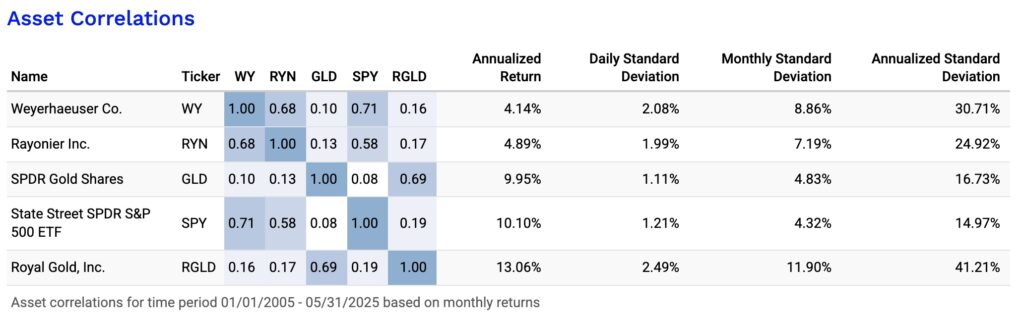

Even for the publicly traded shares, that appears to nonetheless be largely true over time — that is the matrix of correlations for the previous 20 years, and you may see that each RY and RYN have low correlation (0.1-0.13) to GLD, and equally low correlation with RGLD, the one gold royalty firm that has been publicly traded for that lengthy. Curiously, WY is as correlated with RYN as it’s to the S&P 500, and RYN is much less correlated with the S&P 500 — most likely largely as a result of WY has extra of an industrial enterprise on high of its timberland, with main lumber manufacturing and distribution.

Appears smart to personal each. I believe Rayonier is extra attractively valued and has a better yield, with some significant potential to enhance effectivity a bit from the added scale of the still-fresh PotlatchDeltic acquisition, and with a barely stronger give attention to “HBU” land gross sales and housing improvement… however Weyerhaueser has extra leverage to lumber, which is usually extra useful than pulp, with some further capability from Canada on long-term leases, and their timber land ought to be at the least just a little extra useful than Rayonier’s, due principally to effectivity of scale and the larger place on the West Coast. And it’s good that the 2 are usually not completely correlated with one another, which provides us an excuse to diversify a bit throughout the timber sector, amongst what are actually successfully the one publicly-traded North American choices (there are main timber firms all through the world, together with some with giant holdings in Northern Europe and Asia, however I don’t perceive them as properly… they usually’re additionally virtually all actually producers of paper, packaging, or lumber to extra of a level than they’re stewards of timberland, and infrequently have significant investments in different companies, just like the Japanese “timber” firms who’re shopping for out US homebuilders of late).

So to a point, Porter has satisfied me to focus rather less on the efficiency of those two timber REITs as shares over the previous couple many years, and extra on the embedded worth of their timber belongings, as a useful diversifying device at any time when the subsequent disaster occurs to hit. That’s most unlikely to provide my portfolio a greater common return over the subsequent 12 months or two, however I believe the valuations of the timber REITs are at the least usually cheap now, and I like the concept of monitoring them and managing these holdings based mostly on their relative value/e-book worth over time, as they get standard or unpopular — right now, they’re traditionally fairly unpopular, and that looks as if an affordable sign to cease overthinking it, as I’ve been doing for the previous few weeks, and simply begin to purchase (I solely burdened you with that overthinking as soon as, final week, so you’re welcome for that :))

Deleted: Vanguard Dividend Progress (VDIGX) has actually been struggling lately, after the departure of longtime supervisor Don Kilbride the fund has did not take part in a lot of the market’s return whereas additionally, due to enormous positions in Microsoft, Broadcom, Eli Lilly, Apple and different massively profitable and generall costly megacap shares, possible dealing with most of the identical draw back dangers as the general market. I’ve begun easing a few of my accounts out of VDIGX, and into the (traditionally) extra aggressive Vanguard Primecap Core (VPCCX), which has each stronger long-term efficiency and, I believe, a greater portfolio make-up for the present surroundings. I make that change partly as a result of VPCCX is the fund I might have chosen when constructing these portfolios a few years in the past, but it surely wasn’t open at the moment (it reopened in 2024, this isn’t model new however I have a tendency to maneuver slowly inside my fund portfolios). That’s a rise to portfolio danger, on the margins, so I’ll possible leaven that with another comparatively minor changes, together with just a little discount in my holdings in Primecap Progress (POGRX), which has similarities to VPCCX, in a few of my tax-advantaged accounts.

Deleted: This problem at a number of the Wellington-managed funds at Vanguard will not be model new — Vanguard Dividend Progress and Vanguard Well being Care have each underperformed lately, after doing very properly for a really very long time underneath completely different administration groups. Vanguard Well being Care nonetheless provides my portfolio some significant diversification, since I don’t have a lot well being care publicity or sector experience, so I’ll proceed to be a bit extra affected person with that one, but it surely’s additionally a a lot smaller fund place for me, and it has kind of stored up with the (depressed) sector prior to now couple years, if we give them just a little credit score for his or her international diversification.

I’ve additionally added some publicity to the Cambria Rising Shareholder Yield ETF (EYLD), which is a shareholder yield-weighted fund of rising markets shares — in follow, meaning it’s a method to purchase into cash-generating and principally smaller firms in rising markets, with out the large weighting that almost all rising markets ETFs should the huge expertise leaders of Taiwan and South Korea. I don’t have something notably towards the wildly robust reminiscence and chipmaking companies that dominate these indices, however I don’t assume the world’s largest makers of semiconductors and laptop reminiscence are “rising market” positions that supply us diversification from the AI-focused tech increase, they’re simply elements of that increase which occur to be domiciled in different international locations.

I’ll additionally scooch a bit extra of that surplus money into LDRH and LDRI, which I like partially as a result of they’re very liquid whereas avoiding a number of the maturity dangers of ETFs, they usually roll these five-year ladders routinely, which provides them a median maturity of just a little over two years… but in addition as a result of despite the fact that they don’t have excessive quick ratios, they appear to draw quick sellers to sufficient of a level (particularly LDRI), that my holdings have usually been boosted by quick lending charges, which elevated my yield on these ETFs over the previous 12 months by near 50%. You can even do bond ladders your self of any period, both utilizing particular person maturity ETFs (which is what these ETFs use) or particular person bonds, however I discover this short-term answer a LOT simpler for my “just a little higher return than money, just a little extra rate of interest danger” investments in what are successfully short-term bond funds. I used to place some capital into constructing my very own shorter-term T-Invoice and Treasury Notes ladder, however these ETFs are a a lot simpler method.

The place has that yield increase come from? I take part within the lending applications at each of my main brokers, Constancy and Interactive Brokers — which implies I authorize them to lend out my shares to any quick vendor who desires them, and I earn a share of the every day curiosity earnings acquired for these loans (Constancy pays out 60% of the market lending charge for that safety, IBKR 50%). That’s often not an enormous sum of money, and it’s usually zero in any given month… however when these shares are lent, I reinvest the proceeds, and that’s why these positions present up with comparatively excessive returns, in extra of their acknowledged yield.

Right this moment, the acknowledged yield is within the vary of 6.5% for LDRH and three.5% for LDRI, however my annualized returns have been roughly 8.5% and 10.5%, respectively, since I began constructing positions in these ETFs 15 months in the past, principally as a result of there has at occasions been strong demand for borrowing LDRI shares, and it doesn’t take a lot to supply just a little increase, even having the shares borrowed for just a few days a month is significant. That earnings is a bonus, some months there may be little or no borrowing towards my portfolio, some months there’s fairly a bit, however, whereas I allow all of my holdings to be lent out, most of that lending sometimes comes from my ETF positions. I heartily advocate collaborating within the lending program in case your dealer permits it. I consider that quick promoting is a vital a part of a wholesome market, so it doesn’t hassle me that I’m “letting” the shorts entry my shares, and I additionally consider that this train is basically risk-free… and that is additionally a cause, in case you want one, to restrict your use of margin leverage (ie, borrowing cash out of your dealer to purchase inventory) — if you happen to personal shares on margin, the dealer can lend them out at their whim, you don’t get to determine since you don’t totally personal them, and also you gained’t obtain any of the proceeds.

(Concerning danger of lending: you continue to have full financial rights to the securities you lent out, together with the receipt of money in lieu of any dividends these shares obtain, and you may promote at any time — however do be aware that though the financial earnings from lent shares is similar, the taxation can differ just a little, together with that the money you obtain in lieu of dividends is taxed as earnings, so it doesn’t profit from any decrease “certified” dividend charge you would possibly in any other case pay. A lot of my “lent” securities are in tax-deferred accounts, and for those that aren’t the tax distinction isn’t sufficient to offset the worth of the additional earnings).

{kind=link}