Revealed on Could sixth, 2026 by Bob Ciura

The U.S. inventory market, as measured by the S&P 500 Index, is essentially the most well-known on this planet.

Nevertheless, there are good causes for traders to look outdoors the U.S., significantly these in search of earnings.

However earnings traders ought to grow to be aware of the key European inventory indices:

- FTSE 100: The 100 greatest market cap corporations within the U.Okay.

- DAX: 40 of Germany’s greatest blue chip shares

- CAC 40: 40 most vital shares among the many 100 largest market caps on the Euronext Paris

There are numerous high quality, blue-chip companies with excessive dividends which might be situated outdoors the US.

With that in thoughts, now we have created a free listing of over 200 excessive dividend shares with dividend yields above 5%.

You may obtain your copy of the excessive dividend shares listing under:

Worldwide dividend shares with greater yields than their U.S.-based friends could also be enticing for earnings traders.

This text will rank the ten highest-yielding European dividend shares within the Certain Evaluation Analysis Database.

Desk of Contents

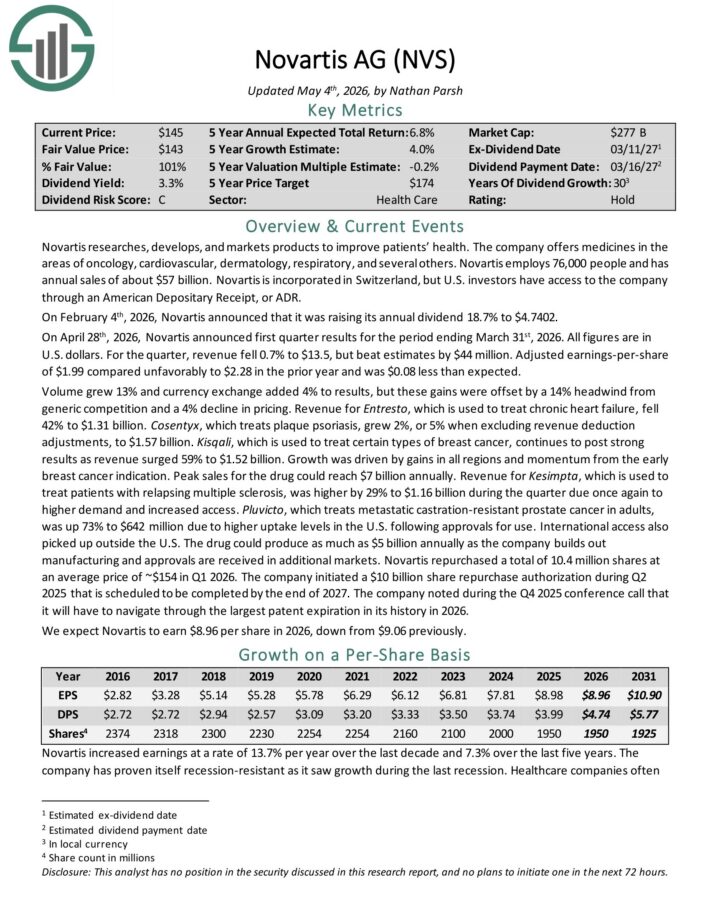

Excessive Yield European Inventory #10: Novartis AG (NVS)

Novartis researches, develops, and markets merchandise to enhance sufferers’ well being. The corporate presents medicines within the areas of oncology, cardiovascular, dermatology, respiratory, and several other others.

Novartis employs 76,000 individuals and has annual gross sales of about $57 billion. Novartis is included in Switzerland, however U.S. traders have entry to the corporate via an American Depositary Receipt, or ADR.

On February 4th, 2026, Novartis raised its annual dividend 18.7% to $4.7402.

On April twenty eighth, 2026, Novartis introduced first quarter outcomes for the interval ending March thirty first, 2026. All figures are in U.S. {dollars}. For the quarter, income fell 0.7% to $13.5, however beat estimates by $44 million.

Adjusted earnings-per-share of $1.99 in contrast unfavorably to $2.28 within the prior 12 months and was $0.08 lower than anticipated.

Quantity grew 13% and forex change added 4% to outcomes, however these features have been offset by a 14% headwind from generic competitors and a 4% decline in pricing.

Income for Entresto, which is used to deal with persistent coronary heart failure, fell 42% to $1.31 billion. Cosentyx, which treats plaque psoriasis, grew 2%, or 5% when excluding income deduction changes, to $1.57 billion.

Kisqali, which is used to deal with sure varieties of breast most cancers, continues to submit robust outcomes as income surged 59% to $1.52 billion.

Novartis repurchased a complete of 10.4 million shares at a mean value of ~$154 in Q1 2026. The corporate initiated a $10 billion share repurchase authorization throughout Q2 2025 that’s scheduled to be accomplished by the top of 2027.

The corporate famous in the course of the This autumn 2025 convention name that it should navigate via the biggest patent expiration in its historical past in 2026.

We anticipate Novartis to earn $8.96 per share in 2026, down from $9.06 beforehand.

Click on right here to obtain our most up-to-date Certain Evaluation report on NVS (preview of web page 1 of three proven under):

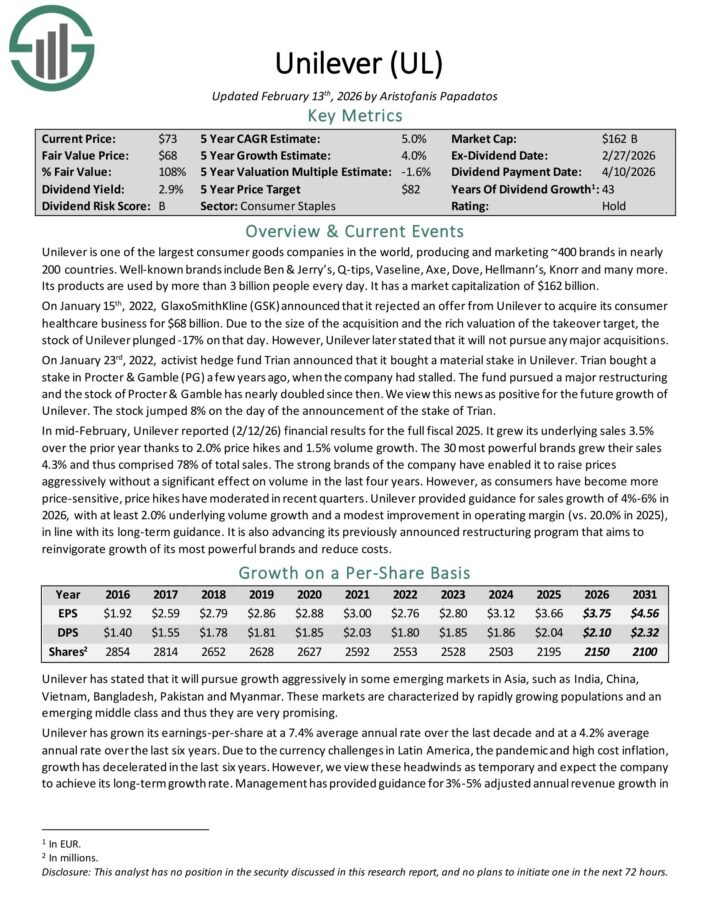

Excessive Yield European Inventory #9: Unilever plc (UL)

Unilever is without doubt one of the largest shopper items corporations on this planet, producing and advertising and marketing ~400 manufacturers in almost 200 nations.

Properly-known manufacturers embrace Ben & Jerry’s, Q-tips, Vaseline, Axe, Dove, Hellmann’s, Knorr and lots of extra. Its merchandise are utilized by greater than 3 billion individuals each day.

In mid-February, Unilever reported (2/12/26) monetary outcomes for the total fiscal 2025. It grew its underlying gross sales 3.5% over the prior 12 months because of 2.0% value hikes and 1.5% quantity progress.

The 30 strongest manufacturers grew their gross sales 4.3% and comprised 78% of whole gross sales. The robust manufacturers of the corporate have enabled it to lift costs aggressively and not using a important impact on quantity within the final 4 years.

Nevertheless, as shoppers have grow to be extra price-sensitive, value hikes have moderated in latest quarters.

Unilever supplied steering for gross sales progress of 4%-6% in 2026, with at the least 2.0% underlying quantity progress and a modest enchancment in working margin (vs. 20.0% in 2025), according to its long-term steering.

Unilever has a major aggressive benefit, particularly the power of its manufacturers. The corporate generates ~80% of its gross sales from the #1 or #2 place in its markets.

Consequently, Unilever has been capable of increase its dividend for 43 consecutive years in Euros.

Click on right here to obtain our most up-to-date Certain Evaluation report on UL (preview of web page 1 of three proven under):

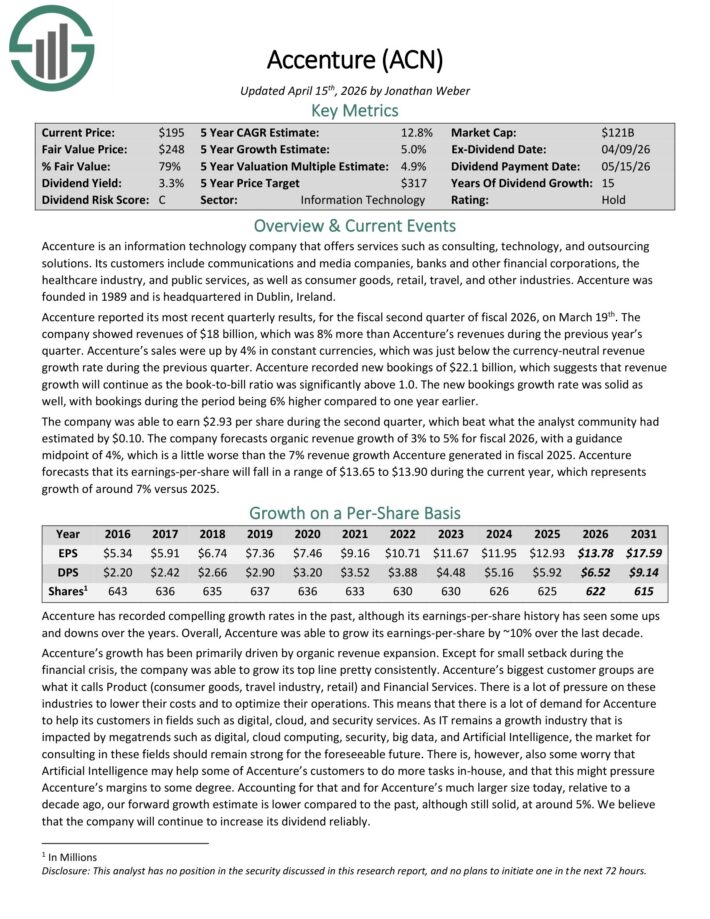

Excessive Yield European Inventory #8: Accenture plc (ACN)

Accenture is an info expertise firm that provides companies reminiscent of consulting, expertise, and outsourcing options.

Its clients embrace communications and media corporations, banks and different monetary firms, the healthcare business, and public companies, in addition to shopper items, retail, journey, and different industries.

Accenture reported its most up-to-date quarterly outcomes, for the fiscal second quarter of fiscal 2026, on March nineteenth. The corporate confirmed revenues of $18 billion, up 8% from the earlier 12 months’s quarter.

Accenture’s gross sales have been up by 4% in fixed currencies, which was slightly below the currency-neutral income progress charge in the course of the earlier quarter.

Accenture recorded new bookings of $22.1 billion, which means that income progress will proceed because the book-to-bill ratio was considerably above 1.0.

The brand new bookings progress charge was stable as properly, with bookings in the course of the interval being 6% greater in comparison with one 12 months earlier.

The corporate was capable of earn $2.93 per share in the course of the second quarter, which beat what the analyst group had estimated by $0.10.

It forecasts natural income progress of three% to five% for fiscal 2026, with a steering midpoint of 4%.

Click on right here to obtain our most up-to-date Certain Evaluation report on ACN (preview of web page 1 of three proven under):

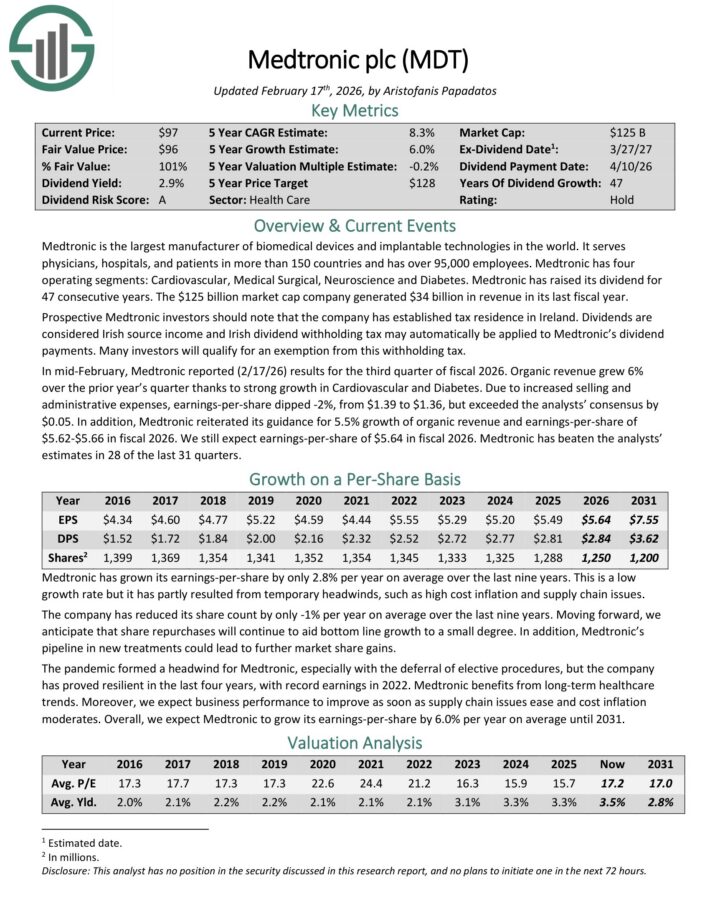

Excessive Yield European Inventory #7: Medtronic plc (MDT)

Medtronic is the biggest producer of biomedical gadgets and implantable applied sciences on this planet.

It serves physicians, hospitals, and sufferers in additional than 150 nations and has over 95,000 staff. Medtronic has 4 working segments: Cardiovascular, Medical Surgical, Neuroscience and Diabetes.

The corporate generated $34 billion in income in its final fiscal 12 months.

In mid-February, Medtronic reported (2/17/26) outcomes for the third quarter of fiscal 2026. Natural income grew 6% over the prior 12 months’s quarter because of robust progress in Cardiovascular and Diabetes.

Resulting from elevated promoting and administrative bills, earnings-per-share dipped -2%, from $1.39 to $1.36, however exceeded the analysts’ consensus by $0.05.

As well as, Medtronic reiterated its steering for five.5% progress of natural income and earnings-per-share of $5.62-$5.66 in fiscal 2026.

Medtronic has raised its dividend for 47 consecutive years. It has grown its dividend by 9.7% per 12 months on common during the last decade and by 5.6% per 12 months on common during the last 5 years.

Click on right here to obtain our most up-to-date Certain Evaluation report on MDT (preview of web page 1 of three proven under):

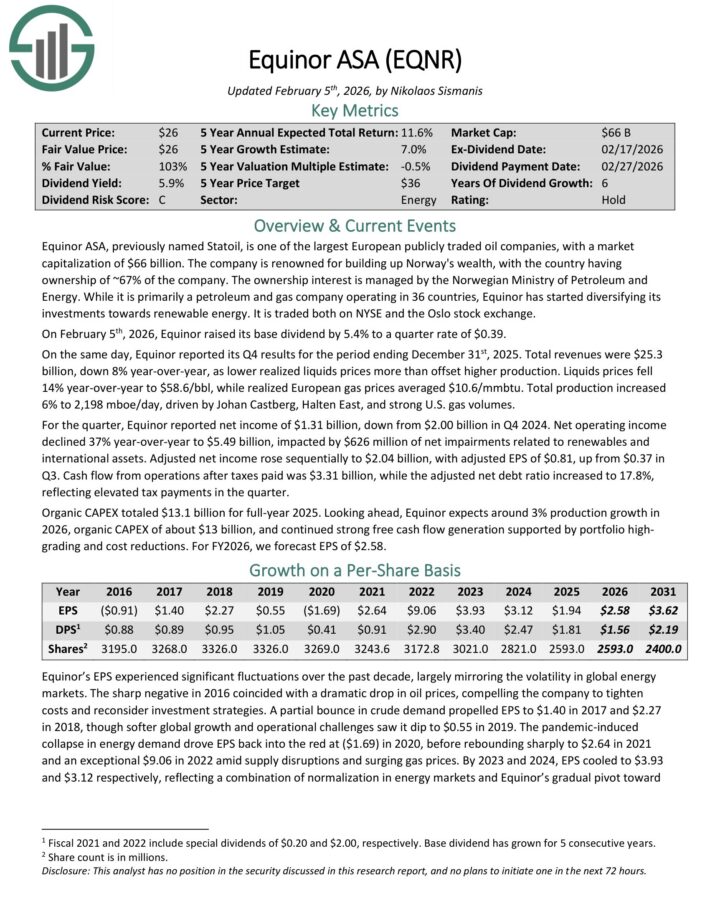

Excessive Yield European Inventory #6: Equinor ASA (EQNR)

Equinor ASA is without doubt one of the largest European publicly traded oil corporations.

The corporate is famend for increase Norway’s wealth, with the nation having possession of ~67% of the corporate. The possession curiosity is managed by the Norwegian Ministry of Petroleum and Vitality.

Whereas it’s primarily a petroleum and fuel firm working in 36 nations, Equinor has began diversifying its investments in direction of renewable vitality. It’s traded each on NYSE and the Oslo inventory change.

On February fifth, 2026, Equinor raised its base dividend by 5.4% to 1 / 4 charge of $0.39.

On the identical day, Equinor reported its This autumn outcomes for the interval ending December thirty first, 2025. Complete income was $25.3

billion, down 8% year-over-year, as decrease realized liquids costs greater than offset greater manufacturing.

Liquids costs fell 14% year-over-year to $58.6/bbl, whereas realized European fuel costs averaged $10.6/mmbtu.

Complete manufacturing elevated 6% to 2,198 mboe/day, pushed by Johan Castberg, Halten East, and powerful U.S. fuel volumes.

For the quarter, Equinor reported web earnings of $1.31 billion, down from $2.00 billion in This autumn 2024. Web working earnings declined 37% year-over-year to $5.49 billion, impacted by $626 million of web impairments associated to renewables and worldwide property.

For FY2026, we forecast EPS of $2.58.

Click on right here to obtain our most up-to-date Certain Evaluation report on EQNR (preview of web page 1 of three proven under):

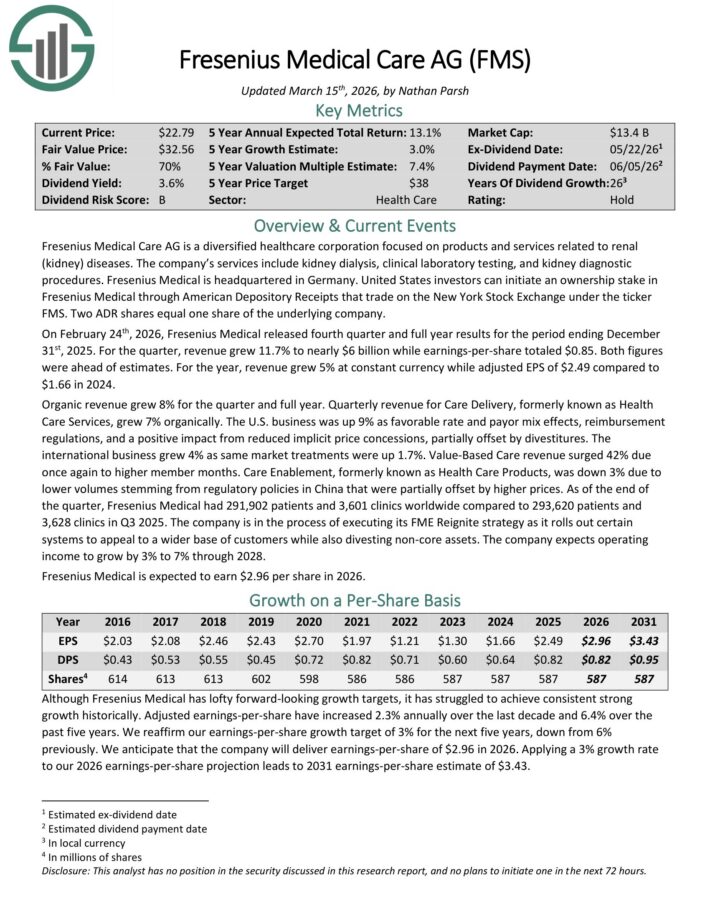

Excessive Yield European Inventory #5: Fresenius Medical Care AG (FMS)

Fresenius Medical Care AG is a diversified healthcare company targeted on services associated to renal ailments.

The corporate’s companies embrace kidney dialysis, medical laboratory testing, and kidney diagnostic procedures. Fresenius Medical is headquartered in Germany.

On February twenty fourth, 2026, Fresenius Medical launched fourth quarter and full 12 months outcomes. For the quarter, income grew 11.7% to almost $6 billion whereas earnings-per-share totaled $0.85. Each figures have been forward of estimates.

For the 12 months, income grew 5% at fixed forex whereas adjusted EPS of $2.49 in comparison with $1.66 in 2024. Natural income grew 8% for the quarter and full 12 months.

Quarterly income for Care Supply, previously often known as Well being Care Providers, grew 7% organically. The U.S. enterprise was up 9% as favorable charge and payor combine results, reimbursement laws, and a constructive influence from decreased implicit value concessions, partially offset by divestitures.

The worldwide enterprise grew 4% as identical market remedies have been up 1.7%. Worth-Primarily based Care income surged 42% due as soon as once more to greater member months.

As of the top of the quarter, Fresenius Medical had 291,902 sufferers and three,601 clinics worldwide in comparison with 293,620 sufferers and three,628 clinics in Q3 2025.

The corporate expects working earnings to develop by 3% to 7% via 2028. Fresenius Medical is anticipated to earn $2.96 per share in 2026.

Click on right here to obtain our most up-to-date Certain Evaluation report on FMS (preview of web page 1 of three proven under):

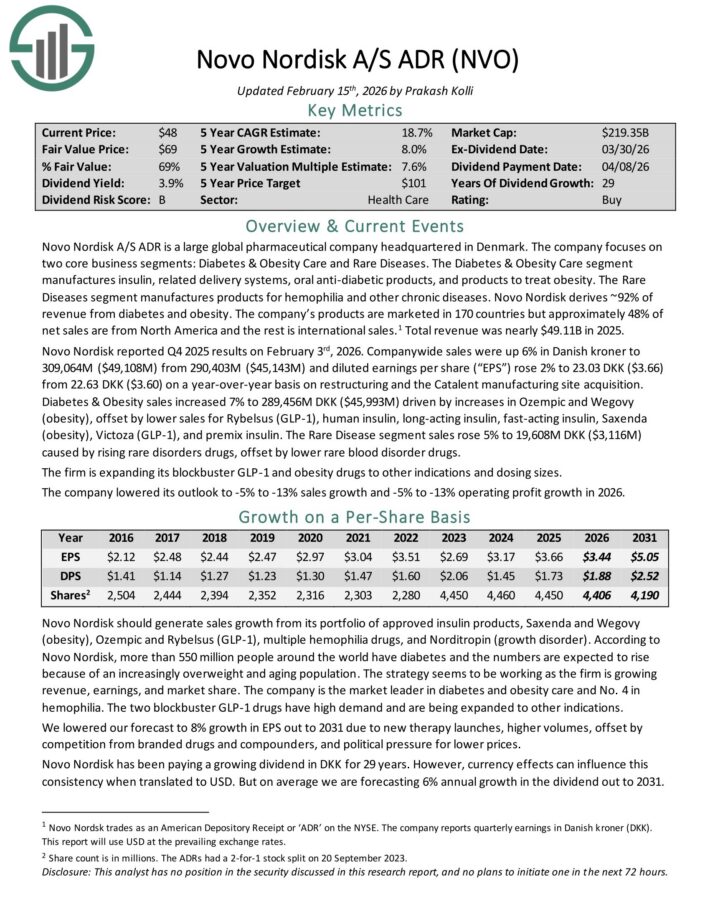

Excessive Yield European Inventory #4: Novo Nordisk (NVO)

Novo Nordisk A/S ADR is a big international pharmaceutical firm headquartered in Denmark. The corporate focuses on two core enterprise segments: Diabetes & Weight problems Care and Uncommon Ailments.

The Diabetes & Weight problems Care section manufactures insulin, associated supply techniques, oral anti-diabetic merchandise, and merchandise to deal with weight problems.

The Uncommon Ailments section manufactures merchandise for hemophilia and different persistent ailments. Novo Nordisk derives ~92% of income from diabetes and weight problems.

The corporate’s merchandise are marketed in 170 nations however roughly 48% of web gross sales are from North America and the remainder is worldwide gross sales.1 Complete income was almost $49.11B in 2025.

Novo Nordisk reported This autumn 2025 outcomes on February third, 2026. Firm-wide gross sales have been up 6% in Danish kroner and diluted earnings per share rose 2% to 23.03 DKK ($3.66) from 22.63 DKK ($3.60) on a year-over-year foundation.

Diabetes & Weight problems gross sales elevated 7% to 289,456M DKK ($45,993M) pushed by will increase in Ozempic and Wegovy (weight problems), offset by decrease gross sales for Rybelsus (GLP-1), human insulin, long-acting insulin, fast-acting insulin, Saxenda (weight problems), Victoza (GLP-1), and premix insulin.

The Uncommon Illness section gross sales rose 5% to 19,608M DKK ($3,116M) brought on by rising uncommon problems medication, offset by decrease uncommon blood dysfunction medication.

Click on right here to obtain our most up-to-date Certain Evaluation report on NVO (preview of web page 1 of three proven under):

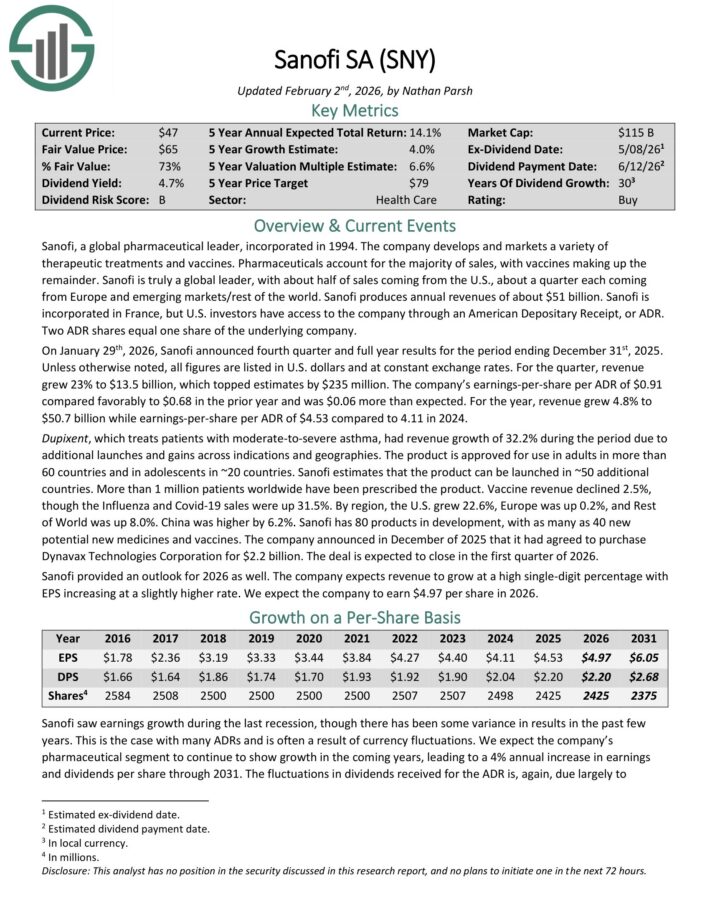

Excessive Yield European Inventory #3: Sanofi (SNY)

Sanofi is a world pharmaceutical chief that develops quite a lot of therapeutic remedies and vaccines.

Prescription drugs account for almost all of gross sales, with vaccines making up the rest. Sanofi produces annual revenues of about $51 billion.

Sanofi is included in France, however U.S. traders have entry to the corporate via an American Depositary Receipt, or ADR. Two ADR shares equal one share of the underlying firm.

On January twenty ninth, 2026, Sanofi introduced fourth quarter and full 12 months outcomes. Except in any other case famous, all figures are listed in U.S. {dollars} and at fixed change charges.

For the quarter, income grew 23% to $13.5 billion, which topped estimates by $235 million. The corporate’s earnings-per-share per ADR of $0.91 in contrast favorably to $0.68 within the prior 12 months and was $0.06 greater than anticipated.

For the 12 months, income grew 4.8% to $50.7 billion whereas earnings-per-share per ADR of $4.53 in comparison with 4.11 in 2024.

Dupixent, which treats sufferers with moderate-to-severe bronchial asthma, had income progress of 32.2% in the course of the interval resulting from extra launches and features throughout indications and geographies.

Sanofi has 80 merchandise in growth, with as many as 40 new potential new medicines and vaccines.

Sanofi supplied an outlook for 2026 as properly. The corporate expects income to develop at a excessive single-digit share with EPS growing at a barely greater charge.

Click on right here to obtain our most up-to-date Certain Evaluation report on SNY (preview of web page 1 of three proven under):

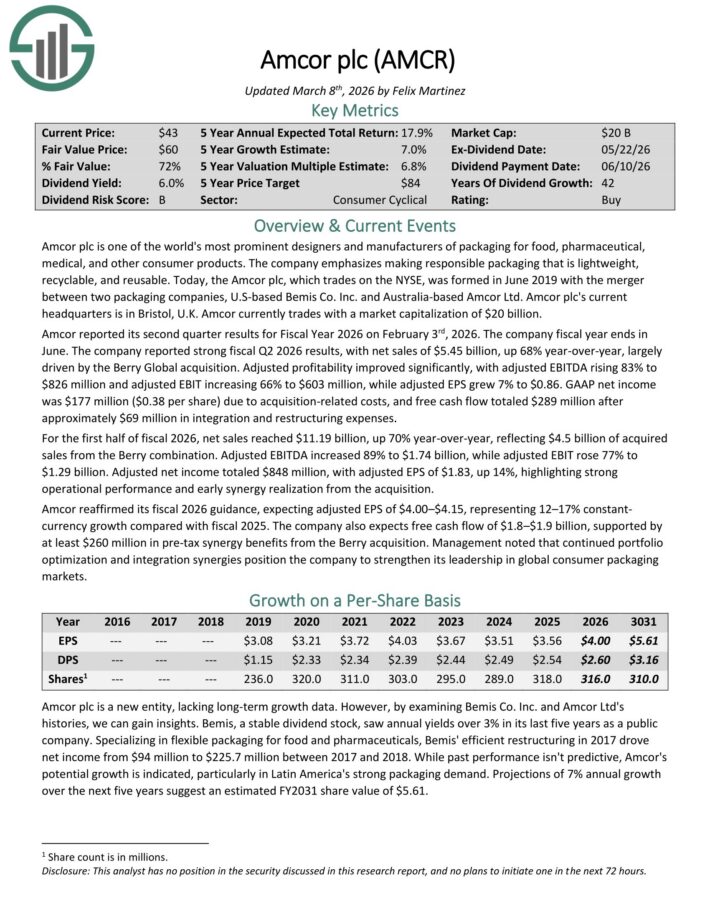

Excessive Dividend Inventory For The Lengthy Run #2: Amcor plc (AMCR)

Amcor plc is without doubt one of the world’s most distinguished designers and producers of packaging for meals, pharmaceutical, medical, and different shopper merchandise.

Amcor reported its second quarter outcomes for Fiscal 12 months 2026 on February third, 2026. The corporate reported robust fiscal Q2 2026 outcomes, with web gross sales of $5.45 billion, up 68% year-over-year, largely pushed by the Berry International acquisition.

Adjusted profitability improved considerably, with adjusted EBITDA rising 83% to $826 million and adjusted EBIT growing 66% to $603 million, whereas adjusted EPS grew 7% to $0.86.

GAAP web earnings was $177 million ($0.38 per share) resulting from acquisition-related prices, and free money circulate totaled $289 million after roughly $69 million in integration and restructuring bills.

For the primary half of fiscal 2026, web gross sales reached $11.19 billion, up 70% year-over-year, reflecting $4.5 billion of acquired gross sales from the Berry mixture.

Amcor reaffirmed its fiscal 2026 steering, anticipating adjusted EPS of $4.00–$4.15, representing 12–17% fixed forex progress in contrast with fiscal 2025.

The corporate additionally expects free money circulate of $1.8–$1.9 billion, supported by at the least $260 million in pre-tax synergy advantages from the Berry acquisition.

Click on right here to obtain our most up-to-date Certain Evaluation report on AMCR (preview of web page 1 of three proven under):

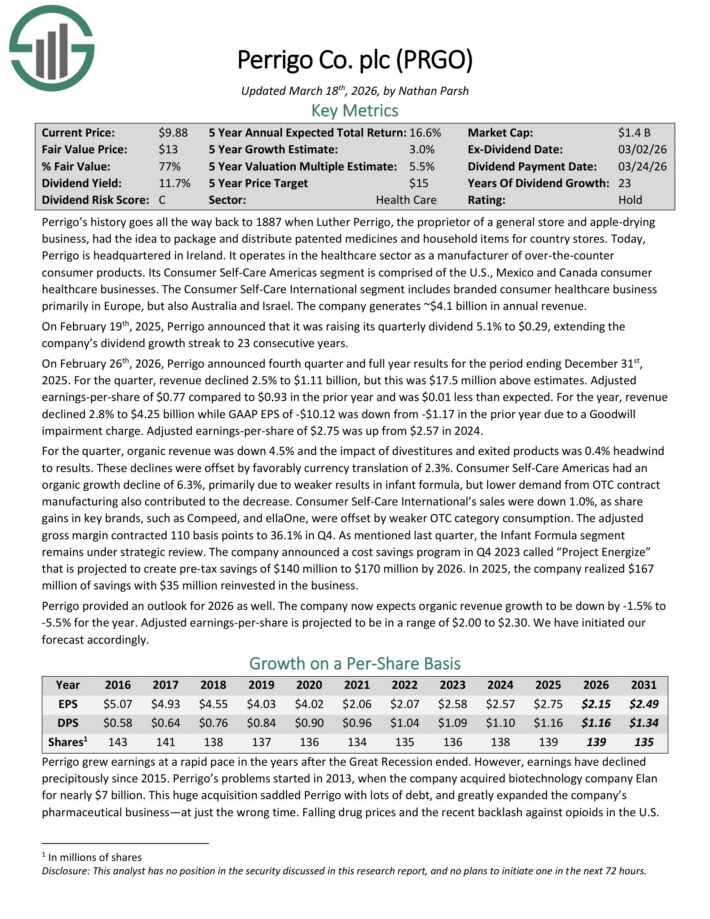

Excessive Yield European Inventory #1: Perrigo Firm plc (PRGO)

Perrigo is headquartered in Eire and operates within the healthcare sector as a producer of over-the-counter shopper merchandise.

Its Shopper Self-Care Americas section is comprised of the U.S., Mexico and Canada shopper healthcare companies.

The Shopper Self-Care Worldwide section contains branded shopper healthcare enterprise primarily in Europe, but in addition Australia and Israel. The corporate generates ~$4.1 billion in annual income.

On February twenty sixth, 2026, Perrigo introduced fourth quarter and full 12 months outcomes for the interval ending December thirty first, 2025. For the quarter, income declined 2.5% to $1.11 billion, however this was $17.5 million above estimates.

Adjusted earnings-per-share of $0.77 in comparison with $0.93 within the prior 12 months and was $0.01 lower than anticipated.

For the 12 months, income declined 2.8% to $4.25 billion whereas GAAP EPS of -$10.12 was down from -$1.17 within the prior 12 months resulting from a Goodwill impairment cost. Adjusted earnings-per-share of $2.75 was up from $2.57 in 2024.

Shopper Self-Care Americas had an natural progress decline of 6.3%, primarily resulting from weaker leads to toddler system, however decrease demand from OTC contract manufacturing additionally contributed to the lower.

Shopper Self-Care Worldwide’s gross sales have been down 1.0%, as share features in key manufacturers, reminiscent of Compeed, and ellaOne, have been offset by weaker OTC class consumption.

The Toddler Method section stays below strategic overview. The corporate introduced a price financial savings program in This autumn 2023 referred to as “Undertaking Energize” that’s projected to create pre-tax financial savings of $140 million to $170 million by 2026.

Perrigo supplied an outlook for 2026 as properly. The corporate now expects natural income progress to be down by -1.5% to -5.5% for the 12 months. Adjusted earnings-per-share is projected to be in a variety of $2.00 to $2.30.

Click on right here to obtain our most up-to-date Certain Evaluation report on PRGO (preview of web page 1 of three proven under):

Extra Studying

In case you are all in favour of discovering high-quality dividend progress shares and/or different high-yield securities and earnings securities, the next Certain Dividend sources will likely be helpful:

Excessive-Yield Particular person Safety Analysis

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

{kind=link}