Printed on April twentieth, 2026 by Bob Ciura

The perfect retirement funding would mix:

- Low valuation

- Robust anticipated development

- Excessive beginning dividend yield

Sadly, this mix is tough to search out within the inventory market.

Tough, however not unattainable.

And that’s the place excessive dividend shares are available in.

With this in thoughts, we’ve created a spreadsheet of over 200 shares with dividend yields of 5% or extra…

You’ll be able to obtain your free full listing of all excessive dividend shares with 5%+ yields (together with necessary monetary metrics equivalent to dividend yield and payout ratio) by clicking on the hyperlink under:

The one time all three of those elements happen collectively is when a development inventory that’s established sufficient to pay rising dividends, experiences a brief valuation decline.

This could happen when the market misjudges the length of a brief adverse occasion, or throughout a broader market downturn.

However all this spells alternative for buy-and-hold traders.

This text will talk about 10 retirement shares which have present yields of 4% or greater, which makes them engaging for revenue traders.

On the identical time, these 10 perfect retirement shares have secure dividends, with Dividend Danger Scores of ‘A’ or ‘B’, our highest rankings.

Lastly, the ten perfect retirement shares have constructive anticipated earnings development sooner or later, and are presently buying and selling under truthful worth.

The shares are listed by annual anticipated returns over the subsequent 5 years, from lowest to highest.

Desk Of Contents

The desk of contents under gives for straightforward navigation of the article:

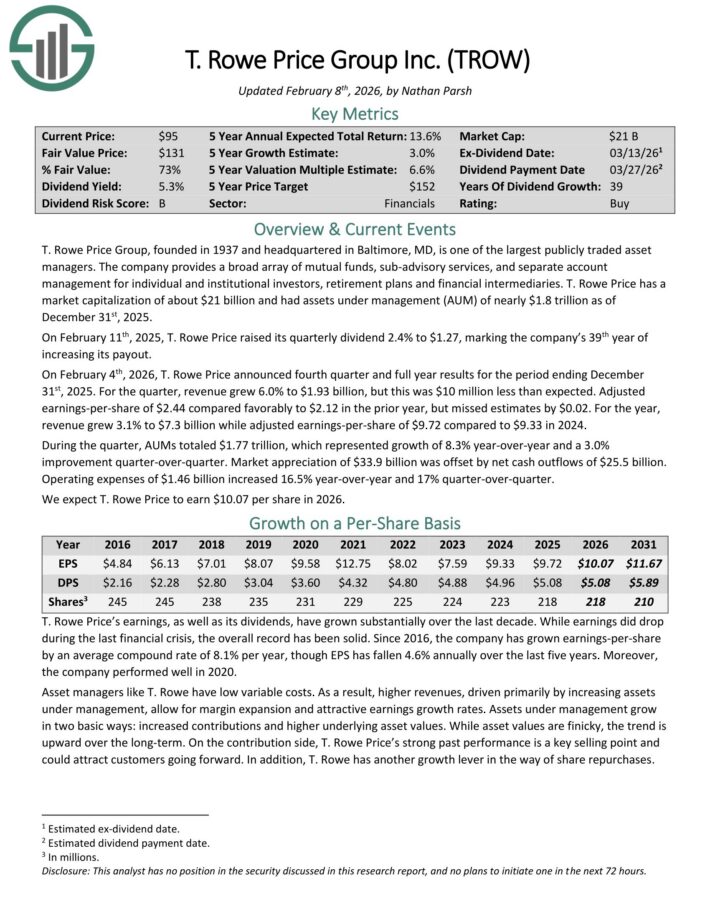

Perfect Retirement Funding #10: T. Rowe Worth Group (TROW)

- Annual Anticipated Returns: 13.2%

T. Rowe Worth Group is without doubt one of the largest publicly traded asset managers. The corporate gives a broad array of mutual funds, sub-advisory companies, and separate account administration for particular person and institutional traders, retirement plans and monetary intermediaries.

T. Rowe Worth had belongings below administration (AUM) of almost $1.8 trillion as of December thirty first, 2025.

On February eleventh, 2025, T. Rowe Worth raised its quarterly dividend 2.4% to $1.27, marking the corporate’s thirty ninth yr of accelerating its payout.

On February 4th, 2026, T. Rowe Worth introduced fourth quarter and full yr outcomes for the interval ending December thirty first, 2025.

For the quarter, income grew 6.0% to $1.93 billion, however this was $10 million lower than anticipated. Adjusted earnings-per-share of $2.44 in contrast favorably to $2.12 within the prior yr, however missed estimates by $0.02.

For the yr, income grew 3.1% to $7.3 billion whereas adjusted earnings-per-share of $9.72 in comparison with $9.33 in 2024. Through the quarter, AUMs totaled $1.77 trillion, which represented development of 8.3% year-over-year and a 3.0% enchancment quarter-over-quarter.

Market appreciation of $33.9 billion was offset by internet money outflows of $25.5 billion. Working bills of $1.46 billion elevated 16.5% year-over-year and 17% quarter-over-quarter.

Click on right here to obtain our most up-to-date Positive Evaluation report on TROW (preview of web page 1 of three proven under):

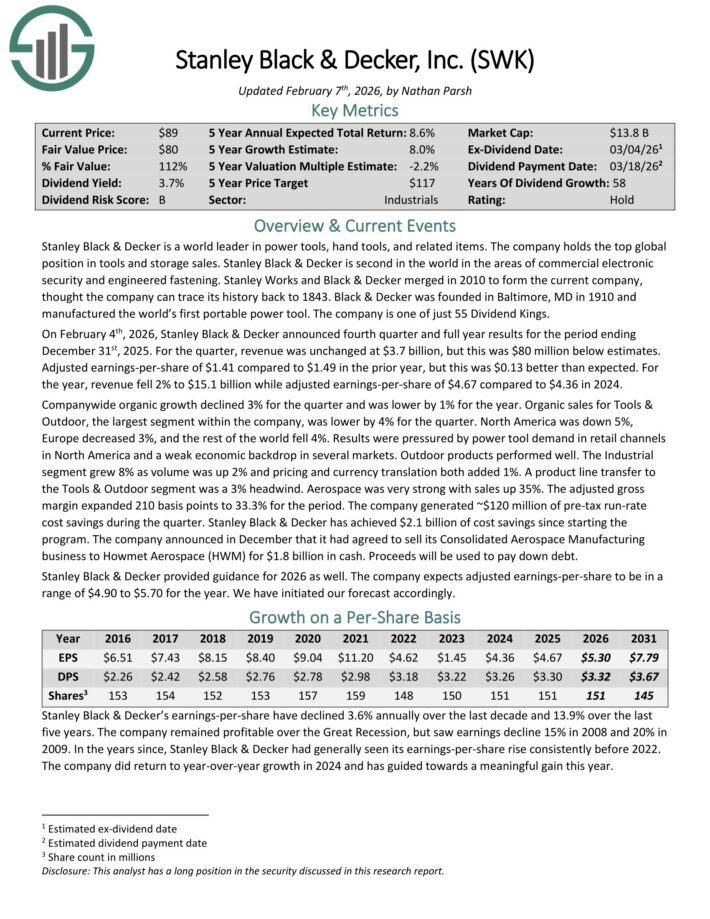

Perfect Retirement Funding #9: Stanley Black & Decker (SWK)

- Annual Anticipated Returns: 13.6%

Stanley Black & Decker is a world chief in energy instruments, hand instruments, and associated objects. The corporate holds the highest international place in instruments and storage gross sales.

Stanley Black & Decker is second on the planet within the areas of economic digital safety and engineered fastening. The corporate consists of three segments: instruments & outside, and industrial.

On February 4th, 2026, Stanley Black & Decker introduced fourth quarter and full yr outcomes. For the quarter, income was unchanged at $3.7 billion, however this was $80 million under estimates.

Adjusted earnings-per-share of $1.41 in comparison with $1.49 within the prior yr, however this was $0.13 higher than anticipated. For the yr, income fell 2% to $15.1 billion whereas adjusted earnings-per-share of $4.67 in comparison with $4.36 in 2024.

Firm-wide natural development declined 3% for the quarter and was decrease by 1% for the yr. Natural gross sales for Instruments & Outside, the most important phase inside the firm, was decrease by 4% for the quarter.

North America was down 5%, Europe decreased 3%, and the remainder of the world fell 4%. Outcomes have been pressured by energy device demand in retail channels in North America and a weak financial backdrop in a number of markets.

Click on right here to obtain our most up-to-date Positive Evaluation report on SWK (preview of web page 1 of three proven under):

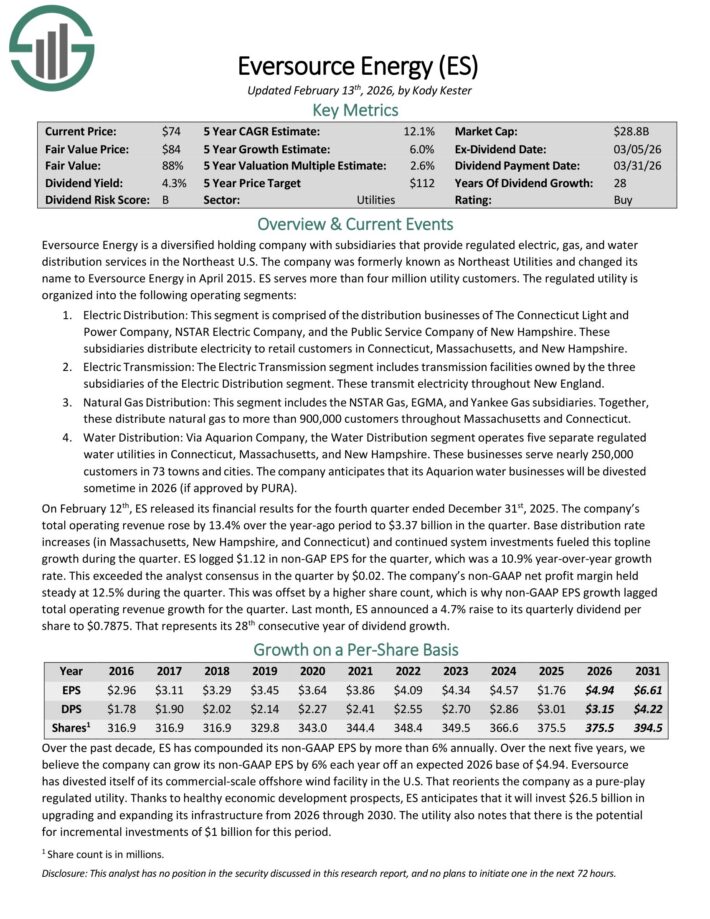

Perfect Retirement Funding #8: Eversource Vitality (ES)

- Annual Anticipated Return: 13.6%

Eversource Vitality is a diversified holding firm with subsidiaries that present regulated electrical, gasoline, and water distribution companies within the Northeast U.S.

ES serves greater than 4 million utility prospects.

On February twelfth, ES launched its monetary outcomes for the fourth quarter. The corporate’s complete working income rose by 13.4% over the year-ago interval to $3.37 billion within the quarter.

Base distribution price will increase (in Massachusetts, New Hampshire, and Connecticut) and continued system investments fueled this prime line development.

ES logged $1.12 in non-GAP EPS for the quarter, which was a ten.9% year-over-year development price. This exceeded the analyst consensus within the quarter by $0.02.

The corporate’s non-GAAP internet revenue margin held regular at 12.5% through the quarter. This was offset by the next share rely, which is why non-GAAP EPS development lagged complete working income development for the quarter.

ES introduced a 4.7% increase to its quarterly dividend per share to $0.7875. That represented its twenty eighth consecutive yr of dividend development.

For 2026, we count on ES to generate adjusted EPS of $4.94.

Click on right here to obtain our most up-to-date Positive Evaluation report on ES (preview of web page 1 of three proven under):

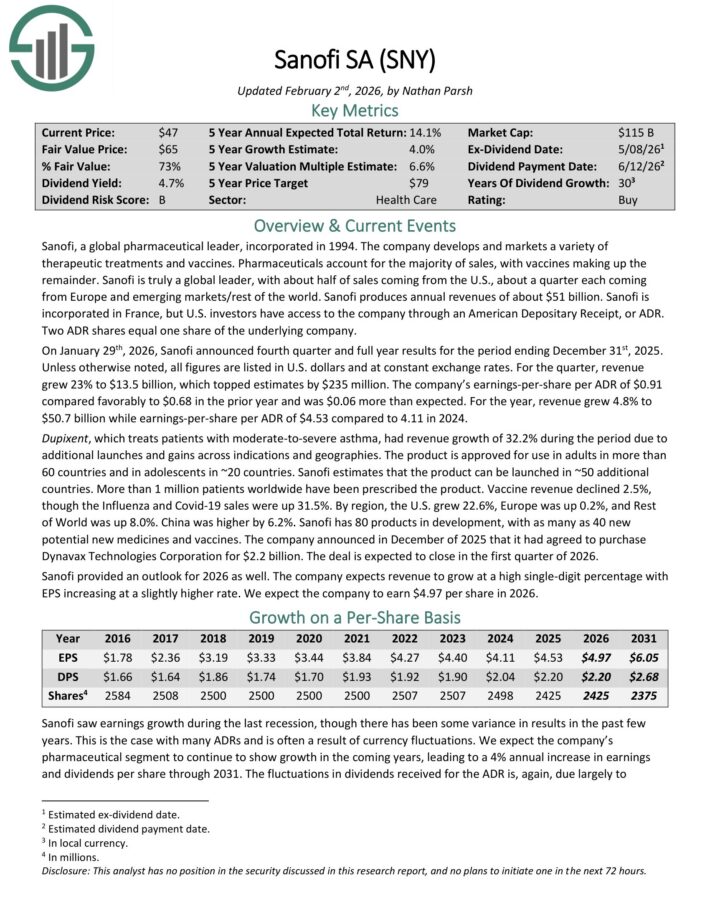

Perfect Retirement Funding #7: Sanofi (SNY)

- Annual Anticipated Returns: 13.7%

Sanofi is a worldwide pharmaceutical chief that develops a wide range of therapeutic therapies and vaccines.

Prescription drugs account for almost all of gross sales, with vaccines making up the rest. Sanofi produces annual revenues of about $51 billion.

Sanofi is integrated in France, however U.S. traders have entry to the corporate by way of an American Depositary Receipt, or ADR. Two ADR shares equal one share of the underlying firm.

On January twenty ninth, 2026, Sanofi introduced fourth quarter and full yr outcomes. Except in any other case famous, all figures are listed in U.S. {dollars} and at fixed change charges.

For the quarter, income grew 23% to $13.5 billion, which topped estimates by $235 million. The corporate’s earnings-per-share per ADR of $0.91 in contrast favorably to $0.68 within the prior yr and was $0.06 greater than anticipated.

For the yr, income grew 4.8% to $50.7 billion whereas earnings-per-share per ADR of $4.53 in comparison with 4.11 in 2024.

Dupixent, which treats sufferers with moderate-to-severe bronchial asthma, had income development of 32.2% through the interval attributable to extra launches and features throughout indications and geographies.

Sanofi has 80 merchandise in improvement, with as many as 40 new potential new medicines and vaccines.

Sanofi offered an outlook for 2026 as nicely. The corporate expects income to develop at a excessive single-digit share with EPS rising at a barely greater price.

Click on right here to obtain our most up-to-date Positive Evaluation report on SNY (preview of web page 1 of three proven under):

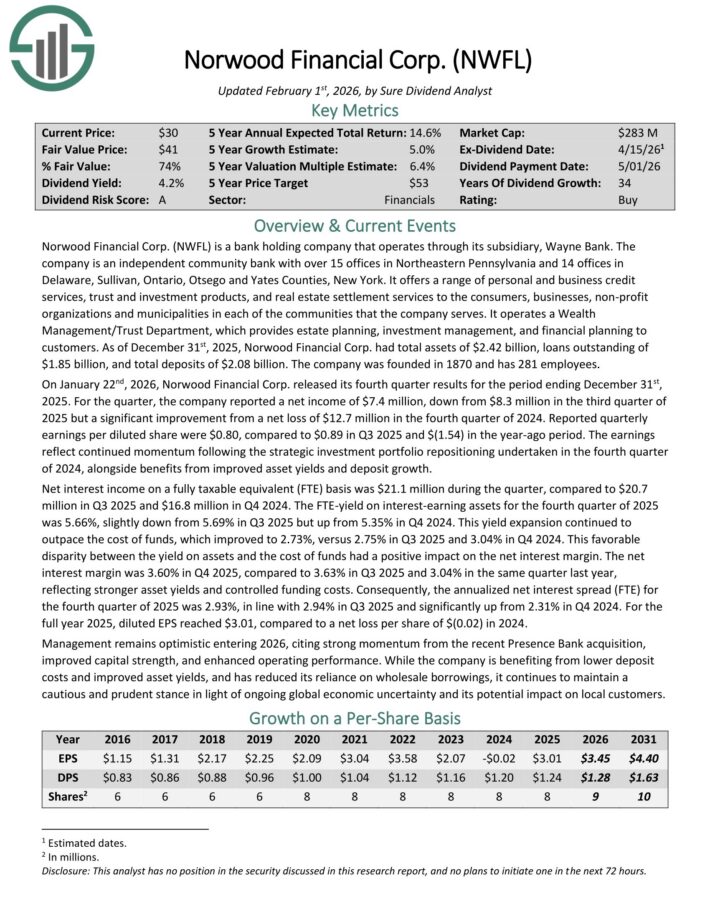

Perfect Retirement Funding #6: Norwood Monetary (NWFL)

- Annual Anticipated Returns: 13.7%

Norwood Monetary is a financial institution holding firm that operates by way of its subsidiary, Wayne Financial institution. The corporate is an unbiased group financial institution with over 15 workplaces in Northeastern Pennsylvania and 14 workplaces in Delaware, Sullivan, Ontario, Otsego and Yates Counties, New York.

It presents a variety of non-public and enterprise credit score companies, belief and funding merchandise, and actual property settlement companies to the shoppers, companies, non-profit organizations and municipalities in every of the communities that the corporate serves.

As of December thirty first, 2025, Norwood Monetary Corp. had complete belongings of $2.42 billion, loans excellent of $1.85 billion, and complete deposits of $2.08 billion.

On January twenty second, 2026, Norwood Monetary Corp. launched its fourth quarter outcomes. For the quarter, the corporate reported a internet revenue of $7.4 million, down from $8.3 million within the third quarter of 2025 however a major enchancment from a internet lack of $12.7 million within the fourth quarter of 2024.

Reported quarterly earnings per diluted share have been $0.80, in comparison with $0.89 in Q3 2025 and $(1.54) within the year-ago interval.

The earnings mirror continued momentum following the strategic funding portfolio repositioning undertaken within the fourth quarter of 2024, alongside advantages from improved asset yields and deposit development.

Click on right here to obtain our most up-to-date Positive Evaluation report on NWFL (preview of web page 1 of three proven under):

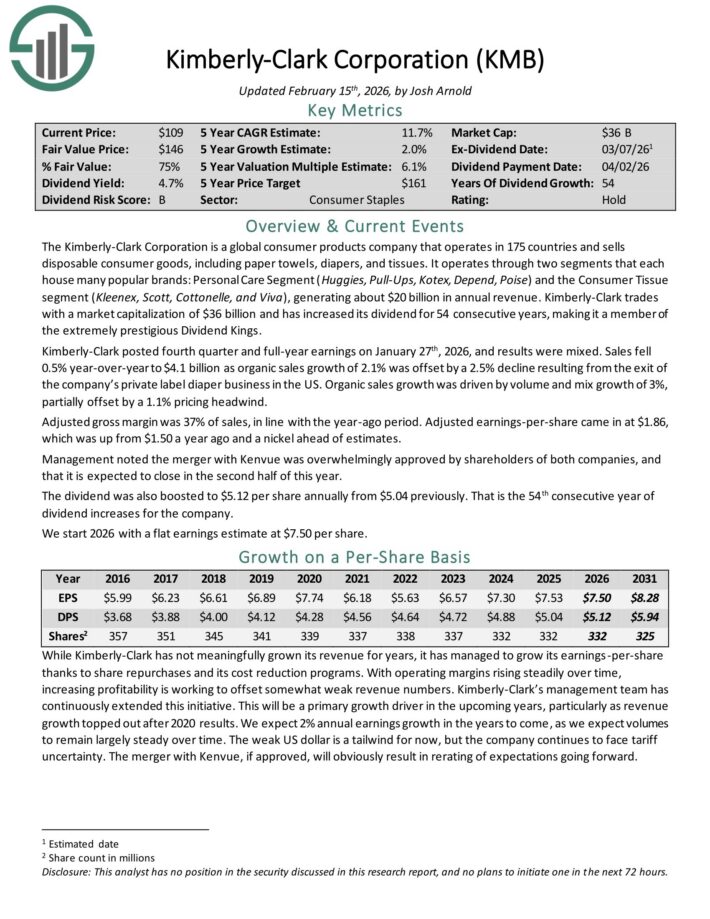

Perfect Retirement Funding #5: Kimberly-Clark Corp. (KMB)

- Annual Anticipated Returns: 13.9%

The Kimberly-Clark Company is a worldwide shopper merchandise firm that operates in 175 international locations and sells disposable shopper items, together with paper towels, diapers, and tissues.

It operates by way of two segments that every home many fashionable manufacturers: Private Care Phase (Huggies, Pull-Ups, Kotex, Rely, Poise) and the Client Tissue phase (Kleenex, Scott, Cottonelle, and Viva), producing about $20 billion in annual income.

Kimberly-Clark posted fourth quarter and full-year earnings on January twenty seventh, 2026. Gross sales fell 0.5% year-over-year to $4.1 billion as natural gross sales development of two.1% was offset by a 2.5% decline ensuing from the exit of the corporate’s non-public label diaper enterprise within the US.

Natural gross sales development was pushed by quantity and blend development of three%, partially offset by a 1.1% pricing headwind.

Adjusted gross margin was 37% of gross sales, in step with the year-ago interval. Adjusted earnings-per-share got here in at $1.86, which was up from $1.50 a yr in the past and a nickel forward of estimates.

Administration famous the merger with Kenvue was overwhelmingly authorised by shareholders of each firms, and that it’s anticipated to shut within the second half of this yr.

The dividend was additionally boosted to $5.12 per share yearly from $5.04 beforehand. That’s the 54th consecutive yr of dividend will increase for the corporate.

Click on right here to obtain our most up-to-date Positive Evaluation report on KMB (preview of web page 1 of three proven under):

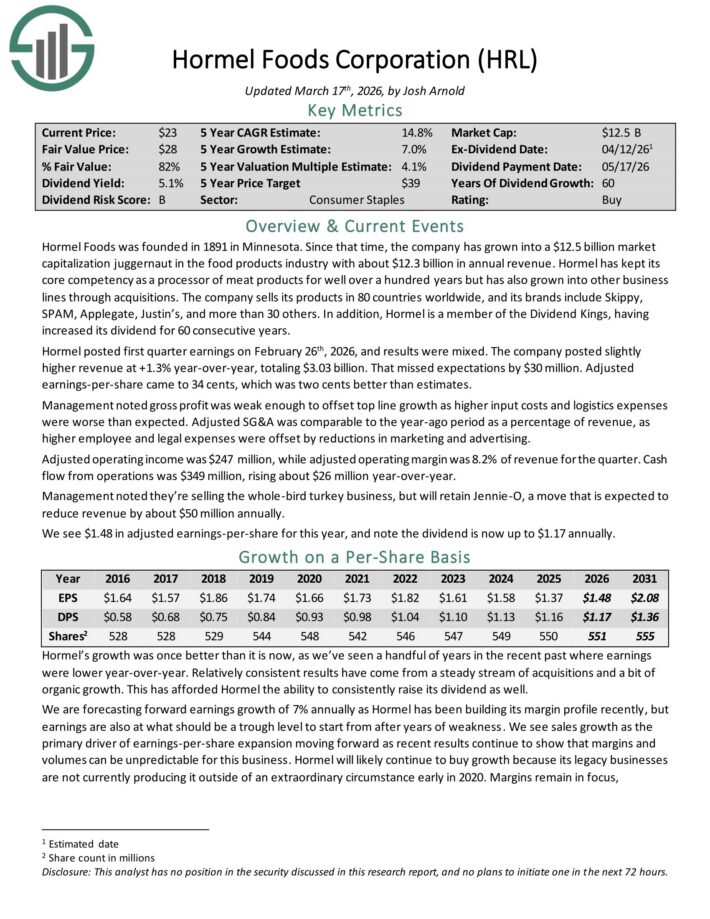

Perfect Retirement Funding #4: Hormel Meals Corp. (HRL)

- Annual Anticipated Returns: 16.6%

Hormel Meals was based in 1891 in Minnesota. Since that point, the corporate has grown right into a juggernaut within the meals merchandise trade with about $12.3 billion in annual income.

The corporate sells its merchandise in 80 international locations worldwide, and its manufacturers embrace Skippy, SPAM, Applegate, Justin’s, and greater than 30 others.

Hormel posted first quarter earnings on February twenty sixth, 2026, and outcomes have been combined. The corporate posted barely greater income at +1.3% year-over-year, totaling $3.03 billion. That missed expectations by $30 million.

Adjusted earnings-per-share got here to 34 cents, which was two cents higher than estimates.

Administration famous gross revenue was weak sufficient to offset prime line development as greater enter prices and logistics bills have been worse than anticipated.

Adjusted SG&A was akin to the year-ago interval as a share of income, as greater worker and authorized bills have been offset by reductions in advertising and promoting.

Adjusted working revenue was $247 million, whereas adjusted working margin was 8.2% of income for the quarter. Money circulate from operations was $349 million, rising about $26 million year-over-year.

Click on right here to obtain our most up-to-date Positive Evaluation report on HRL (preview of web page 1 of three proven under):

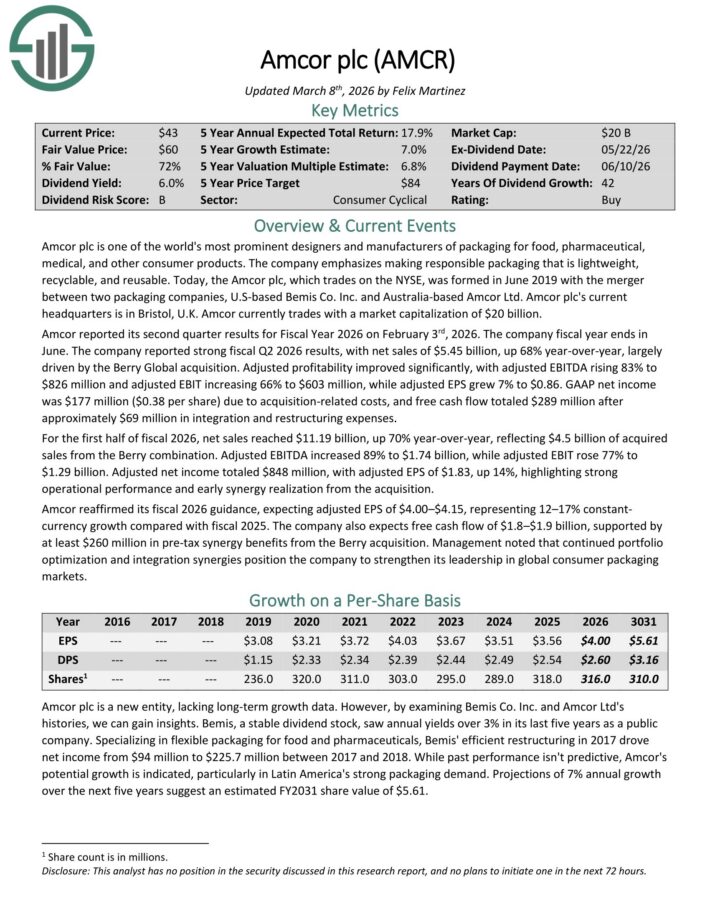

Perfect Retirement Funding #3: Amcor plc (AMCR)

- Annual Anticipated Return: 18.6%

Amcor plc is without doubt one of the world’s most distinguished designers and producers of packaging for meals, pharmaceutical, medical, and different shopper merchandise. The corporate emphasizes making accountable packaging that’s light-weight, recyclable, and reusable.

Amcor reported its second quarter outcomes for Fiscal 12 months 2026 on February third, 2026. The corporate reported sturdy fiscal Q2 2026 outcomes, with internet gross sales of $5.45 billion, up 68% year-over-year, largely pushed by the Berry International acquisition.

Adjusted profitability improved considerably, with adjusted EBITDA rising 83% to $826 million and adjusted EBIT rising 66% to $603 million, whereas adjusted EPS grew 7% to $0.86.

GAAP internet revenue was $177 million ($0.38 per share) attributable to acquisition-related prices, and free money circulate totaled $289 million after roughly $69 million in integration and restructuring bills.

For the primary half of fiscal 2026, internet gross sales reached $11.19 billion, up 70% year-over-year, reflecting $4.5 billion of acquired gross sales from the Berry mixture.

Amcor reaffirmed its fiscal 2026 steerage, anticipating adjusted EPS of $4.00–$4.15, representing 12–17% fixed forex development in contrast with fiscal 2025.

The corporate additionally expects free money circulate of $1.8–$1.9 billion, supported by no less than $260 million in pre-tax synergy advantages from the Berry acquisition.

Click on right here to obtain our most up-to-date Positive Evaluation report on AMCR (preview of web page 1 of three proven under):

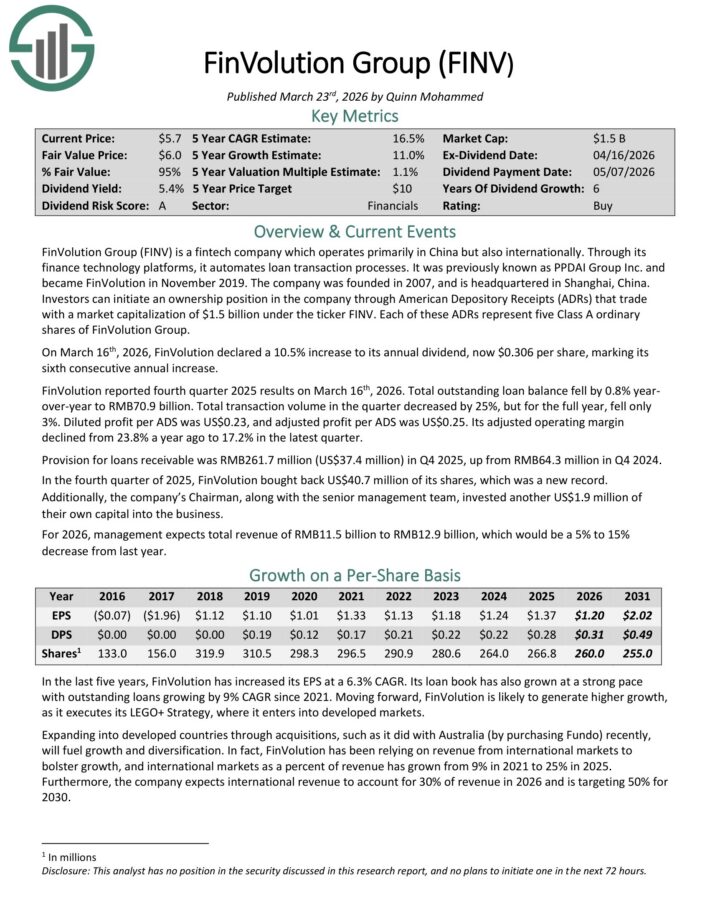

Perfect Retirement Funding #2: FinVolution Group (FINV)

- Annual Anticipated Returns: 20.4%

FinVolution Group is a fintech firm which operates primarily in China but additionally internationally. Via its finance expertise platforms, it automates mortgage transaction processes.

The corporate was based in 2007, and is headquartered in Shanghai, China.

Buyers can provoke an possession place within the firm by way of American Depository Receipts (ADRs) below the ticker FINV. Every of those ADRs signify 5 Class A peculiar shares of FinVolution Group.

On March sixteenth, 2026, FinVolution declared a ten.5% improve to its annual dividend, now $0.306 per share, marking its sixth consecutive annual improve.

FinVolution reported fourth quarter 2025 outcomes on March sixteenth, 2026. Whole excellent mortgage steadiness fell by 0.8% year-over-year to RMB70.9 billion.

Whole transaction quantity within the quarter decreased by 25%, however for the total yr, fell solely 3%.

Diluted revenue per ADS was US$0.23, and adjusted revenue per ADS was US$0.25. Its adjusted working margin declined from 23.8% a yr in the past to 17.2% within the newest quarter.

Provision for loans receivable was RMB261.7 million (US$37.4 million) in This autumn 2025, up from RMB64.3 million in This autumn 2024.

For 2026, administration expects complete income of RMB11.5 billion to RMB12.9 billion, which might be a 5% to fifteen% lower from final yr.

Click on right here to obtain our most up-to-date Positive Evaluation report on FINV (preview of web page 1 of three proven under):

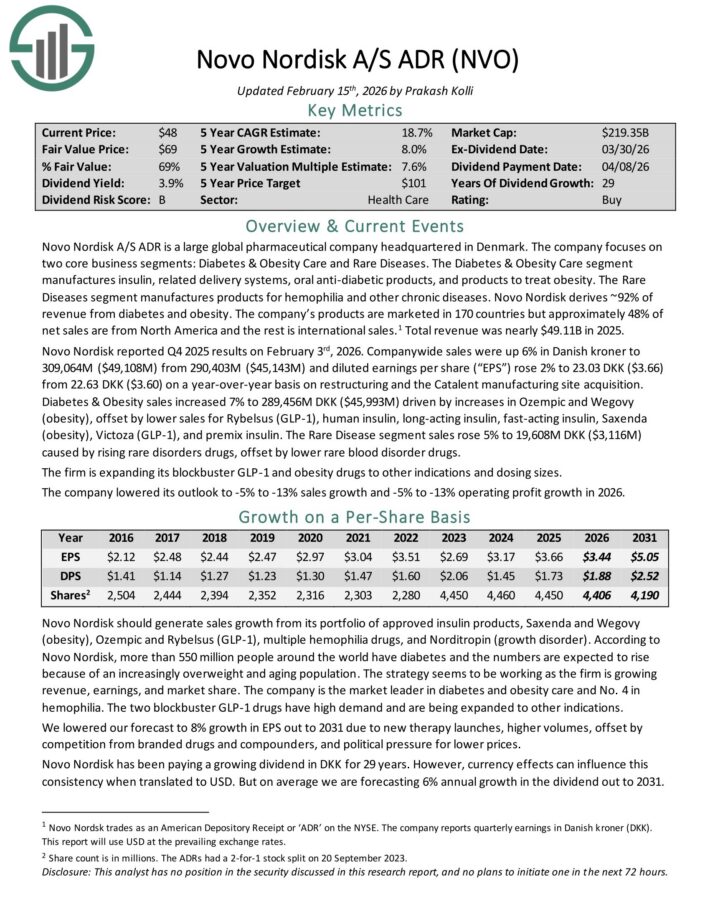

Perfect Retirement Funding #1: Novo Nordisk (NVO)

- Annual Anticipated Return: 22.6%

Novo Nordisk A/S ADR is a big international pharmaceutical firm headquartered in Denmark. The corporate focuses on two core enterprise segments: Diabetes & Weight problems Care and Uncommon Ailments.

The Diabetes & Weight problems Care phase manufactures insulin, associated supply methods, oral anti-diabetic merchandise, and merchandise to deal with weight problems.

The Uncommon Ailments phase manufactures merchandise for hemophilia and different continual illnesses. Novo Nordisk derives ~92% of income from diabetes and weight problems.

The corporate’s merchandise are marketed in 170 international locations however roughly 48% of internet gross sales are from North America and the remaining is worldwide gross sales.1 Whole income was almost $49.11B in 2025.

Novo Nordisk reported This autumn 2025 outcomes on February third, 2026. Companywide gross sales have been up 6% in Danish kroner and diluted earnings per share rose 2% to 23.03 DKK ($3.66) from 22.63 DKK ($3.60) on a year-over-year foundation.

Diabetes & Weight problems gross sales elevated 7% to 289,456M DKK ($45,993M) pushed by will increase in Ozempic and Wegovy (weight problems), offset by decrease gross sales for Rybelsus (GLP-1), human insulin, long-acting insulin, fast-acting insulin, Saxenda (weight problems), Victoza (GLP-1), and premix insulin.

The Uncommon Illness phase gross sales rose 5% to 19,608M DKK ($3,116M) attributable to rising uncommon issues medication, offset by decrease uncommon blood dysfunction medication.

Click on right here to obtain our most up-to-date Positive Evaluation report on NVO (preview of web page 1 of three proven under):

Further Studying

If you’re concerned about discovering high-quality dividend development shares and/or different high-yield securities and revenue securities, the next Positive Dividend assets might be helpful:

Excessive-Yield Particular person Safety Analysis

Different Positive Dividend Sources

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

{kind=link}