Printed on October twenty second, 2025 by Felix Martinez

Excessive-yield shares pay out dividends which can be considerably increased than the market common. For instance, the S&P 500’s present yield is barely ~1.2%.

Excessive-yield shares might be significantly useful in supplementing retirement earnings. A $120,000 funding in shares with a median dividend yield of 5% creates a median of $500 a month in dividends.

Ellington Monetary Inc. (EFC) is a part of our ‘Excessive Dividend 50’ collection, which covers the 50 highest-yielding shares within the Certain Evaluation Analysis Database.

We have now created a spreadsheet of shares (and intently associated REITs, MLPs, and so on.) with dividend yields of 5% or extra.

You may obtain your free full listing of all securities with 5%+ yields (together with necessary monetary metrics resembling dividend yield and payout ratio) by clicking on the hyperlink under:

Subsequent on our listing of high-dividend shares to overview is Ellington Monetary Inc. (EFC).

Enterprise Overview

Ellington Monetary solely transitioned right into a REIT originally of 2019. Earlier than this, the belief was taxed as a partnership. It’s now categorised as a mortgage REIT.

Ellington Monetary is a hybrid REIT, which means that the belief combines the traits of an fairness REIT, which owns properties, and a mortgage REIT, which invests in mortgage loans and mortgage-backed securities.

The corporate manages mortgage-backed securities backed by prime jumbo loans, Alt-A loans, manufactured housing loans, and subprime residential mortgage loans.

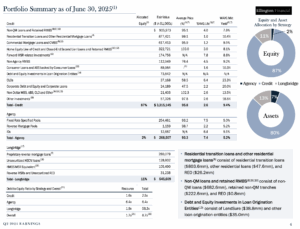

Ellington Monetary has a market capitalization of about $1.4 billion. You may see a snapshot of Ellington’s funding portfolio within the picture under:

Supply: Investor Relations

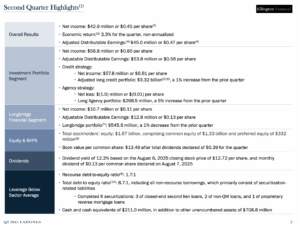

Ellington Monetary Inc. (EFC) posted robust Q2 2025 outcomes, with internet earnings of $42.9 million, or $0.45 per share, and adjusted distributable earnings of $45.0 million, or $0.47 per share, above its $0.39 quarterly dividend. Income rose 14.9% year-over-year to $115.47 million, pushed by broad contributions from its funding portfolio, credit score technique, and Longbridge section. Ebook worth per share elevated to $13.49, and the dividend yield was 12.3%.

The corporate accomplished six securitizations and maintained a secure portfolio, with the credit score portfolio rising barely to $3.32 billion. Internet curiosity margins improved to three.11% attributable to decrease funding prices. Company RMBS outcomes had been impacted by hedge losses, whereas Longbridge’s portfolio declined 1% sequentially however benefited from increased reverse mortgage originations and servicing positive aspects.

Wanting ahead, Ellington plans to broaden its portfolio, speed up securitizations, and leverage Longbridge’s new HELOC for Seniors program. Whole property reached $17.1 billion, with $211 million in money, and debt-to-equity ratios of 1.7:1 (recourse) and eight.7:1 general, reflecting disciplined leverage and monetary flexibility.

Supply: Investor Relations

Progress Prospects

Ellington Monetary’s earnings per share have been uneven over the previous decade, largely attributable to a declining rate of interest surroundings. Consequently, its per-share dividend has largely decreased since 2015.

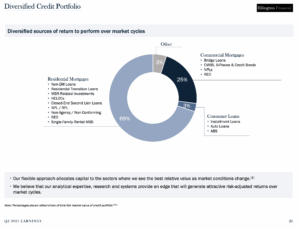

To mitigate volatility, the corporate has centered on diversifying its portfolio throughout a number of funding methods and sectors. This method helps scale back efficiency swings and smooths general returns.

Its residential mortgage investments are unfold throughout numerous safety sorts, together with Non-QM loans, reverse mortgages, and REOs. By avoiding concentrated danger, Ellington improves the steadiness of its financial returns and enhances portfolio resilience.

Supply: Investor Presentation

Ellington has structured its portfolio to attenuate the influence of rate of interest fluctuations on general efficiency. This defensive positioning helps stabilize returns, even in altering market circumstances.

The Federal Reserve has indicated potential future fee cuts if inflation reaches its goal, which might probably profit Ellington. Below the present portfolio, a 50-basis-point decline within the fee may generate $2.2 million in fairness positive aspects, whereas a 50-basis-point improve may end in $9.7 million in losses.

Wanting forward, the corporate is predicted to attain modest development, with projected annual EPS will increase of roughly 1% over the subsequent 5 years. Its portfolio design and danger administration help regular, resilient efficiency.

Aggressive Benefits & Recession Efficiency

Ellington Monetary doesn’t have a serious aggressive benefit, although it maintains a high-quality stability sheet. Its recourse debt-to-equity ratio was 1.8x in This fall, down from 2x on the finish of 2023, reflecting decrease borrowings within the Company RMBS and proprietary reverse mortgage portfolios.

Though the corporate was not publicly traded throughout the Nice Recession, its inventory value fell sharply on the onset of the COVID-19 pandemic. This highlights some sensitivity to market stress regardless of conservative leverage.

For the reason that pandemic, EFC’s earnings and dividends have recovered, but each stay under 2014 ranges. The corporate stays dedicated to sustaining monetary stability amid financial uncertainty.

Dividend Evaluation

Ellington Monetary has a unstable dividend historical past, with cuts and subsequent will increase. The corporate lowered its month-to-month dividend from $0.15 to $0.08 in Q1 2020 as a result of pandemic, later elevating it a number of occasions. In This fall 2023, the month-to-month dividend was lowered from $0.15 to $0.13 to help fairness development and has remained at that degree.

The annual dividend is at the moment $1.56 per share, translating to a yield of 11.5%. Whereas that is engaging for earnings buyers, dividend security is unsure given previous cuts and excessive anticipated payout ratios, that are projected at 96% for 2025. The five-year common payout ratio has been 85%, although it has exceeded 100% in earlier intervals.

Regardless of volatility, Ellington has delivered robust cumulative dividends since its IPO, totaling over $34 per share—practically thrice the present inventory value—demonstrating a traditionally strong earnings stream for shareholders.

Remaining Ideas

Excessive-yield dividend shares warrant warning, as elevated yields usually sign underlying dangers. Ellington Monetary exemplifies this, exhibiting vital volatility in its dividend funds over time.

The corporate maintains a diversified mortgage portfolio and has improved profitability, supporting the present dividend. Nevertheless, a slowdown in enterprise may set off one other lower, highlighting potential danger.

EFC affords a horny yield of 11.5%, however buyers ought to concentrate on the elevated danger related to its inventory.

Excessive-Yield Particular person Safety Analysis

Different Certain Dividend Assets

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

{kind=link}