Revealed on October twenty second, 2025 by Felix Martinez

Excessive-yield shares pay out dividends which can be considerably increased than the market common. For instance, the S&P 500’s present yield is just ~1.2%.

Excessive-yield shares may be significantly useful in supplementing retirement revenue. A $120,000 funding in shares with a mean dividend yield of 5% creates a mean of $500 a month in dividends.

Capital Southwest Company (CSWC) is a part of our ‘Excessive Dividend 50’ sequence, which covers the 50 highest-yielding shares within the Positive Evaluation Analysis Database.

We now have created a spreadsheet of shares (and carefully associated REITs, MLPs, and many others.) with dividend yields of 5% or extra.

You may obtain your free full listing of all securities with 5%+ yields (together with necessary monetary metrics equivalent to dividend yield and payout ratio) by clicking on the hyperlink under:

Subsequent on our listing of high-dividend shares to evaluation is Capital Southwest Company (CSWC).

Enterprise Overview

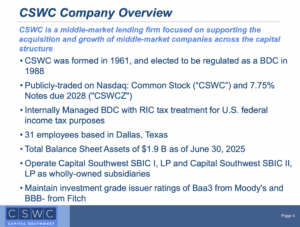

Capital Southwest Company is a Dallas-based, internally managed funding firm structured as a Enterprise Improvement Firm (BDC). It offers tailor-made debt and fairness financing to decrease middle-market (LMM) corporations and debt capital to higher middle-market (UMM) corporations within the U.S., producing roughly $82 million in annual income.

On July 23, 2025, the corporate modified its base dividend to a month-to-month fee of $0.1934 per share, together with a supplemental dividend of $0.06, sustaining an annualized base dividend of $2.32, as mirrored in our estimates.

Supply: Investor Relations

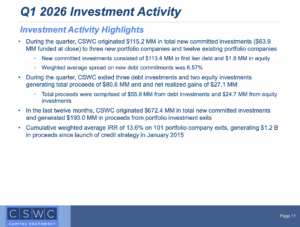

Capital Southwest Company (Nasdaq: CSWC) reported Q1 FY2026 outcomes for the quarter ended June 30, 2025. The corporate’s $1.8 billion funding portfolio contains $1.6 billion in credit score, principally first-lien senior secured debt, and $166 million in fairness. In the course of the quarter, CSWC dedicated $113.4 million in new credit score and $1.8 million in fairness co-investments. Pre-tax internet funding revenue was $32.7 million ($0.61 per share), supported by $27.2 million in realized fairness positive aspects. Money totaled $46.9 million, internet belongings $916.5 million, NAV $16.59 per share, and dividends have been $0.64 per share.

CSWC originated $115.2 million in new investments and acquired $80.6 million in proceeds from prepayments and exits, producing $27.1 million in internet realized positive aspects. Whole funding revenue rose to $55.9 million from $52.4 million, pushed by increased curiosity revenue and yields. Working bills have been $8.0 million, curiosity expense $15.3 million, and internet funding losses totaled $4.9 million, leading to a $27.0 million enhance in internet belongings for the quarter.

Liquidity stays robust, with $46.9 million in money and $397.2 million in unused credit score capability. CSWC raised $41.7 million by way of its Fairness ATM Program and holds SBA licenses for added leverage. The corporate will shift common dividends to a month-to-month schedule and expects increased deal stream within the subsequent quarter, sustaining a conservative funding method whereas supporting middle-market enterprise progress.

Supply: Investor Relations

Progress Prospects

Capital Southwest Company (CSWC) is positioned for sustained progress by strategic funding initiatives and a powerful monetary basis. In 2025, the corporate enhanced its liquidity with a $347.7 million senior unsecured word providing and secured a second SBIC license, offering entry to as much as $350 million in low-cost, SBA-guaranteed funding.

These strikes strengthen CSWC’s capability to pursue new investments, help portfolio progress, and handle refinancing wants effectively. Analysts at the moment preserve a “Purchase” ranking, with a consensus value goal of $23.50, indicating potential upside of almost 15% from present ranges.

Wanting forward, CSWC tasks $283.9 million in income and $196.4 million in earnings by 2028, reflecting a ten.7% annual income progress charge. The corporate’s constant capacity to generate robust pre-tax internet funding revenue, coupled with its conservative underwriting and versatile financing mannequin, positions it to capitalize on rising alternatives within the decrease and higher middle-market segments whereas delivering long-term worth to shareholders.

Supply: Investor Relations

Aggressive Benefits & Recession Efficiency

Capital Southwest Company (CSWC) leverages its aggressive benefits as an internally managed BDC by offering versatile debt and fairness options to middle-market corporations. Its give attention to first-lien senior secured debt, conservative underwriting, and entry to SBIC licenses and an Fairness ATM program provides it monetary flexibility and the power to behave shortly on new funding alternatives.

The corporate has demonstrated resilience throughout financial downturns, with non-accruals accounting for lower than 1% of its portfolio and a conservative debt-to-EBITDA ratio of three.4 instances. By concentrating on secure middle-market companies, CSWC constantly maintains dividends and internet funding revenue, demonstrating a defensive and dependable enterprise mannequin.

The corporate carried out effectively throughout the earlier main financial downturn, the Nice Recession of 2008-2009:

- 2008 earnings-per-share: $0.24

- 2009 earnings-per-share: $0.68

- 2010 earnings-per-share: $4.91

Dividend Evaluation

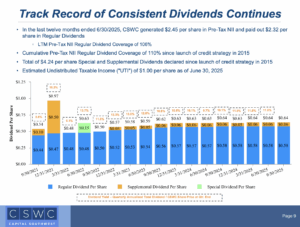

The corporate’s annual dividend is $2.32 per share. At its latest share value, the inventory has a excessive yield of 10.0%. This excludes some small particular dividends the corporate has declared.

Given the corporate’s earnings outlook for 2025, NII is predicted to be $2.35 per share. Because of this, the corporate is predicted to pay out 99% of its NII to shareholders in dividends.

Supply: Investor Relations

Closing Ideas

Capital Southwest is a well-diversified and long-established enterprise growth firm that has efficiently navigated a number of market cycles. Since its 2015 spinoff, the corporate’s financials have grown steadily, supported by low-cost financing and disciplined portfolio growth.

We challenge medium-term annualized returns of 9.5%, excluding supplemental dividends, pushed by its robust dividend yield and progress. Nonetheless, the inventory is rated a maintain.

Excessive-Yield Particular person Safety Analysis

Different Positive Dividend Assets

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

{kind=link}