Revealed on December thirty first, 2024 by Bob Ciura

Excessive yield securities are considered primarily as revenue turbines. However much less consideration is paid to their potential to compound revenue over time.

There are three drivers for compounding revenue from any funding:

- Reinvesting dividends

- Dividend development on a per share foundation

- The time over which the funding is held

Reinvesting dividends is particularly highly effective with high-yield securities. Larger yields imply you could compound your revenue stream sooner by reinvesting dividends.

If all dividends from a 5.0% yielding inventory are reinvested, you’ll compound your revenue stream at roughly 5.0% yearly.

And since excessive yield shares, on common, don’t have significantly excessive development charges, you may “create” revenue development by reinvesting dividends till you want them for private finance causes.

We keep an inventory of high-dividend shares with present yields above 5%. You’ll be able to obtain the excessive dividend shares listing by clicking on the hyperlink beneath:

There are numerous excessive yield securities on the market. However it’s non as frequent for a high-yield safety to pay rising dividends on a per share foundation over time.

When this occurs, your revenue compounds, even while you don’t reinvest dividends.

However in the event you do reinvest dividends, you get compounding advantages from each proudly owning extra shares (by means of reinvesting dividends), and receiving extra revenue from every share (from dividend development on a per share foundation).

Subsequently, discovering shares with a excessive present yield with dividend will increase, generally is a highly effective mixture.

The next 10 excessive yield dividend compounders have present yields above 5%, and Dividend Danger Scores of ‘C’ or higher. The listing additionally excludes REITs, BDCs, and MLPs.

Desk of Contents

The ten excessive yield dividend compounders are ranked by 5-year dividend development price, from lowest to highest.

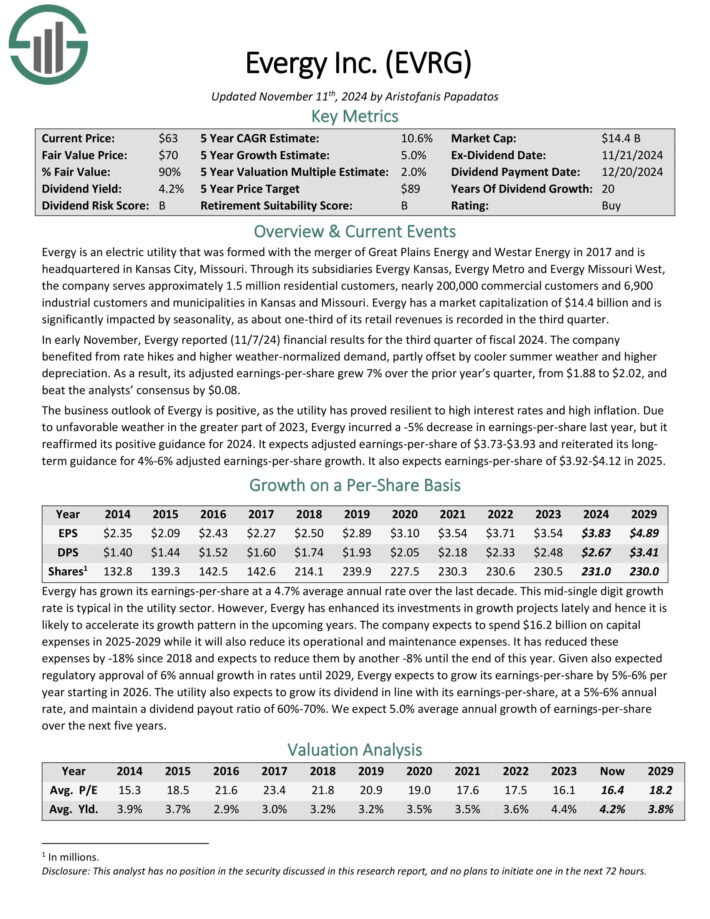

Excessive Yield Dividend Compounder #10: Evergy Inc. (EVRG)

- Dividend Yield: 4.3%

- Dividend Progress Fee: 5.0%

Evergy is an electrical utility holding firm integrated in 2017 and headquartered in Kansas Metropolis, Missouri.

Via its subsidiaries Evergy Kansas, Evergy Metro and Evergy Missouri West, the corporate serves roughly 1.4 million residential clients, almost 200,000 business clients and 6,900 industrial clients and municipalities in Kansas and Missouri.

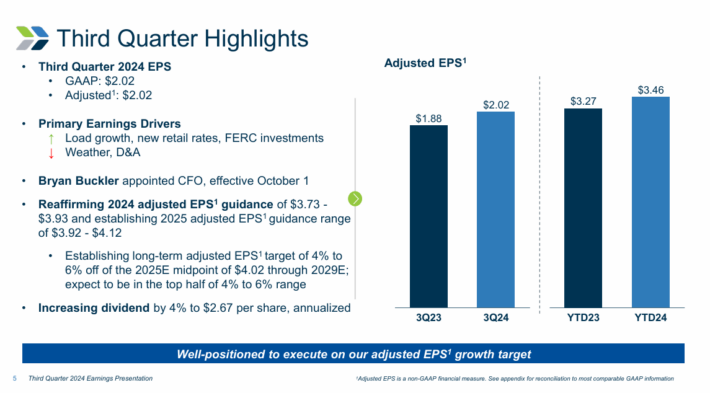

In early November, Evergy reported (11/7/24) monetary outcomes for the third quarter of fiscal 2024. The corporate benefited from price hikes and better weather-normalized demand, partly offset by cooler summer time climate and better depreciation.

Supply: Investor Presentation

Adjusted earnings-per-share grew 7% year-over-year. Evergy reaffirmed its optimistic steerage for 2024. It expects adjusted earnings-per-share of $3.73-$3.93 and reiterated its long-term steerage for 4%-6% adjusted earnings-per-share development.

It additionally expects earnings-per-share of $3.92-$4.12 in 2025.

Click on right here to obtain our most up-to-date Positive Evaluation report on Evergy Inc. (preview of web page 1 of three proven beneath):

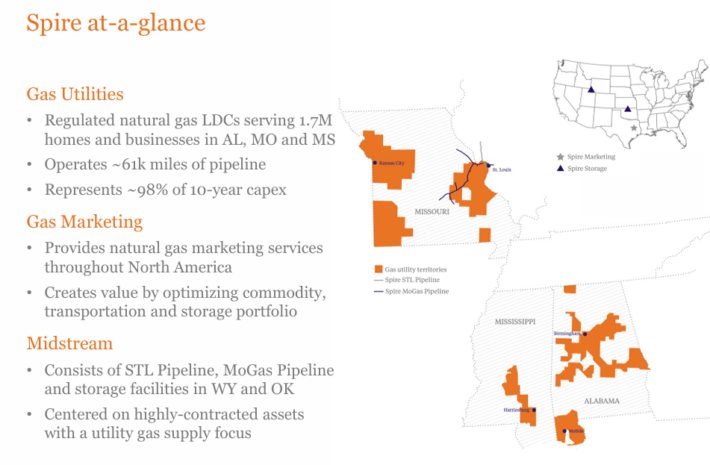

Excessive Yield Dividend Compounder #9: Spire Inc. (SR)

- Dividend Yield: 6.2%

- Dividend Danger Rating: B

Spire Inc. is a public utility holding firm based mostly in St. Louis, Missouri. The corporate gives pure gasoline service by means of its regulated core utility operations whereas participating in non-regulated actions that present enterprise alternatives.

The corporate has 5 gasoline utilities, serving 1.7 million houses and companies throughout Alabama, Mississippi, and Missouri. This makes Spire the fifth largest publicly traded pure gasoline firm within the nation.

Supply: Investor Presentation

The corporate generated $2.6 billion in gross sales in Fiscal Yr (FY)2024. Spire has been rising its dividends for 22 straight years.

On November twentieth., 2024, the corporate reported its FY2024 fourth quarter outcomes. The corporate reported a internet revenue of $250.9 million ($4.19 per share), up from $217.5 million ($3.85 per share) in fiscal 2023.

Adjusted earnings reached $247.4 million ($4.13 per share), bettering from $228.1 million ($4.05 per share) the earlier 12 months.

The corporate reaffirmed its long-term adjusted earnings development goal of 5–7% and supplied fiscal 2025 earnings steerage of $4.40 to $4.60 per share.

Click on right here to obtain our most up-to-date Positive Evaluation report on SR (preview of web page 1 of three proven beneath):

Excessive Yield Dividend Compounder #8: Flowers Meals, Inc. (FLO)

- Dividend Yield: 4.7%

- Dividend Progress Fee: 5.1%

Flowers Meals opened its first bakery in 1919 and has since develop into one of many largest producers of packaged bakery meals in the USA, working 46 bakeries in 18 states.

Its well-known manufacturers embody Marvel Bread, Residence Delight, Nature’s Personal, Dave’s Killer Bread, Tastykake and Canyon Bakehouse.

The corporate operates in two segments: Direct Retailer-Supply (DSD) and Warehouse Supply, with ~85% of the corporate’s product being delivered on to shops.

Supply: Investor Presentation

Recent breads, buns, rolls, and tortillas make up a few three-fourths of the enterprise, with gross sales channels for the corporate break up between Supermarkets, Mass Merchandisers, Foodservice, and Comfort Retailer.

On Could twenty third, 2024, Flower Meals elevated its quarterly dividend 4.3% to $0.24, extending the corporate’s dividend development streak to 22 consecutive years.

On November eighth, 2024, Flowers Meals reported third quarter outcomes for the interval ending October fifth, 2024. For the quarter, income of $1.19 billion was down 0.8% from the prior 12 months. Adjusted earnings-per-share equaled $0.33, up from $0.29 in the identical quarter final 12 months.

Flowers Meals supplied an up to date outlook for 2024 as properly. For the 12 months, income is predicted in a spread of $5.116 billion to $5.147 billion. Adjusted earnings-per-share are anticipated to be in a spread of $1.24 to $1.28.

Click on right here to obtain our most up-to-date Positive Evaluation report on FLO (preview of web page 1 of three proven beneath):

Excessive Yield Dividend Compounder #7: RGC Sources, Inc. (RGCO)

- Dividend Yield: 4.2%

- Dividend Progress Fee: 5.2%

RGC Sources, Inc. operates as a distributor and vendor of pure gasoline to industrial, business, and residential clients by means of its subsidiaries: Roanoke Fuel, Midstream, and Diversified Power.

Residential clients are the corporate’s largest buyer phase, accounting for ~58% of the whole revenues, adopted by business clients at 34%.

The corporate operates in three segments: Fuel Utility, the important thing income generator; Funding in Associates; and Father or mother & Different. The corporate was based in 1883 and generates just below $100 million in annual income.

On November 14th, 2024, RGC Sources introduced its This autumn 2024 outcomes. The corporate posted non-GAAP EPS of $0.01, beating the market’s estimate by $0.02, and whole revenues of $13.10 million, which have been up 5.11% 12 months over 12 months.

The earnings development was pushed by greater contributions from the Mountain Valley Pipeline (MVP), primarily from Allowance for Funds Used Throughout Building (AFUDC) earlier than the pipeline commenced operations in June 2024.

Click on right here to obtain our most up-to-date Positive Evaluation report on RGCO (preview of web page 1 of three proven beneath):

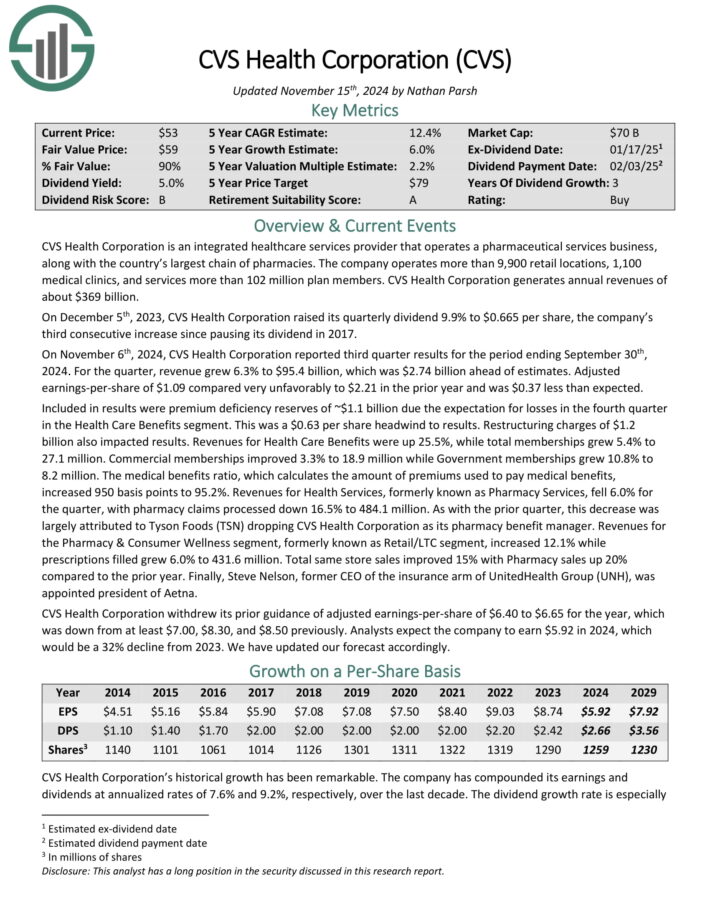

Excessive Yield Dividend Compounder #6: CVS Well being Corp. (CVS)

- Dividend Yield: 6.1%

- Dividend Progress Fee: 6.0%

CVS Well being Company is an built-in healthcare companies supplier that operates a pharmaceutical companies enterprise, together with the nation’s largest chain of pharmacies.

The corporate operates greater than 9,900 retail areas, 1,100 medical clinics, and companies greater than 102 million plan members. CVS Well being Company generates annual revenues of about $369 billion.

On November sixth, 2024, CVS Well being Company reported third quarter outcomes for the interval ending September thirtieth, 2024. For the quarter, income grew 6.3% to $95.4 billion, which was $2.74 billion forward of estimates. Adjusted earnings-per-share of $1.09 in contrast very unfavorably to $2.21 within the prior 12 months and was $0.37 lower than anticipated.

Included in outcomes have been premium deficiency reserves of ~$1.1 billion due the expectation for losses within the fourth quarter within the Well being Care Advantages phase.

This was a $0.63 per share headwind to outcomes. Restructuring expenses of $1.2 billion additionally impacted outcomes. Revenues for Well being Care Advantages have been up 25.5%, whereas whole memberships grew 5.4% to 27.1 million.

Click on right here to obtain our most up-to-date Positive Evaluation report on CVS (preview of web page 1 of three proven beneath):

Excessive Yield Dividend Compounder #5: Eversource Power (ES)

- Dividend Yield: 5.0%

- Dividend Progress Fee: 6.0%

Eversource Power is a diversified holding firm with subsidiaries that present regulated electrical, gasoline, and water distribution service within the Northeast U.S.

The corporate’s utilities serve greater than 4 million clients after buying NStar’s Massachusetts utilities in 2012, Aquarion in 2017, and Columbia Fuel in 2020.

Eversource has delivered regular development to shareholders for a few years.

Supply: Investor Presentation

On November 4th, 2024, Eversource Power launched its third-quarter 2024 outcomes for the interval ending September thirtieth, 2024.

For the quarter, the corporate reported a internet lack of $(118.1) million, a pointy decline from earnings of $339.7 million in the identical quarter of final 12 months, which displays the impression of the corporate’s exit from offshore wind investments.

The corporate reported a loss per share of $(0.33), in contrast with earnings-per-share of $0.97 within the prior 12 months. Earnings from the Electrical Transmission phase elevated to $174.9 million, up from $160.3 million within the prior 12 months, primarily as a consequence of a better stage of funding in Eversource’s electrical transmission system.

Click on right here to obtain our most up-to-date Positive Evaluation report on ES (preview of web page 1 of three proven beneath):

Excessive Yield Dividend Compounder #4: Portland Basic Electrical (POR)

- Dividend Yield: 4.6%

- Dividend Progress Fee: 6.0%

Portland Basic Electrical is an electrical utility based mostly in Portland, Oregon, offering electrical energy to greater than 930,000 clients in 51 cities. The corporate owns or contracts greater than 3.5 gigawatts of power era, between gasoline, coal, wind & photo voltaic, and hydro.

On April nineteenth, 2024, Portland Basic Electrical introduced a 5% improve within the quarterly dividend to $0.50 per share.

Portland Basic reported third quarter 2024 outcomes on October twenty fifth, 2024. The corporate reported internet revenue of $94 million for the quarter, equal to $0.90 per diluted share on a GAAP foundation, in comparison with $0.46 in Q3 2023.

Retail power deliveries rose 0.3% year-to-date in comparison with the identical prior 12 months interval, however wholesale power deliveries soared 45%. Consequently, whole power deliveries rose 11%.

Management narrowed its 2024 full 12 months steerage for adjusted earnings per share to $3.13 on the midpoint based mostly on a collection of assumptions, most notably a 2.5% improve in annual power deliveries.

Click on right here to obtain our most up-to-date Positive Evaluation report on Portland Basic Electrical Firm (preview of web page 1 of three proven beneath):

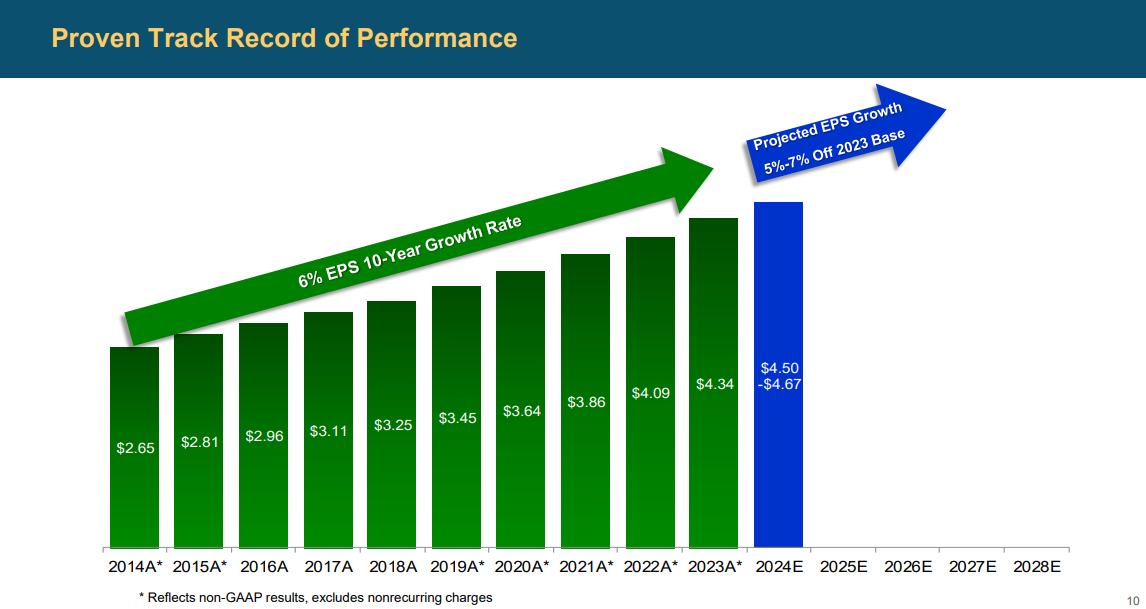

Excessive Yield Dividend Compounder #3: Interpublic Group of Cos. (IPG)

- Dividend Yield: 4.7%

- Dividend Progress Fee: 6.5%

The Interpublic Group of Firms, Inc. gives promoting and advertising companies worldwide. Its operations are properly arrayed amongst client promoting, digital advertising, communications planning, media shopping for, and knowledge administration companies.

On October twenty second, 2024, Interpublic reported its Q3 outcomes for the interval ending September thirtieth, 2024. For the interval, internet revenues got here in at $2.24 billion, down 2.9% in comparison with final 12 months.

This was derived from a damaging 0.5% foreign money translation impact and a damaging impression of two.4% from inclinations, offset by natural development of 1.0%.

The corporate noticed strong contributions to development from media companies, sports activities advertising, knowledge administration and public relations.

Adjusted EPS was $0.70, flat in comparison with final 12 months. Yr-to-date, the corporate repurchased $230.1 million value of inventory, which barely aided EPS.

Click on right here to obtain our most up-to-date Positive Evaluation report on IPG (preview of web page 1 of three proven beneath):

Excessive Yield Dividend Compounder #2: FMC Corp. (FMC)

- Dividend Yield: 4.8%

- Dividend Progress Fee: 7.0%

FMC Company is an agricultural sciences firm that gives crop safety, plant well being, {and professional} pest and turf administration merchandise. Via acquisitions, FMC is now one of many 5 largest patented crop chemical firms.

The corporate markets its merchandise by means of its personal gross sales group and thru alliance companions, unbiased distributors, and gross sales representatives. It operates in North America, Latin America, Europe, the Center East, Africa, and Asia.

On October twenty ninth, 2024, FMC Company launched its third quarter outcomes for the interval ending September thirtieth, 2024.

For the quarter, the corporate reported income of $1.07 billion, up 9% versus the third quarter of 2023, and adjusted earnings per diluted share of $0.69, up 57% versus the identical quarter of the earlier 12 months.

Quarterly income development was primarily pushed by a 17% improve in quantity, significantly sturdy in North America and Latin America, regardless of dealing with a 5% decline from value decreases as a consequence of difficult market circumstances and a 3% overseas trade headwind.

Click on right here to obtain our most up-to-date Positive Evaluation report on FMC (preview of web page 1 of three proven beneath):

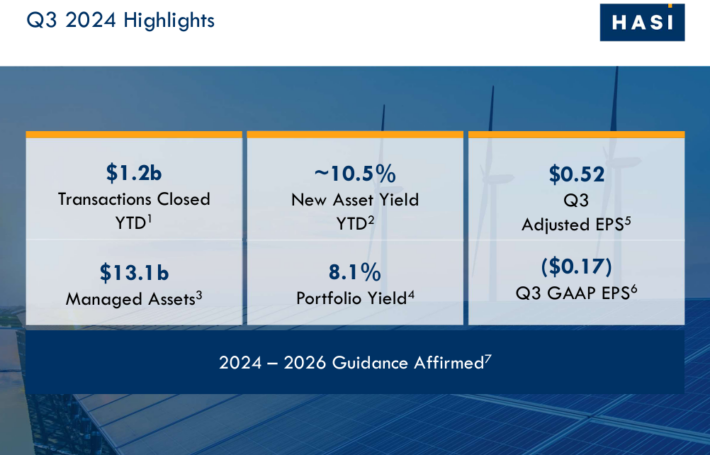

Excessive Yield Dividend Compounder #1: HA Sustainable Infrastructure Capital (HASI)

- Dividend Yield: 6.2%

- Dividend Progress Fee: 7.0%

Hannon Armstrong is a U.S. public firm that invests in local weather change options, offering capital to main firms in power effectivity, renewable power, and different sustainable infrastructure markets.

The corporate’s portfolio of belongings is value round $13.1 billion and is break up between three market segments: Its Behind the Meter enterprise (46% of belongings) focuses on the set up of solar energy, electrical storage, and different warmth and energy programs.

The Grid-Linked phase (30% of belongings) entails investments in grid-connected renewable power tasks, equivalent to photo voltaic and off/on-shore wind tasks, whose generated yield the corporate then sells on the wholesale power markets.

Lastly, occupying the remainder of its portfolio (24% of belongings), are the corporate’s Fuels, Transport, & Nature tasks, enabling the usage of pure assets, equivalent to its tasks to gradual air pollution runoff throughout the Chesapeake Bay area.

Supply: Investor Presentation

On November seventh, 2024, Hannon Armstrong reported its Q3 outcomes for the interval ending September thirtieth, 2024. For the quarter, whole revenues fell by 8.5% year-over-year to about $82 million.

The drop in revenues was primarily as a consequence of decrease rental revenue as a consequence of asset gross sales in addition to decrease features on belongings bought in comparison with final 12 months.

Adjusted EPS fell by 16% to $0.52 in comparison with the prior-year interval. The drop was primarily as a consequence of decrease revenues, offset partially by development in adjusted internet funding revenue as a consequence of a bigger portfolio.

The corporate’s pipeline remained sturdy, together with $5.5 billion of asset alternatives. Administration affirmed its prior outlook, anticipating to ship adjusted EPS CAGR between 8% and 10% by means of 2026.

Click on right here to obtain our most up-to-date Positive Evaluation report on HASI (preview of web page 1 of three proven beneath):

Extra Studying

Traders ought to proceed to watch every inventory to ensure their fundamentals and development stay on observe, significantly amongst shares with extraordinarily excessive dividend yields.

See the assets beneath to generate further compelling funding concepts for dividend development shares and/or high-yield funding securities.

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

{kind=link}