Printed on December twenty sixth, 2025 by Bob Ciura

Conservative retirement investing is all about creating passive earnings with high quality securities held for the long-run.

At Positive Dividend, we give attention to dividend paying shares to construct a rising and dependable passive earnings stream. The Dividend Kings are an ideal instance of this.

The Dividend Kings have elevated their dividends for at the very least 50 consecutive years.

You’ll be able to see the complete downloadable spreadsheet of all 56 Dividend Kings (together with vital monetary metrics reminiscent of dividend yields, payout ratios, and price-to-earnings ratios) by clicking on the hyperlink under:

Conservative buyers will naturally be drawn to larger high quality companies much less more likely to cut back their dividend funds throughout recessions.

And once you make investments conservatively for earnings you get to revenue from market volatility by selecting once you purchase and promote as an alternative of letting the market dictate your strikes.

Choosing precisely what to put money into can get difficult, nevertheless it doesn’t need to.

The ten prime retirement earnings shares under are Dividend Kings primarily based within the U.S., with present yields above 2.5%, equal to double the present dividend yield of the S&P 500 Index.

The ten shares are ranked by dividend yield under.

Desk of Contents

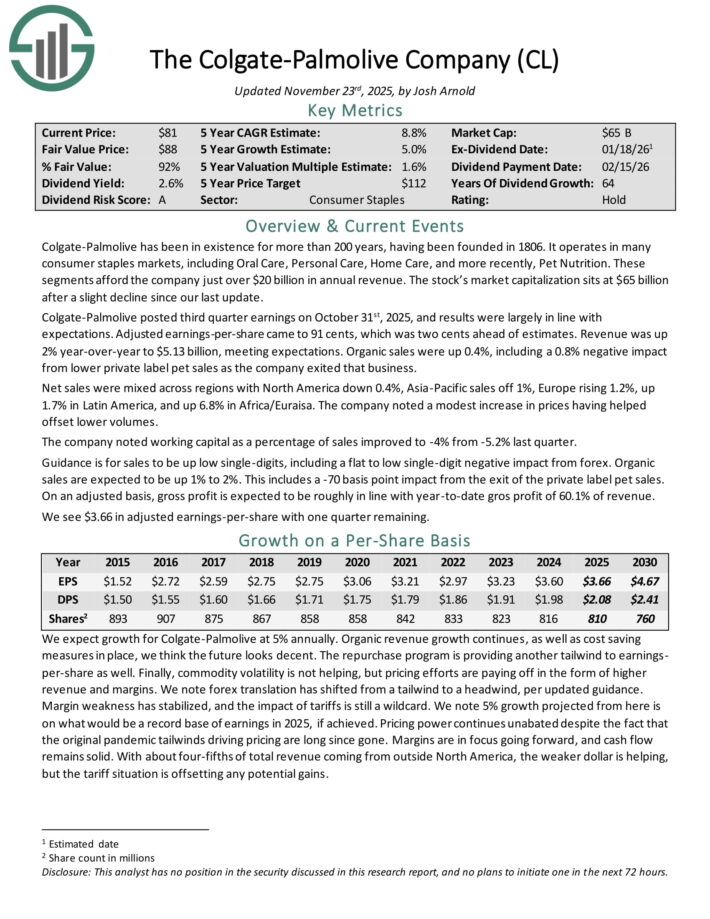

Conservative Retirement Revenue Inventory: Colgate-Palmolive Co. (CL)

Colgate-Palmolive has been in existence for greater than 200 years, having been based in 1806. It operates in lots of client staples markets, together with Oral Care, Private Care, House Care, and extra not too long ago, Pet Diet.

These segments afford the corporate simply over $20 billion in annual income.

Colgate-Palmolive posted third quarter earnings on October thirty first, 2025, and outcomes have been largely in keeping with expectations. Adjusted earnings-per-share got here to 91 cents, which was two cents forward of estimates.

Income was up 2% year-over-year to $5.13 billion, assembly expectations. Natural gross sales have been up 0.4%, together with a 0.8% unfavourable affect from decrease non-public label pet gross sales as the corporate exited that enterprise.

Web gross sales have been combined throughout areas with North America down 0.4%, Asia-Pacific gross sales off 1%, Europe rising 1.2%, up 1.7% in Latin America, and up 6.8% in Africa/Euraisa. The corporate famous a modest enhance in costs having helped offset decrease volumes.

The corporate famous working capital as a share of gross sales improved to -4% from -5.2% final quarter. Steering is for gross sales to be up low single-digits, together with a flat to low single-digit unfavourable affect from foreign exchange. Natural gross sales are anticipated to be up 1% to 2%.

Click on right here to obtain our most up-to-date Positive Evaluation report on CL (preview of web page 1 of three proven under):

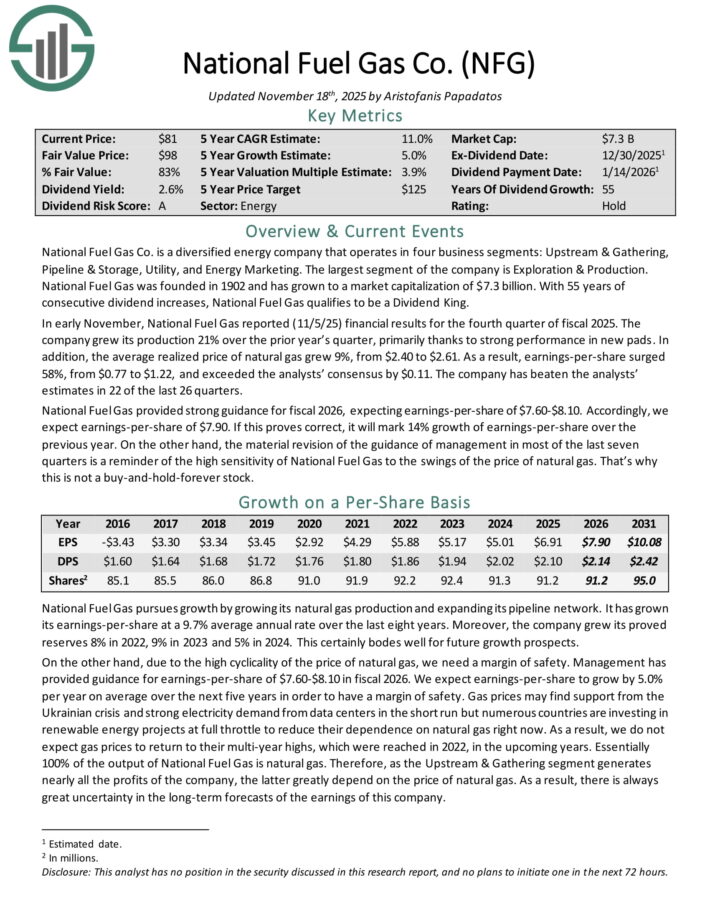

Conservative Retirement Revenue Inventory: Nationwide Gasoline Fuel (NFG)

Nationwide Gasoline Fuel Co. is a diversified power firm that operates in 4 enterprise segments: Upstream & Gathering, Pipeline & Storage, Utility, and Power Advertising and marketing.

The biggest section of the corporate is Exploration & Manufacturing. With 55 years of consecutive dividend will increase, Nationwide Gasoline Fuel qualifies to be a Dividend King.

In early November, Nationwide Gasoline Fuel reported (11/5/25) monetary outcomes for the fourth quarter of fiscal 2025. The corporate grew its manufacturing 21% over the prior yr’s quarter, primarily due to sturdy efficiency in new pads.

As well as, the typical realized value of pure fuel grew 9%, from $2.40 to $2.61. Consequently, earnings-per-share surged 58%, from $0.77 to $1.22, and exceeded the analysts’ consensus by $0.11.

The corporate has overwhelmed the analysts’ estimates in 22 of the final 26 quarters. Nationwide Gasoline Fuel supplied sturdy steering for fiscal 2026, anticipating earnings-per-share of $7.60-$8.10.

Accordingly, we anticipate earnings-per-share of $7.90. If this proves right, it’ll mark 14% development of earnings-per-share over the earlier yr.

Click on right here to obtain our most up-to-date Positive Evaluation report on NFG (preview of web page 1 of three proven under):

Conservative Retirement Revenue Inventory: Procter & Gamble Co. (PG)

Procter & Gamble is a client merchandise large that sells its merchandise in over 180 international locations. Notable manufacturers embody Pampers, Luvs, Tide, Achieve, Bounty, Charmin, Puffs, Gillette, Head & Shoulders, Outdated Spice, Daybreak, Febreze, Swiffer, Crest, Oral-B, Scope, Olay and lots of extra.

The corporate generated $84 billion in gross sales in fiscal 2024 and 2025. Procter & Gamble has paid a dividend for 134 years and has grown its dividend for 69 consecutive years – one of many longest lively streaks of any firm.

In late October, Procter & Gamble reported (10/24/25) outcomes for the primary quarter of fiscal 2025 (its fiscal yr ends June thirtieth). Its gross sales and natural gross sales grew 3% and a pair of%, respectively, over final yr’s quarter, due to larger costs and a good mixture of merchandise.

Core earnings-per-share grew 3%, from $1.93 to $1.99, beating the analysts’ consensus by $0.09. The agency gross sales amid sustained value hikes are a testomony to the power of the manufacturers of Procter & Gamble.

Nonetheless, we observe a outstanding deceleration in value hikes within the final six quarters. This means that the corporate can not maintain elevating its costs aggressively anymore.

Because of mushy client spending amid elevated financial uncertainty, Procter & Gamble reiterated its modest steering for fiscal 2026. It expects 0%-4% development of natural gross sales and 0%-4% development of core earnings-per-share.

Click on right here to obtain our most up-to-date Positive Evaluation report on PG (preview of web page 1 of three proven under):

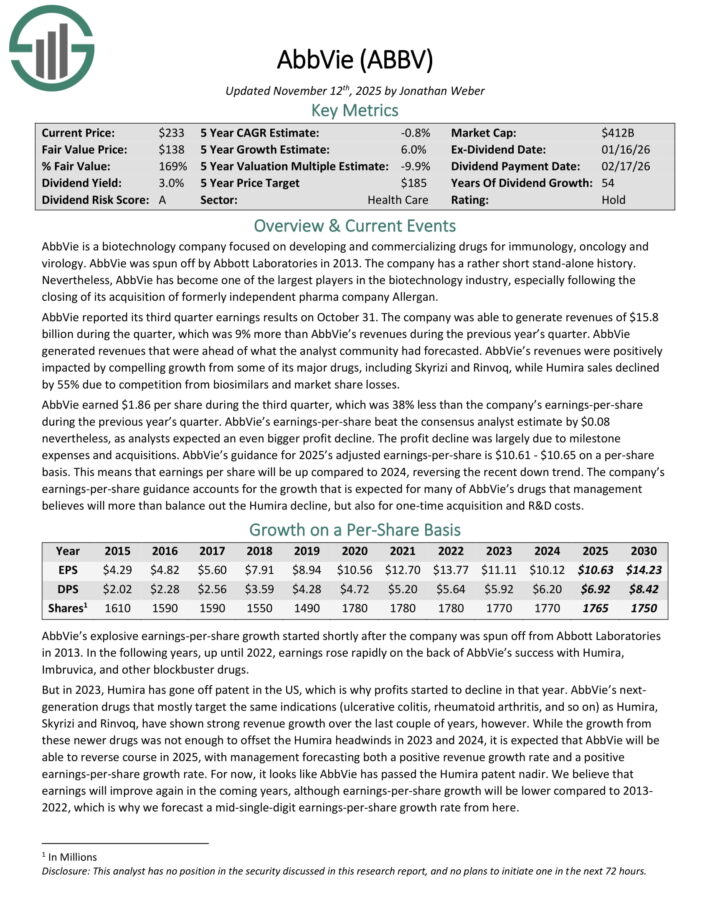

Conservative Retirement Revenue Inventory: AbbVie Inc. (ABBV)

AbbVie is a biotechnology firm targeted on growing and commercializing medicine for immunology, oncology and virology. It was spun off by Abbott Laboratories in 2013 and has turn into one of many largest gamers within the biotechnology trade.

AbbVie reported its third quarter earnings outcomes on October 31. The corporate was in a position to generate revenues of $15.8 billion throughout the quarter, which was 9% year-over-year development.

Income was positively impacted by compelling development from a few of its main medicine, together with Skyrizi and Rinvoq, whereas Humira gross sales declined by 55% attributable to competitors from biosimilars and market share losses.

AbbVie earned $1.86 per share throughout the third quarter, which was 38% lower than the corporate’s earnings-per-share throughout the earlier yr’s quarter.

Earnings-per-share beat the consensus analyst estimate by $0.08. Steering for 2025 adjusted earnings-per-share is $10.61 – $10.65.

Click on right here to obtain our most up-to-date Positive Evaluation report on ABBV (preview of web page 1 of three proven under):

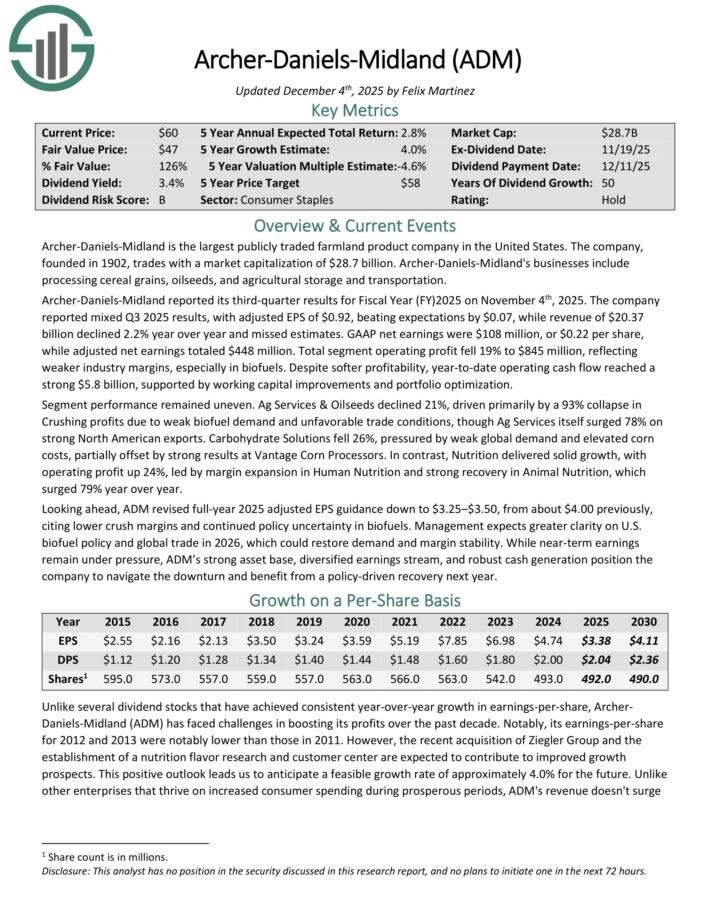

Conservative Retirement Revenue Inventory: Archer Daniels Midland (ADM)

Archer-Daniels-Midland is the most important publicly traded farmland product firm in america. Its companies embody processing cereal grains, oilseeds, and agricultural storage and transportation.

Archer-Daniels-Midland reported its third-quarter outcomes for Fiscal 12 months (FY)2025 on November 4th, 2025. The corporate reported combined Q3 2025 outcomes, with adjusted EPS of $0.92, beating expectations by $0.07, whereas income of $20.37 billion declined 2.2% yr over yr and missed estimates.

Complete section working revenue fell 19% to $845 million, reflecting weaker trade margins, particularly in biofuels. Regardless of softer profitability, year-to-date working money circulation reached a powerful $5.8 billion, supported by working capital enhancements and portfolio optimization.

Section efficiency remained uneven. Ag Providers & Oilseeds declined 21%, pushed primarily by a 93% collapse in Crushing income attributable to weak biofuel demand and unfavorable commerce situations, although Ag Providers itself surged 78% on sturdy North American exports.

Carbohydrate Options fell 26%, pressured by weak world demand and elevated corn prices, partially offset by sturdy outcomes at Vantage Corn Processors.

Wanting forward, ADM revised full-year 2025 adjusted EPS steering all the way down to $3.25–$3.50.

Click on right here to obtain our most up-to-date Positive Evaluation report on ADM (preview of web page 1 of three proven under):

Conservative Retirement Revenue Inventory: PepsiCo Inc. (PEP)

PepsiCo is a worldwide meals and beverage firm that generates $89 billion in annual gross sales. The corporate’s merchandise embody Pepsi, Mountain Dew, Frito-Lay chips, Gatorade, Tropicana orange juice and Quaker meals.

The corporate has greater than 20 $1 billion manufacturers in its portfolio. On February 4th, 2025, PepsiCo elevated its annualized dividend by 5.0% to $5.69 beginning with the fee that was made in June 2025, extending the corporate’s dividend development streak to 53 consecutive years.

On October ninth, 2025, PepsiCo reported third quarter earnings outcomes for the interval ending September thirtieth, 2025. For the quarter, income grew 2.7% to $23.9 billion, which beat estimates by $90 million. Adjusted earnings-per-share of $2.29 in contrast unfavorably to $2.31 the prior yr, however this was $0.03 higher than anticipated.

Natural gross sales grew 1.3% for the third quarter. For the interval, volumes for each drinks and meals have been down 1%. PepsiCo Drinks North America’s natural income grew 2% for the interval at the same time as quantity declined by 3%.

Income for PepsiCo Meals North America decreased 3%, largely attributable to divestitures. Meals quantity decreased 4%. The Worldwide Drinks section fell 1%, primarily attributable to decrease quantity. Revenues in Europe/Center East/Africa have been up 5.5%. Meals quantity declined 1%, however this was offset by a 1.5% acquire in drinks.

PepsiCo reaffirmed prior steering for 2025, with the corporate nonetheless anticipating natural gross sales within the low single-digit vary.

Click on right here to obtain our most up-to-date Positive Evaluation report on PEP (preview of web page 1 of three proven under):

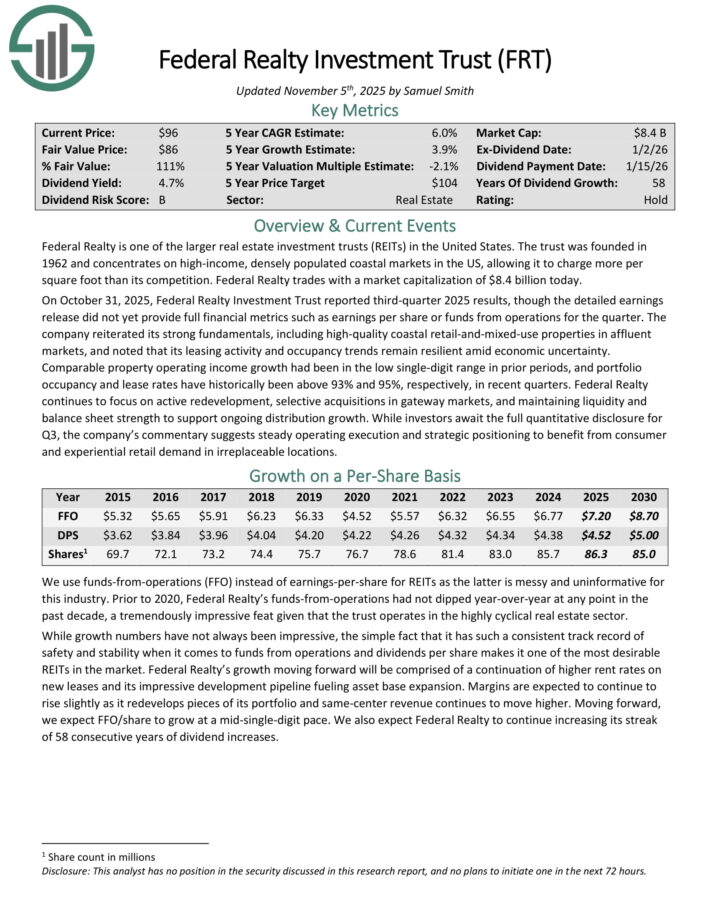

Conservative Retirement Revenue Inventory: Federal Realty Funding Belief (FRT)

Federal Realty is without doubt one of the bigger actual property funding trusts (REITs) in america. The belief was based in 1962 and concentrates on high-income, densely populated coastal markets within the US, permitting it to cost extra per sq. foot than its competitors.

On October 31, 2025, Federal Realty Funding Belief reported third-quarter 2025 outcomes, although the detailed earnings launch didn’t but present full monetary metrics reminiscent of earnings per share or funds from operations for the quarter.

The corporate reiterated its sturdy fundamentals, together with high-quality coastal retail-and-mixed-use properties in prosperous markets, and famous that its leasing exercise and occupancy tendencies stay resilient amid financial uncertainty.

Comparable property working earnings development had been within the low single-digit vary in prior durations, and portfolio occupancy and lease charges have traditionally been above 93% and 95%, respectively, in current quarters.

Click on right here to obtain our most up-to-date Positive Evaluation report on FRT (preview of web page 1 of three proven under):

Conservative Retirement Revenue Inventory: Hormel Meals (HRL)

Hormel Meals was based in 1891 in Minnesota. Since that point, the corporate has grown right into a $13 billion market capitalization juggernaut within the meals merchandise trade with about $12 billion in annual income.

Hormel has stored its core competency as a processor of meat merchandise for effectively over 100 years however has additionally grown into different enterprise strains via acquisitions.

The corporate sells its merchandise in 80 international locations worldwide, and its manufacturers embody Skippy, SPAM, Applegate, Justin’s, and greater than 30 others. As well as, Hormel is a member of the Dividend Kings, having elevated its dividend for 60 consecutive years.

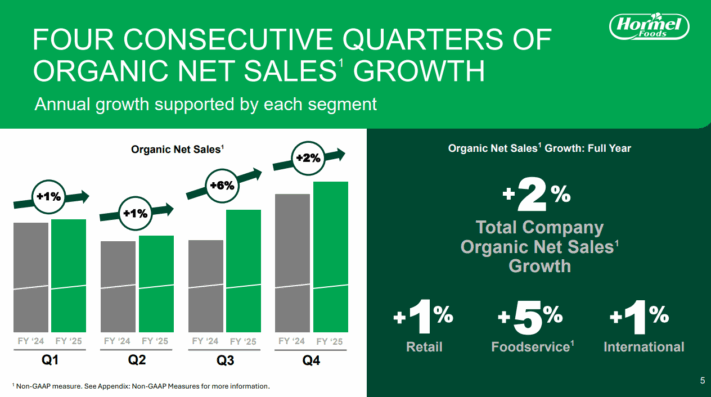

Hormel posted fourth quarter and full-year earnings on December 4th, 2025.

Supply: Investor Presentation

The corporate noticed 32 cents in adjusted earnings-per-share for the quarter, beating estimates by two cents. Income was up 1.6% year-over-year and missed estimates by $30 million, coming in at $3.19 billion.

Adjusted working margin was 7.7% of income, whereas money circulation from operations was $323 million. Volumes within the fourth quarter have been flat within the retail section, down 5% in foodservice, and down 7% within the worldwide section.

Hormel raised its dividend for the sixtieth consecutive yr, this time including 0.9% to a brand new payout of $1.20 per share yearly. We begin 2026 with an estimate of $1.47 in adjusted earnings-per-share.

Click on right here to obtain our most up-to-date Positive Evaluation report on HRL (preview of web page 1 of three proven under):

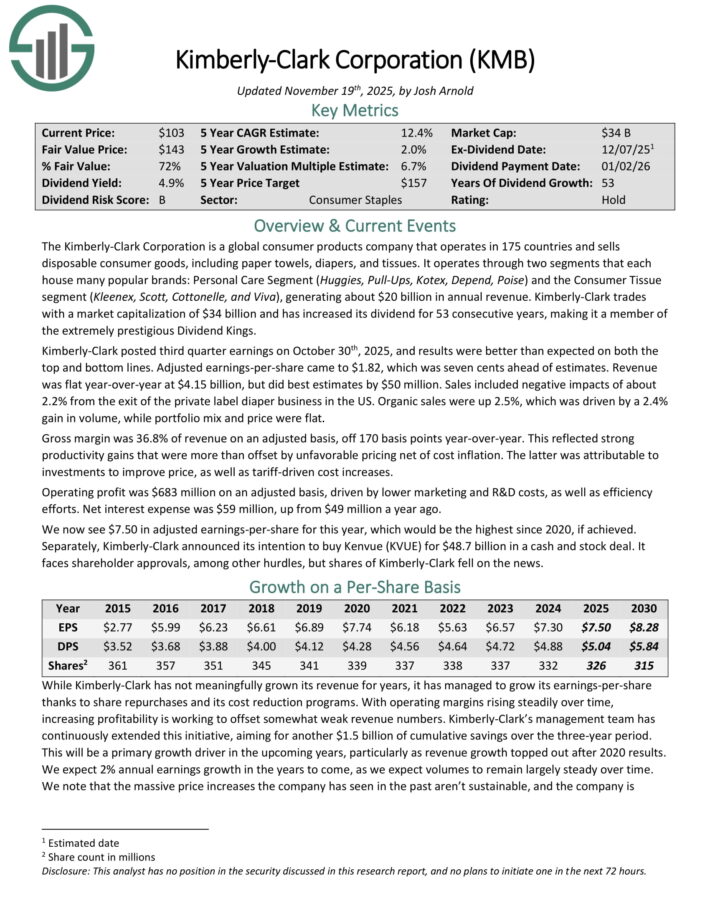

Conservative Retirement Revenue Inventory: Kimberly-Clark Corp. (KMB)

The Kimberly-Clark Company is a worldwide client merchandise firm that operates in 175 international locations and sells disposable client items, together with paper towels, diapers, and tissues.

It operates via two segments that every home many widespread manufacturers: Private Care Section (Huggies, Pull-Ups, Kotex, Rely, Poise) and the Shopper Tissue section (Kleenex, Scott, Cottonelle, and Viva), producing about $20 billion in annual income.

Kimberly-Clark trades with a market capitalization of $33 billion and has elevated its dividend for 53 consecutive years.

Kimberly-Clark posted third quarter earnings on October thirtieth, 2025, and outcomes have been higher than anticipated on each the highest and backside strains. Adjusted earnings-per-share got here to $1.82, which was seven cents forward of estimates.

Income was flat year-over-year at $4.15 billion, however did finest estimates by $50 million. Gross sales included unfavourable impacts of about 2.2% from the exit of the non-public label diaper enterprise within the US.

Natural gross sales have been up 2.5%, which was pushed by a 2.4% acquire in quantity, whereas portfolio combine and value have been flat.

On November third, 2025, it was introduced that Kimberly-Clark had agreed to buy Kenvue (KVUE) in a money and inventory deal valued at $48.7 billion. It will make the brand new firm a number one well being and wellness firm.

Click on right here to obtain our most up-to-date Positive Evaluation report on KMB (preview of web page 1 of three proven under):

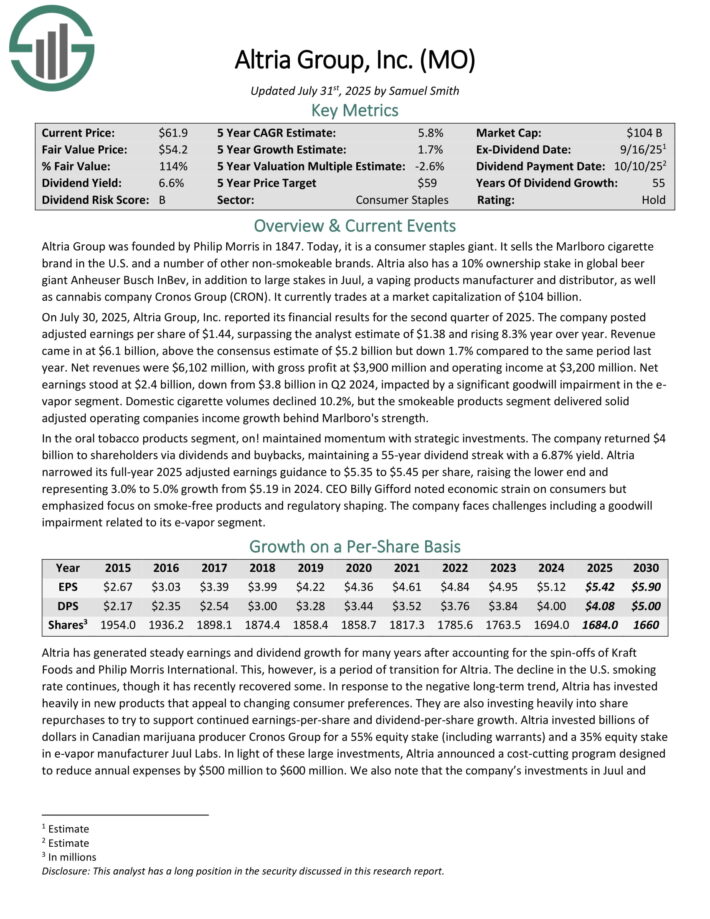

Conservative Retirement Revenue Inventory: Altria Group (MO)

Altria is a tobacco inventory that sells cigarettes, chewing tobacco, cigars, e-cigarettes, and extra below quite a lot of manufacturers, together with Marlboro, Skoal, and Copenhagen, amongst others.

This can be a interval of transition for Altria. The decline within the U.S. smoking price continues. In response, Altria has invested closely in new merchandise that enchantment to altering client preferences, because the smoke-free class continues to develop.

The corporate additionally has a 35% funding stake in e-cigarette maker JUUL, and a forty five% stake within the Canadian hashish producer Cronos Group (CRON).

On July 30, 2025, Altria Group, Inc. reported its monetary outcomes for the second quarter of 2025. The corporate posted adjusted earnings per share of $1.44, surpassing the analyst estimate of $1.38 and rising 8.3% yr over yr.

Income got here in at $6.1 billion, above the consensus estimate of $5.2 billion however down 1.7% in comparison with the identical interval final yr. Web revenues have been $6,102 million, with gross revenue at $3,900 million and working earnings at $3,200 million.

Web earnings stood at $2.4 billion, down from $3.8 billion in Q2 2024, impacted by a big goodwill impairment within the e-vapor section.

Home cigarette volumes declined 10.2%, however the smokeable merchandise section delivered strong adjusted working firms earnings development behind Marlboro’s power.

Click on right here to obtain our most up-to-date Positive Evaluation report on Altria (preview of web page 1 of three proven under):

Extra Assets

The Dividend Kings aren’t the one high-quality dividend development inventory concepts.

Positive Dividend maintains related databases on the next helpful universes of shares:

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

{kind=link}