Printed on January seventh, 2026 by Bob Ciura

Excessive dividend shares are engaging for revenue buyers. With the S&P 500 common yield at simply 1.1%, it has gotten more durable to seek out appropriate yields within the inventory market.

And with the Federal Reserve chopping rates of interest, revenue yields on financial savings accounts and CDs are more likely to decline as properly.

Fortuitously, there are nonetheless loads of high quality excessive dividend shares to select from. With that in thoughts, we now have created a free listing of over 200 excessive dividend shares with dividend yields above 5%.

You’ll be able to obtain your copy of the excessive dividend shares listing under:

Nevertheless, buyers ought to do not forget that extraordinarily excessive yields could be deceiving. There are lots of examples of excessive dividend shares decreasing or eliminating their dividends.

Because of this, buyers ought to search for excessive dividend shares that even have sustainable payouts. This implies buyers will obtain the advantages of excessive revenue for a few years.

The ten excessive dividend shares under had been discovered primarily based on a qualitative evaluation of their particular person enterprise fashions and future development prospects.

Desk of Contents

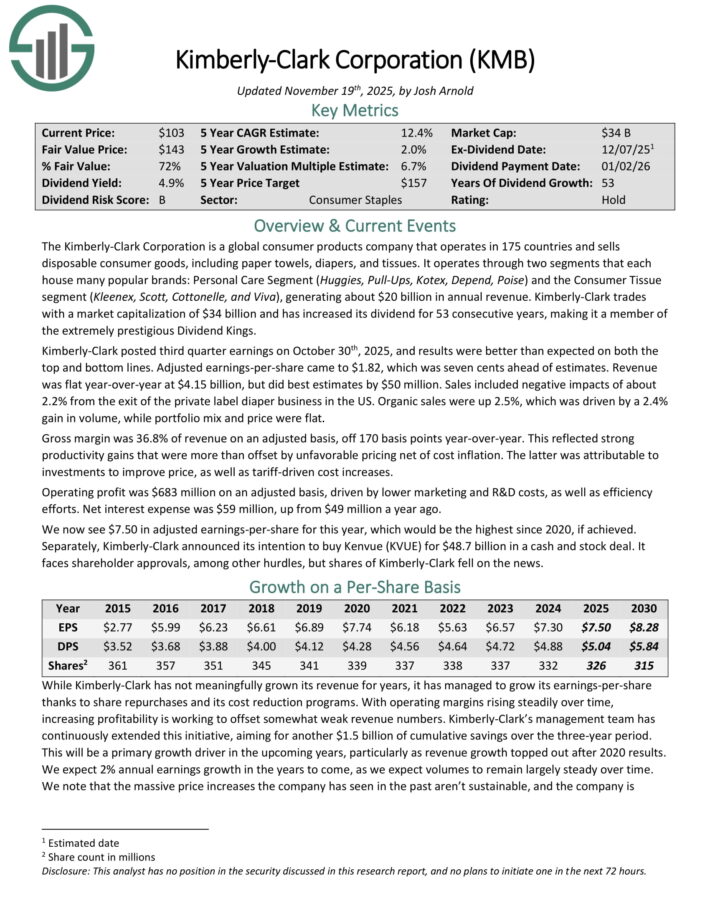

Excessive Dividend Inventory For The Lengthy Run #10: Kimberly-Clark Corp. (KMB)

The Kimberly-Clark Company is a world shopper merchandise firm that operates in 175 nations and sells disposable shopper items, together with paper towels, diapers, and tissues.

It operates by way of two segments that every home many standard manufacturers: Private Care Section (Huggies, Pull-Ups, Kotex, Rely, Poise) and the Shopper Tissue section (Kleenex, Scott, Cottonelle, and Viva), producing about $20 billion in annual income.

Kimberly-Clark has elevated its dividend for 53 consecutive years, making it a member of the Dividend Kings.

Kimberly-Clark posted third quarter earnings on October thirtieth, 2025, and outcomes had been higher than anticipated on each the highest and backside strains. Adjusted earnings-per-share got here to $1.82, which was seven cents forward of estimates.

Income was flat year-over-year at $4.15 billion, however did greatest estimates by $50 million. Gross sales included destructive impacts of about 2.2% from the exit of the personal label diaper enterprise within the US.

Natural gross sales had been up 2.5%, which was pushed by a 2.4% achieve in quantity, whereas portfolio combine and worth had been flat.

On November third, 2025, Kimberly-Clark agreed to buy Kenvue (KVUE) in a money and inventory deal valued at $48.7 billion. This can make the brand new firm a number one well being and wellness firm.

Click on right here to obtain our most up-to-date Certain Evaluation report on KMB (preview of web page 1 of three proven under):

Excessive Dividend Inventory For The Lengthy Run #9: Hormel Meals Corp. (HRL)

Hormel Meals was based in 1891 in Minnesota. Since that point, the corporate has grown right into a juggernaut within the meals merchandise business with about $12 billion in annual income.

The corporate sells its merchandise in 80 nations worldwide, and its manufacturers embody Skippy, SPAM, Applegate, Justin’s, and greater than 30 others.

As well as, Hormel is a member of the Dividend Kings, having elevated its dividend for 60 consecutive years.

Hormel posted fourth quarter and full-year earnings on December 4th, 2025. The corporate noticed 32 cents in adjusted earnings-per-share for the quarter, beating estimates by two cents.

Income was up 1.6% year-over-year and missed estimates by $30 million, coming in at $3.19 billion.

Hormel’s important aggressive benefit is its ~40 merchandise which are both #1 or #2 of their class. Hormel has manufacturers

which are confirmed, and that management place is tough for rivals to supplant.

Click on right here to obtain our most up-to-date Certain Evaluation report on HRL (preview of web page 1 of three proven under):

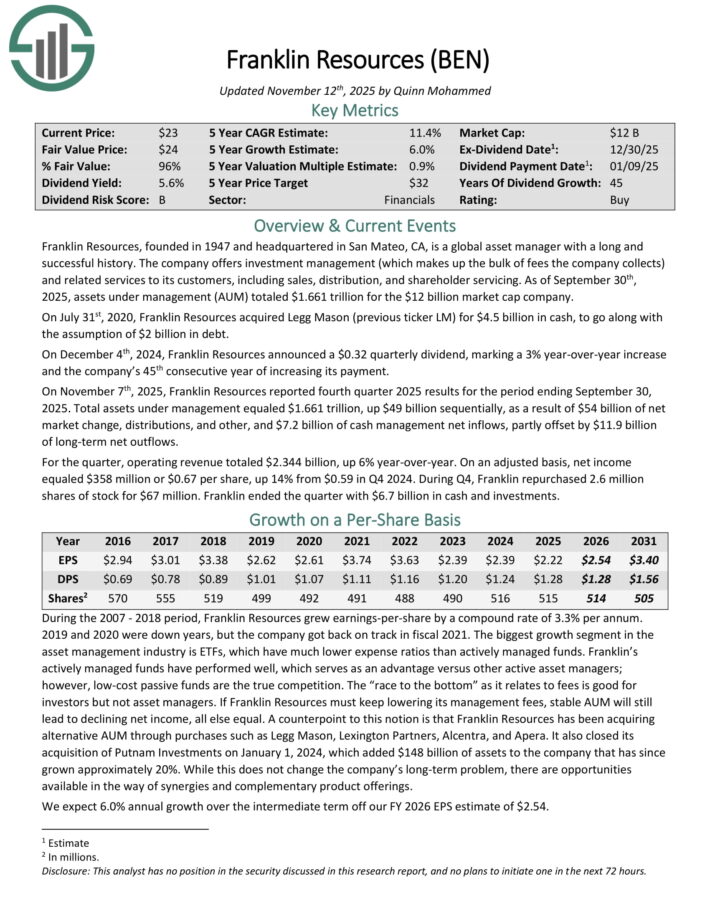

Excessive Dividend Inventory For The Lengthy Run #8: Franklin Sources (BEN)

Franklin Sources gives funding administration (which makes up the majority of charges the corporate collects) and associated providers to its prospects, together with gross sales, distribution, and shareholder servicing.

As of September thirtieth, 2025, belongings beneath administration (AUM) totaled $1.661 trillion. On July thirty first, 2020, Franklin Sources acquired Legg Mason (earlier ticker LM) for $4.5 billion in money, to go together with the idea of $2 billion in debt.

On November seventh, 2025, Franklin Sources reported fourth quarter 2025 outcomes. Whole belongings beneath administration equaled $1.661 trillion, up $49 billion sequentially, on account of $54 billion of internet market change, distributions, and different, and $7.2 billion of money administration internet inflows, partly offset by $11.9 billion of long-term internet outflows.

For the quarter, working income totaled $2.344 billion, up 6% year-over-year. On an adjusted foundation, internet revenue equaled $358 million or $0.67 per share, up 14% from $0.59 in This fall 2024. Throughout This fall, Franklin repurchased 2.6 million shares of inventory for $67 million.

Click on right here to obtain our most up-to-date Certain Evaluation report on BEN (preview of web page 1 of three proven under):

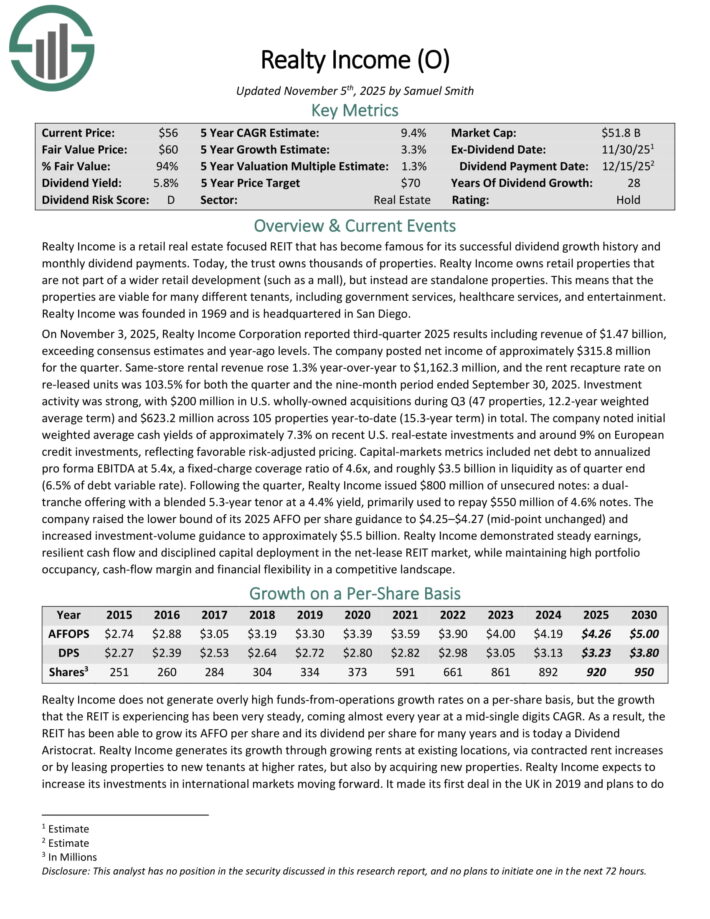

Excessive Dividend Inventory For The Lengthy Run #7: Realty Revenue (O)

Realty Revenue is a retail actual property centered REIT that has develop into well-known for its profitable dividend development historical past and month-to-month dividend funds.

Realty Revenue owns retail properties that aren’t a part of a wider retail improvement (comparable to a mall), however as a substitute are standalone properties. Which means that the properties are viable for a lot of completely different tenants, together with authorities providers, healthcare providers, and leisure.

On November 3, 2025, Realty Revenue Company reported third-quarter 2025 outcomes together with income of $1.47 billion, exceeding consensus estimates and year-ago ranges.

The corporate posted internet revenue of roughly $315.8 million for the quarter. Identical-store rental income rose 1.3% year-over-year to $1,162.3 million, and the hire recapture charge on re-leased models was 103.5% for each the quarter and the nine-month interval ended September 30, 2025.

Funding exercise was robust, with $200 million in U.S. wholly-owned acquisitions throughout Q3 (47 properties, 12.2-year weighted common time period) and $623.2 million throughout 105 properties year-to-date (15.3-year time period) in complete.

Realty Revenue’s most essential aggressive benefit is its world-class administration crew that has efficiently guided the belief up to now.

It has elevated its dividend for 28 consecutive years, and is on the listing of Dividend Aristocrats.

Click on right here to obtain our most up-to-date Certain Evaluation report on Realty Revenue (preview of web page 1 of three proven under):

Excessive Dividend Inventory For The Lengthy Run #6: Enbridge Inc. (ENB)

Enbridge is a Canadian oil & fuel firm that operates the next segments: Liquids Pipelines, Gasoline Distributions, Power Providers, Gasoline Transmission & Midstream, and Inexperienced Energy & Transmission.

Enbridge reported its third quarter earnings leads to November. The corporate generated revenues of CAD$14.6 billion in the course of the interval, which was down 2% in comparison with the earlier 12 months’s quarter, and which pencils out to US$10.5 billion.

In the course of the quarter, Enbridge grew its adjusted EBITDA by 2% 12 months over 12 months, to CAD$4.3 billion, up from CAD$4.2 billion in the course of the earlier 12 months’s quarter.

In the course of the third quarter, Enbridge was in a position to generate distributable money flows of CAD$2.6 billion, which equates to US$1.9 billion, or US$0.87 on a per-share foundation.

Whereas distributable money flows in 2024 had been down in US {Dollars}, that was as a consequence of forex charge actions – outcomes had been larger in Canadian {Dollars}. The identical holds true for Enbridge’s dividend, which was elevated by 3% in Canadian {Dollars}, to CAD$0.9424 firstly of the present 12 months.

Enbridge is forecasting distributable money flows in a variety of CAD$5.50 – CAD$5.90 per share for the present 12 months. Utilizing present change charges, this equates to USD$4.08 on the midpoint of the steerage vary, which might be up 6% versus 2024.

Click on right here to obtain our most up-to-date Certain Evaluation report on ENB (preview of web page 1 of three proven under):

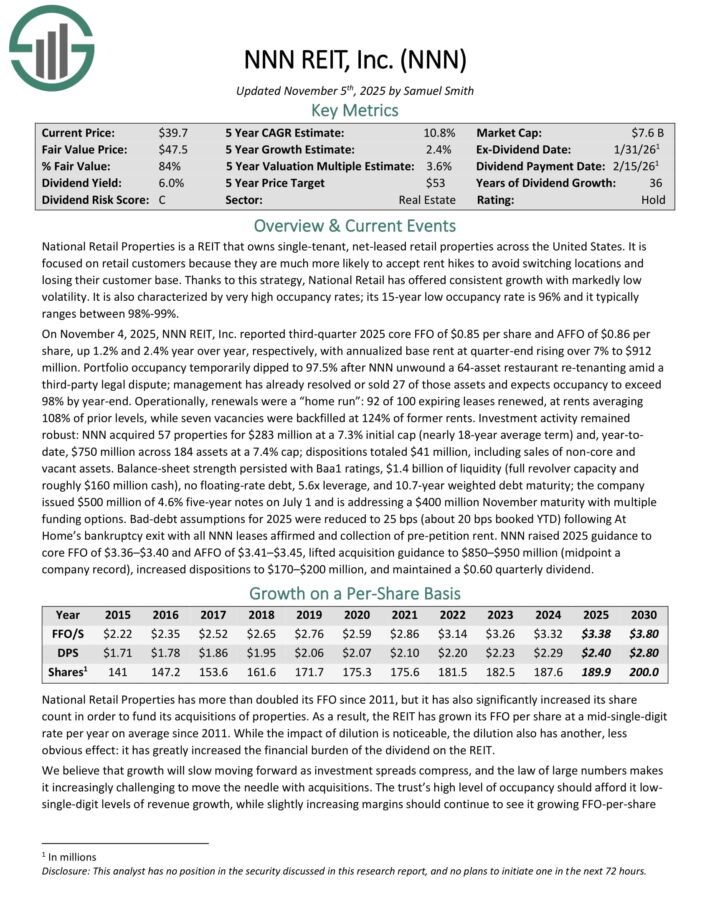

Excessive Dividend Inventory For The Lengthy Run #5: NNN REIT (NNN)

Nationwide Retail Properties is a REIT that owns single-tenant, net-leased retail properties throughout america.

Nationwide Retail has supplied constant development with markedly low volatility. It is usually characterised by very excessive occupancy charges; its 15-year low occupancy charge is 96% and it sometimes ranges between 98%-99%.

On November 4, 2025, NNN REIT reported third-quarter 2025 core FFO of $0.85 per share and AFFO of $0.86 per share, up 1.2% and a couple of.4% 12 months over 12 months, respectively, with annualized base hire at quarter-end rising over 7% to $912 million.

Portfolio occupancy briefly dipped to 97.5% after NNN unwound a 64-asset restaurant re-tenanting amid

third-party authorized dispute; administration has already resolved or bought 27 of these belongings and expects occupancy to exceed 98% by year-end.

Operationally, renewals had been a “house run”: 92 of 100 expiring leases renewed, at rents averaging 108% of prior ranges, whereas seven vacancies had been back-filled at 124% of former rents.

Funding exercise remained sturdy: NNN acquired 57 properties for $283 million at a 7.3% preliminary cap (practically 18-year common time period) and, year-to-date, $750 million throughout 184 belongings at a 7.4% cap.

Click on right here to obtain our most up-to-date Certain Evaluation report on NNN (preview of web page 1 of three proven under):

Excessive Dividend Inventory For The Lengthy Run #4: Verizon Communications (VZ)

Verizon Communications is among the largest wi-fi carriers within the nation. Wi-fi contributes three-quarters of all revenues, and broadband and cable providers account for a few quarter of gross sales. The corporate’s community covers ~300 million folks and 98% of the U.S.

On September fifth, 2025, Verizon elevated its quarterly dividend 1.8% to $0.69 for the November third, 2025 cost, extending the corporate’s dividend development streak to 21 consecutive years.

On October twenty ninth, 2025, Verizon reported third quarter outcomes for the interval ending September thirtieth, 2025. For the quarter, income grew 1.5% to $33.8 billion, however this was $470 million under estimates. Adjusted earnings-per-share of $1.21 in contrast favorably to $1.19 within the prior 12 months and was $0.02 higher than anticipated.

For the quarter, Verizon Shopper had postpaid telephone internet losses of seven,000, which compares to internet additions of 18,000 in the identical interval of final 12 months. Nevertheless, wi-fi retail core pay as you go internet additions grew 47,000, marking the fifth consecutive quarter of optimistic subscriber development.

Shopper wi-fi retail postpaid telephone churn charge stays low at 0.91%. The Shopper section grew 2.9% to $26.1 billion whereas shopper wi-fi service income elevated 2.4% to $17.4 billion. Shopper wi-fi postpaid common income per account grew 2.0% to $147.91.

Broadband totaled 306K internet new prospects in the course of the interval, which marks 13 consecutive quarters of at the very least 300K internet provides. The entire fastened wi-fi buyer base is sort of 5.4 million. Verizon goals to have 8 to 9 million fastened wi-fi subscribers by 2028.

Wi-fi retail postpaid internet additions had been 110K for the interval. Free money stream was $15.8 billion for the primary three quarters of the 12 months, up from $14.5 billion for a similar interval in 2024.

Verizon reaffirmed prior steerage for 2025 as properly, with the corporate nonetheless anticipating wi-fi service income to develop 2% to 2.8% for the 12 months. Verizon can also be anticipated to provide adjusted EPS development in a variety of 1% to three%.

Click on right here to obtain our most up-to-date Certain Evaluation report on VZ (preview of web page 1 of three proven under):

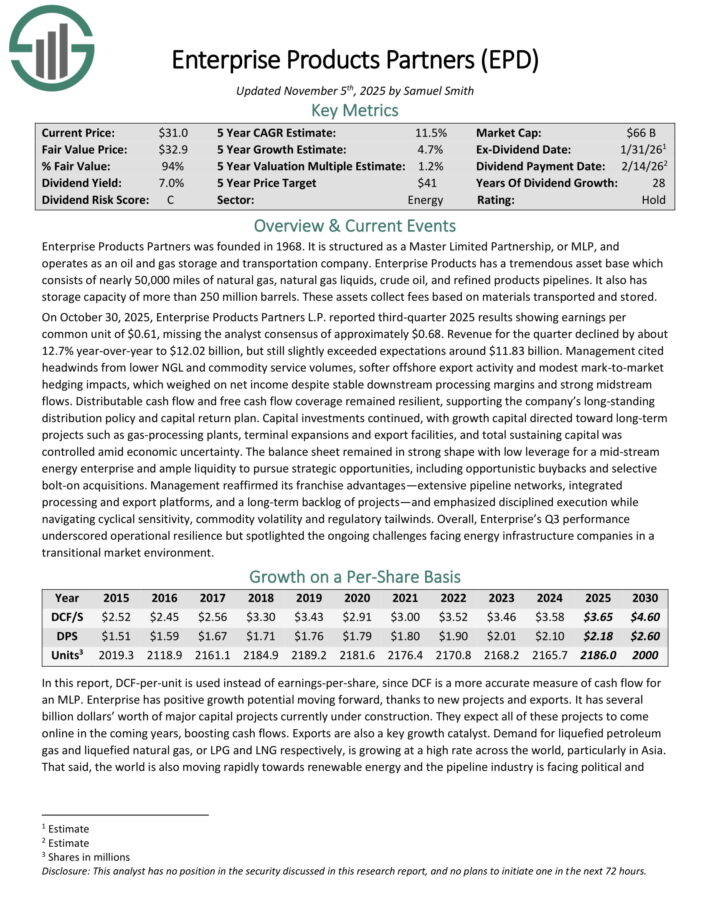

Excessive Dividend Inventory For The Lengthy Run #3: Enterprise Merchandise Companions LP (EPD)

Enterprise Merchandise Companions was based in 1968. It’s structured as a Grasp Restricted Partnership, or MLP, and operates as an oil and fuel storage and transportation firm.

Enterprise Merchandise has an amazing asset base which consists of practically 50,000 miles of pure fuel, pure fuel liquids, crude oil, and refined merchandise pipelines. It additionally has storage capability of greater than 250 million barrels. These belongings accumulate charges primarily based on supplies transported and saved.

On October 30, 2025, Enterprise Merchandise Companions L.P. reported third-quarter 2025 outcomes displaying earnings per frequent unit of $0.61, lacking the analyst consensus of roughly $0.68. Income for the quarter declined by about 12.7% year-over-year to $12.02 billion, however nonetheless barely exceeded expectations round $11.83 billion.

Administration cited headwinds from decrease NGL and commodity service volumes, softer offshore export exercise and modest mark-to-market hedging impacts, which weighed on internet revenue regardless of secure downstream processing margins and powerful midstream flows.

Click on right here to obtain our most up-to-date Certain Evaluation report on EPD (preview of web page 1 of three proven under):

Excessive Dividend Inventory For The Lengthy Run #2: Common Well being Realty Revenue Belief (UHT)

Common Well being Realty Revenue Belief operates as an actual property funding belief (REIT), specializing within the healthcare sector. The belief owns healthcare and human service-related services.

Its property portfolio contains acute care hospitals, medical workplace buildings, rehabilitation hospitals, behavioral healthcare services, sub-acute care services and childcare facilities. Common Well being’s portfolio consists of 76 properties situated in 21 states.

On October 27, 2025, Common Well being Realty Revenue Belief (UHT) reported third quarter 2025 internet revenue of $4.0 million, or $0.29 per diluted share, unchanged from the identical quarter in 2024.

Outcomes included a one-time $275,000 achieve ($0.02 per share) from a settlement and launch settlement associated to one in all its medical workplace buildings, partially offset by a $256,000 lower in combination property revenue, which included $900,000 of nonrecurring depreciation expense.

Funds from operations (FFO) rose to $12.2 million, or $0.88 per diluted share, up from $11.3 million, or $0.82 per share, within the prior 12 months interval.

Click on right here to obtain our most up-to-date Certain Evaluation report on UHT (preview of web page 1 of three proven under):

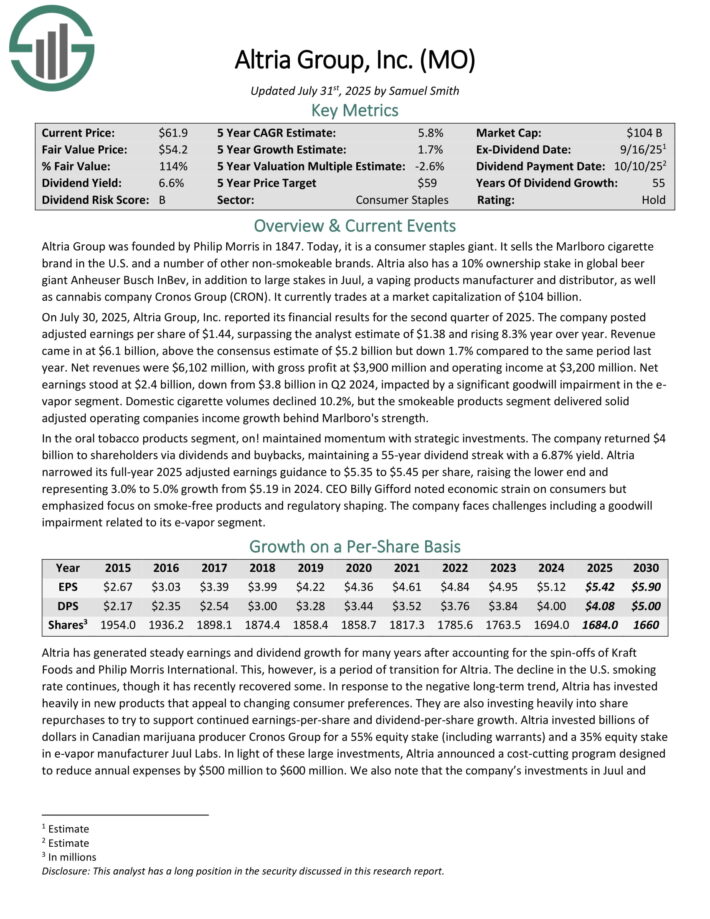

Excessive Dividend Inventory For The Lengthy Run #1: Altria Group (MO)

Altria is a tobacco inventory that sells cigarettes, chewing tobacco, cigars, e-cigarettes, and extra beneath quite a lot of manufacturers, together with Marlboro, Skoal, and Copenhagen, amongst others.

The decline within the U.S. smoking charge continues, although it has just lately recovered some. In response to the destructive long-term development, Altria has invested closely in new merchandise that enchantment to altering shopper preferences.

It is usually investing closely into share repurchases to attempt to help continued earnings-per-share and dividend-per-share development.

Altria invested billions of {dollars} in Canadian marijuana producer Cronos Group for a 55% fairness stake (together with warrants) and a 35% fairness stake in e-vapor producer Juul Labs.

Altria enjoys robust manufacturers throughout its product portfolio, together with the No. 1 cigarette model. Because of this, it has pricing energy and model loyalty.

As well as, tobacco corporations take pleasure in low manufacturing and distribution prices, due to its economies of scale.

This has fueled Altria’s large dividend development, enabling it to boast a formidable dividend development streak of 55 years.

Click on right here to obtain our most up-to-date Certain Evaluation report on Altria (preview of web page 1 of three proven under):

Extra Studying

If you’re enthusiastic about discovering high-quality dividend development shares and/or different high-yield securities and revenue securities, the next Certain Dividend sources will likely be helpful:

Excessive-Yield Particular person Safety Analysis

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

{kind=link}